Central bank monetary policy has lifted asset prices but reduced yields on most market-based instruments. The impact of this, combined with the nerves of the market last year during the Covid-19 recession took yields to all-time lows. Currently, 27% of the global fixed income market yields negative returns and 94% yields below 3%. This impacts the banks in a number of ways:

- Securities on banks’ balance sheets have gone up in value (but generally have not been marked-to-market upwards) but the reduced yield on new investments flows through to the P&L and is a drag on future revenues/profits.

- With low yields, the spread that banks add on for their ‘margin’ tends to be reduced as well causing a further headwind.

- Banks have been considered collateral damage over the last 5-10 years with regard to central bank policy…with regards to their net interest margin.

- However, both central bank monetary policy, combined with governmental fiscal support has created a significantly better environment for credit (relative to where it would have been with the government-induced lockdowns without any support). As such, despite the large provisions taken in H1 ’20 last year, from Q3 ’20, provisions have been consistently falling. It is also clear that in general European banks have over-provided and should start to release the provisions over 2021 and 2022.

Interestingly, the first three negative points above have started to inflect the other way. Central banks have started to compensate the banks for some of the negative impacts caused by their policies. One particularly negative impact is that the banks are very liquid/strong having a lot of deposits. In Europe, they are required to deposit a certain amount with the central bank, who pay negative rates to the bank (essentially a tax). From last year, in June, the ECB started paying the banks 50bps to borrow money, heavily reversing the adverse impact of negative policy rates. With long bond yields starting to go back up (US-10 year up from 50bps in August last year to ~160bps now), there is greater scope to charge a higher margin and receive a higher yield. Whereas this is negative for all other sectors in the economy, it is almost uniquely positive for the bank sector.

Below is an example of what is happening to the banks’ balance sheet and P&Ls at the moment (especially interesting with reference to net interest margins and provisions as mentioned above):

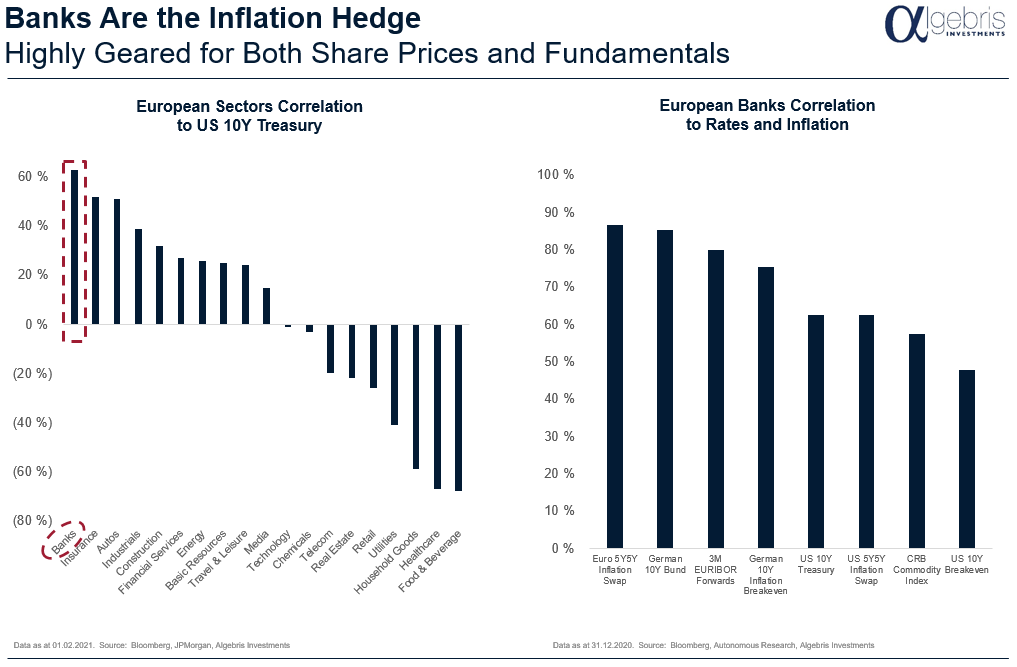

We have essentially started both a new economic cycle but we are clearly at the start of a new monetary cycle as well. We currently have ‘peak’ monetary support and the next decade is likely to see a gradual removal of that support. For the bank sector this is good news, as can be seen below:

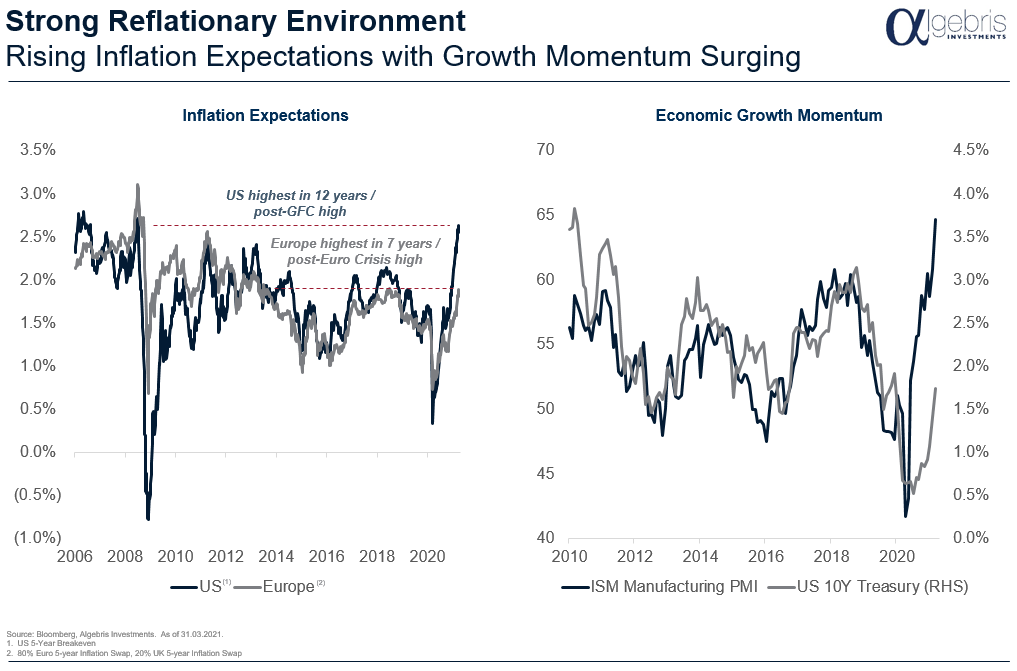

Of course, we can be slightly cynical on whether it is central bank policy that is driving this, but if you include the fiscal support from government and perhaps more importantly now, the successful vaccine rollout, these policies are improving inflation expectations and the improvement in the economy. However, irrespective of who wants to take credit, one of the biggest beneficiaries is the bank sector as the economy improves, as can be seen below:

This document is issued by Algebris (UK) Limited. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris (UK) Limited. Algebris (UK) Limited is authorised and Regulated in the UK by the Financial Conduct Authority. The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Under no circumstances should any part of this document be construed as an offering or solicitation of any offer of any fund managed by Algebris (UK) Limited. Any investment in the products referred to in this document should only be made on the basis of the relevant prospectus. This information does not constitute Investment Research, nor a Research Recommendation. Algebris (UK) Limited is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris (UK) Limited, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions. The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is for private circulation to professional investors only. © 2021 Algebris (UK) Limited. All Rights Reserved. 4th Floor, 1 St James’s Market, SW1Y 4AH.

This document is issued by Algebris (UK) Limited. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris (UK) Limited.

Algebris (UK) Limited is authorised and Regulated in the UK by the Financial Conduct Authority. The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Under no circumstances should any part of this document be construed as an offering or solicitation of any offer of any fund managed by Algebris (UK) Limited. Any investment in the products referred to in this document should only be made on the basis of the relevant prospectus. This information does not constitute Investment Research, nor a Research Recommendation. Algebris (UK) Limited is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris (UK) Limited , its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is for private circulation to professional investors only.

© 2021 Algebris (UK) Limited. All Rights Reserved. 4th Floor, 1 St James’s Market, SW1Y 4AH.