“This guy wants to tell me we’re living in a community? Don’t make me laugh! I’m livin’ in America, and in America you’re on your own. America’s not a country, it’s just a business.”

– Killing them Softly, Andrew Dominik, 2012

When you are stuck in a Jackson Hole, keep digging. Over the past few decades, western governments have prioritised short term economic gains over long term measures through a combination of asset-based policies and de-regulation. Today, asset markets are at record highs and interest rates at their lows – with the Fed, Bank of England and ECB unwilling to risk a tantrum in order to bring policy back near normality. In addition, recent research by Atif Mian et al. presented at the Jackson Hole Symposium confirms a relationship that we have long argued since the onset of quantitative easing: rising inequality is not only a consequence of low interest rates, but also the cause of more savings and, in turn, of low interest rates.

The rich get richer, and rates go lower. As the top earners can only consume so much, they hoard wealth into unproductive investments: gold, bricks, space rockets – you name it. Secular stagnation is the result: stagnant productivity, declining growth potential and public debt overhangs were accumulated in the attempt to keep the economy going. The paradox – which we have highlighted for years as QE infinity – is that asset-based policies and rising inequality make secular stagnation self-perpetuating. Unfortunately, it is something the Fed and other central banks seem to ignore. The US infrastructure plan and Europe’s recovery fund are attempts to escape this QE infinity trap. However, without more targeted measures to rebalance opportunity and investment, such as the ones proposed by Senator Warren, the stimulus plans alone are unlikely to succeed.

China, instead, is trying something different. Like western countries, China also used credit to boost growth over recent decades in a rapid urbanisation process. This led to debt overhangs and a decline in the marginal impact of fiscal stimulus and credit. Today, China’s cross-cyclical strategy pledges to play the long-term game, improving financial stability, prioritising reforms and aiming at restoring equality and sustainability. In theory, this sounds like the opposite vs the short-term asset-based emergency stimuli implemented by western governments and central banks. In practice, however, the implementation of reforms has initiated a harsh crackdown on several sectors, with markets and investors responding very negatively, including Mr Soros in a recent article. Yet, these policies might be the much-needed micro regulatory actions necessary to rebalance the economy – and might perhaps be more effective than the one-size-fits-all monetary policy hammer. Which policy mix will work against secular stagnation? How will the geopolitical balance evolve after the Allies’ retreat from Afghanistan? And how should investors allocate capital? Buy Biden’s or buy Xi’s policies – or prepare for negative real rates, financial repression and debasement of paper assets to continue?

From Growth First to Common Prosperity

At the Party’s top economic commission’s meeting on 17th August, President Xi made a call for increasing efforts to promote common prosperity. The term quickly caught market attention and joined the latest catchphrases guiding China’s economic strategy, together with the so-called cross-cyclical approach. Nevertheless, it is not a completely new concept but a more forceful embodiment of the policy direction set by Xi four years ago.

Held every five years, the National Congress of the Chinese Communist Party (CCP) is probably the most important event for any China-watcher to get a sense of the country’s priorities and policy direction for the following years. The 19th National Congress, held in October 2017, saw the incorporation of “Xi Jinping Thought” into the party’s constitution, a similar status only enjoyed by Mao Zedong and Deng Xiaoping. It was also at this meeting President Xi redefined the party’s principal contradiction – the ultimate issue characterising each period of social development – to “the contradiction between unbalanced and inadequate development and the people’s ever-growing needs for a better life.” This marks a significant shift from the previous definition by Deng Xiaoping in 1981, which was between “the ever-growing material and cultural needs of the people versus backward social production”. In other words, China recognises that its growth first economic model supported by high investment and credit expansion over the past decades is no longer appropriate. Addressing the many economic imbalances and debt overhangs accumulated so far requires a fundamental shift.

Trend growth – time to rebalance towards the “average Xi”

A weak middle class has turned into a drag on economic performance, as China fails to boost domestic spending. China’s consumption share of GDP currently hovers around 40-55%, vs 65-75% in large developed markets such as US or Germany. The consumption share has been flat since 2012, and has fallen since 2000. The contribution of consumption to China’s growth has thus been falling over time, in line with the slowdown in trend growth. In 2007, China was growing at 9%, with 6% from consumption. In 2019, growth was down to 6%, with consumption down to 3%. The lack of social development has thus turned into a serious macroeconomic issue. As the industrial infrastructure reached capacity after 30 years catching up with the West and export-led investments, the only source of growth can be the development of a healthy domestic market. This is where policy makers will focus.

Corporate debt – too big or to fail?

The other side of “corporate-led growth” is a dangerously high level of private debt. China’s non-financial corporate debt is 165% of GDP vs less than 100% in most developed markets. Total debt is not higher than in developed market counterparts, but unlike those economies, it is concentrated in the private sector. High corporate debt is an inheritance of the strong banks and real estate de-regulation that accompanied the boom of the early 2000s. Corporate leverage crowds out household debt, which in China is 20-30% lower vs mature markets, and constrains monetary policy. As such, corporate balance sheets are vulnerable to any ‘pro-consumer’ shifts from policymakers.

Monetary policy – from FX to onshore liquidity

High corporate debt and a slowdown in growth poses the question of how monetary policy should be managed. In the past 20 years, the main problem of the PBoC was to pin down an adequate level of reserves and to manage the yuan. Given the export-led nature of the development model, CNY was all that mattered. In the current setup, internal economics will matter more. So policy rates will gradually move to target onshore liquidity on top of offshore targets and the exchange rates. A natural trade-off between growth and reserves policy will emerge, and the PBoC will need to take a more marked stance.

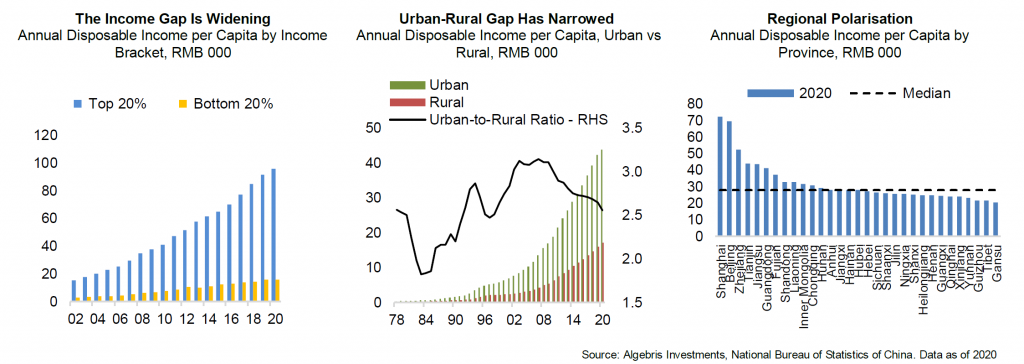

Rising inequality threatens to stall growth and ignite social instability

Over the past decade, the number of billionaires in China grew fivefold to reach 626 in 2021, while median annual urban household disposable income more than doubled to RMB 43,834 (~$6,800) in 2020. However, the growth in wealth and income has not been evenly distributed. Over 600mn people earn less than RMB 1,000 a month (~$150), while median income of the top 20% of households is 6.2x of that of the bottom 20%. Great disparities also still exist across regions and between urban and rural households. At the same time, those high-income households living in Tier 1/2 cities have issue too – high and rising cost of living, especially for the so-called “three big mountains” of housing, education and health care.

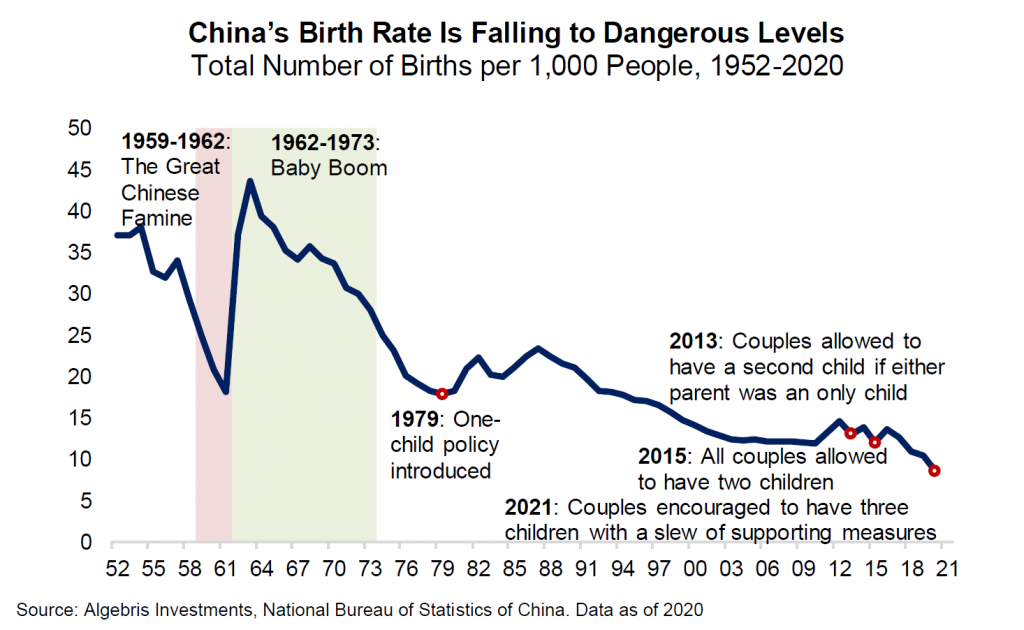

On the one hand, a weak tail of low-income households and sluggish growth in middle class income mean limited purchasing power, which in turn impedes the transition to a consumption-driven economy. On the other hand, more serious social problems that could threaten the party’s basis of governance may ensue. The 2019 Hong Kong protests likely rang an alarm bell for the CCP about how much social polarisation could be caused by unaffordable housing. In addition, high economic burden was found by a nationwide survey to be the top reason behind China’s falling birth rate, contributing further to its deteriorating demographics.

Environmental problems add risks to long-term growth and public health

The environmental costs of China’s rapid industrialisation include mass greenhouse gas emission, air pollution, desertification, water shortages and soil contamination, exposing the country to increasing risks of climate change and public health issues. Poor air quality and deteriorating living conditions are also fuelling public dissatisfaction towards the government.

Intensified regulation reflects a stronger push in the new policy direction

Against this social and economic backdrop, it is not difficult to see how the regulatory tightening over the past months is exactly targeted at the issues mentioned above to reflect the CCP’s new policy direction. The goal of common prosperity is more sustainable and equitable growth, while the cross-cyclical approach aims to be pre-emptive and anticipate systemic risks. More specifically, tighter policy for the property market is aimed at keeping urban living costs in check and prevent further wealth polarisation, while the banning of after-school tutoring attempts to reduce education costs and promote demographics. The antitrust campaign, crackdowns on big tech companies and shunning of the “9-9-6” work culture are efforts to reign in corporate power and re-distribute economic value to workers and consumers. In addition, the 2060 Carbon Neutral pledge and accompanied reform plans reflect growing urgency to tackle environmental issues and promote sustainability.

Implications of Common Prosperity

The August CCP meeting states that rather than being egalitarian or there only being a few people who are prosperous, common prosperity refers to affluence shared by everyone in both material and cultural terms. A central pillar of the strategy is the creation of an olive-shaped social structure with an expanded middle-income group, which would be achieved across both incomes and living costs.

On the income side, the CCP called for a three-layer distribution system, where primary distribution refers to a more progressive wage system, secondary distribution refers to government interventions through transfer payments, enhanced social security and tax adjustments, while third distribution refers to incentives for firms and high-income individuals to give back to the society through charitable activities. On the cost of living, the key is reducing people’s cost of living through public services and industry regulations.

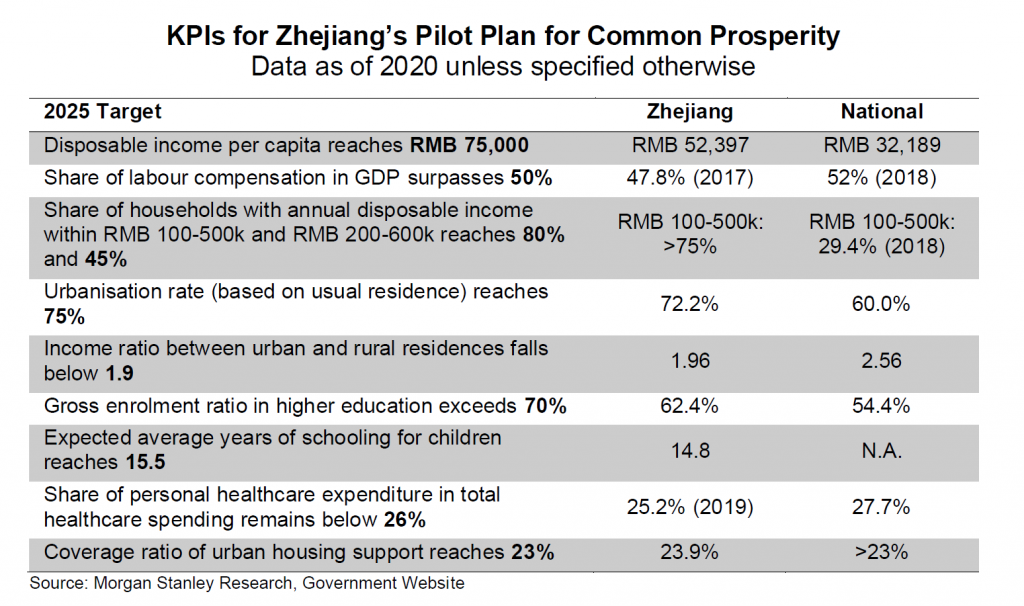

In the long term, these measures should benefit China with a more balanced and efficient economy, if implemented prudently with measurable targets met, such as those listed in Zhejiang’s Province’s detailed pilot plan. Prominent Chinese economists also moved quickly to clarify that the policy goal was not to “kill the rich to help the poor”. However, the risks are that opaque policy communication, poor policy coordination or over-regulation could create undue uncertainty and hurt private investor confidence, leading to short-term growth and market headwinds.

Conclusions: Pick Your Version of State Capitalism

“Government is not the solution to our problem. Government is the problem.”

– Ronald Reagan, 1981

In this environment, the most important decision for investors will be to choose which policy mix will succeed. The US and most western economies remain stuck in a variety of asset-based policies. These have failed to improve growth potential and inflation – instead, they have supported large firms in capital markets, incentivising concentration, reducing competition, and boosting inequality, which in turns correlates with high savings and persistent low interest rates. China, on the other hand, is using micro policy and regulation to resolve the many overhangs accumulated during recent decades.

China: align with the Politburo

President Xi’s recent policy actions have negatively impacted almost all Chinese asset prices. Chinese stocks’ valuations have cheapened but long-term risks persist. Xi’s new policies aim to address three points of concern: anti-competitive/monopolistic practices, data security and inequality. Valuations are attractive, but prices are likely to stay volatile, as it is unclear what sector Xi might target next. Chinese credit remains under pressure too, with spreads over twice as wide as other high yield firms. The policy action in the property sector began with rules to promote deleveraging but has since escalated to lending restrictions and higher mortgage rates. Xi has since reiterated that “houses are for living not for investing”. As such, we think the aim is to control house price growth, not to cause a large correction. However, the party might be underestimating the risk of over-tightening spill-overs from defaults in large systemic firms.

United States: the Dollar has to give

In the short term, Xi’s policy actions may slow China’s growth. Even though the PBOC might start easing in the second half of the year, the slowdown is already a drag on global growth and it is likely to result in a dovish bias from DM central banks. But unlike in 2015, when China’s slowing growth resulted in a market crisis, global credit spreads and volatility are likely to remain contained this time around for the following reasons. Firstly, China’s growth is slowing but starting from a higher base; secondly, credit support is now embedded into DM central banks’ reaction functions, with even the Fed having bought credit in its Covid response. Over time, the use of monetary policy tools and fiscal deficits a la MMT is likely to undermine the Dollar.

Europe: hang together or hang separately

Against a backdrop of a United States government dealing with a difficult economic rebalancing, the recent withdrawal from Afghanistan represents the confirmation of a profound turning point. Those US allies who thought the Biden administration would make a U-turn from Trump’s hands-off foreign policy strategy will now have to revise their assumptions. Ukraine, Taiwan, the Baltic states and the EU itself, will have to strengthen their defence capabilities. We remain selective on bond yields and credit spreads, which remain near record lows. Over the recent weeks of volatility, we have added upside through equity optionality in sectors linked to economic reopening and Chinese firms.

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.