As we have discussed in our latest Algebris Bullet, energy continues to be the field on which the hardest and most controversial battle of this economic war is going to be fought. Despite an increase in political noise, the EU has been treading carefully around energy. The recently introduced EU oil embargo is likely to be little and late, from the standpoint of putting short-term financial pressure on the Russian war effort, the move increases the chance of retaliation in gas markets. Meanwhile, countries are spending considerable amounts to shelter domestic consumers and producers from energy costs – a quest that in the longer term may put pressure on State’s coffers, especially for countries with narrower fiscal space. The EU will make additional resources available, but they may be unequally distributed across countries. Overall, a sudden cut-off of Europe from Russian energy remains the biggest downside risk to the continent’s growth prospects, and the success of the EU energy independence plan will be a litmus test for EU coordination.

EU Oil Embargo – Politics First

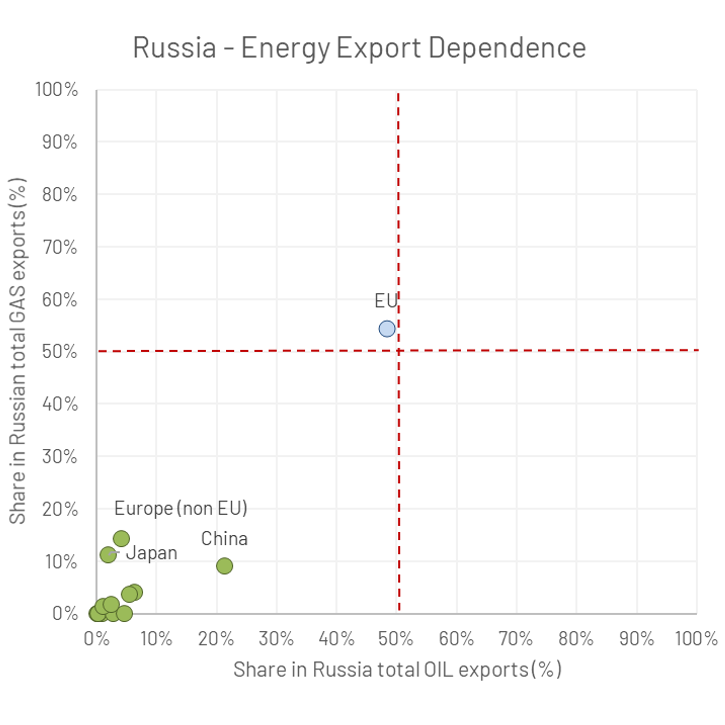

After refraining from a ban on Russia’s energy in the initial rounds of sanctions, in May the European Commission published a proposal of a gradual ban on Russian oil imports. Oil is a matter on which the EU has leverage vis-à-vis Russia because the European block’s oil imports are more diversified than its gas imports. For Russia, the EU market accounts for about 50% of oil exports: an EU oil embargo would therefore not only have a direct economic impact on the Russian energy revenues, but also strengthen the hand of the residual buyers of Russian oil in asking for discounts (something both India and China are reportedly already doing).

Banning Russian oil from entering the EU however proved easier said than done. The sixth package of EU sanctions including the oil embargo took three weeks of negotiations to overcome a veto by Hungary – in yet another proof of how controversial and polarising energy sanctions continue to be in the EU. The package that was agreed on May 31st is weaker than the original European Commission’s proposal. First, the transition is FAIRLY long, as the embargo will not come into force before 6 months (for crude oil) and 8 months (for refined oil). Second, a proposed ban on EU tankers shipping Russian oil to third countries was scrapped. With the EU accounting for 17% of global oil tankers’ capacity – mostly through Greece and Malta – such a ban on EU tankers would have made a dent in Russia’s export capacity (UNCTAD data on maritime trade. As at end-2021. In dead weights tonnes DWT) and increased costs for Russia of shipping its oil around the world. Yet, with oil tankers accounting for approximately 65% (UNCTAD data on maritime trade. As at end-2021. In dead weights tonnes DWT) of the entire Greek fleet, it is probably unsurprising that it turned out impossible to balance different political interests on this piece of the puzzle. A ban on insurance of oil cargos (90% of which is done in London) is included in the package but with a 6-month grace period and details still to be negotiated. Pipeline oil has been temporarily exempted, and while Germany and Poland voluntarily committed to cut themselves off the Druzhba pipeline by end/year, there is no set deadline for the general exemption. Overall, the EU oil embargo is a measure that goes halfway: the risk is that it will leave enough time for Russia to diversify its oil exports before it enters into force.

The Gas Standoff – Risk of Retaliation

The difficulties in striking agreement on the oil ban make the prospect of a politically more controversial EU ban on Russian gas less likely than it had appeared weeks ago. The game theory of the gas standoff is simple: Putin’s request for gas payments in roubles was a step to circumvent sanctions, replenish foreign reserves and weaponize gas to seed division in Europe. So far, the Kremlin has been following through with its threats: Poland’s PGNiG, Bulgaria’s Bulgargaz, Finland’s Gasum, Denmark’s Orsted and Dutch’s GasTerra all faced a halt of flows after refusing to pay in accordance with the rouble gas payment scheme. Despite EU guidance suggesting that opening accounts in roubles at a Russian bank to pay for gas may be in breach of the bloc’s sanctions, enough ambiguity was left by the Commission’s guidance for major energy companies to press ahead – highlighting the difficulty the EU is facing to show a united front on energy sanctions.

Source: Algebris Investments, GIE AGSI. As at 11 June 2022

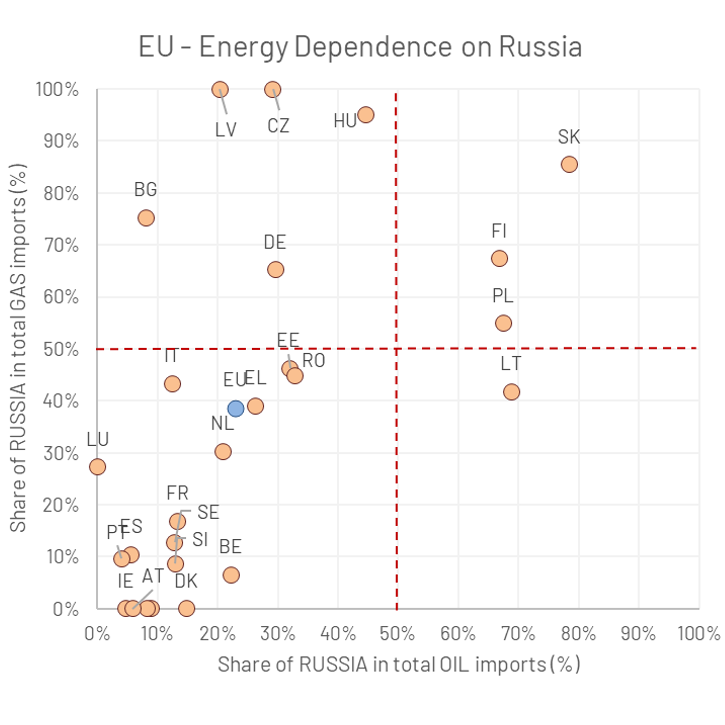

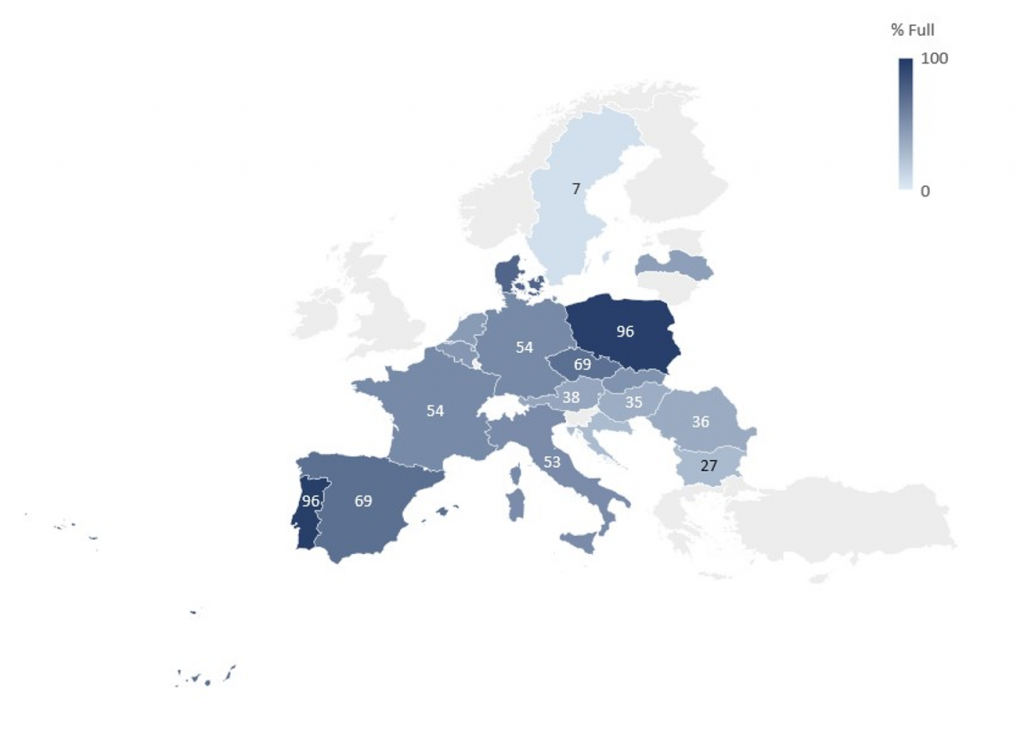

From Europe’s standpoint, the calculation is also quite simple: sanctions have demonstrated that forcing a sudden stop on a current account surplus economy is very difficult, unless the other party is willing to take the difficult decision to stop importing from it. To effectively heighten financial pressure on Russia in the hope of accelerating a resolution of the conflict, the EU would therefore need to step away from Russian energy as soon as possible. On the 18th of May the European Commission published REPowerEU, a plan setting out how the block is to achieve energy independence from Russia by 2027. In the meantime, however, the EU’s move to impose an oil embargo increases the risk of retaliatory actions on natural gas by Russia. In the weeks following the announcements – although reportedly for different reasons – Gazprom communicated that it would cut daily gas deliveries to Germany via Nord Stream 1 by ~40% and deliveries to Italy’s ENI by 15%. While gas storage levels have kept increasing over the past few months across the EU, storage in most countries is still far below the 80% target to be achieved by November 2022.

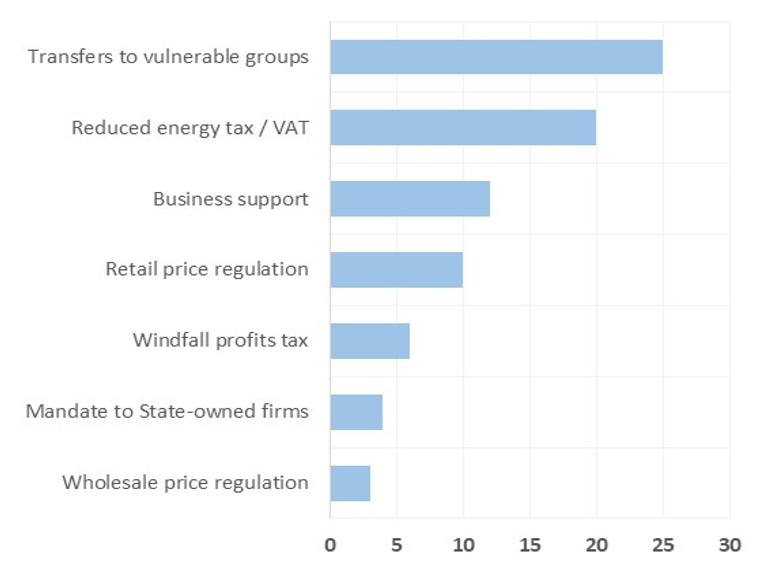

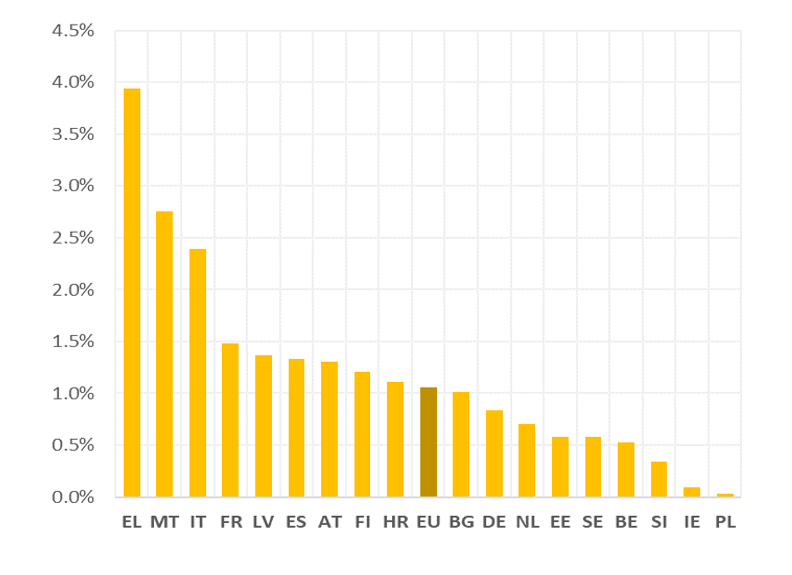

An interruption of Russian gas supply to Europe would thus be a tough test for political cohesion in the EU. So far, governments have been going to great lengths to shelter producers or consumers from the impact of higher energy prices. Almost all EU Member States have undertaken transfers to vulnerable groups, and a majority has introduced reduced energy taxes or energy VAT rates. In some cases, governments rolled out business support measures and retail price regulations or – less frequently – gone all the way to regulate the wholesale market and impose mandates on state-owned energy firms. At the EU level, the cost of national policies on energy prices introduced between Q4-2021 and Q2-2022 totals around 1% of GDP. But some countries – such as Greece, Italy, or France – have been spending significantly more. The longer the tensions on gas markets drag on, the more difficult it may become for governments – especially those who already have a narrower fiscal space as a legacy of previous crises – to mitigate the impact of higher energy prices on their citizens’ standards of living. The risk of fatigue and local political crises could increase accordingly.

Source: Algebris Investments, Bruegel. Data as at end-May 2022.

Source: Algebris Investments, Bruegel. Data as at 15/06/2022.

REPowerEU – Watch Implementation

The Commission estimates that achieving independence from Russian gas will require an investment of EUR 210 billion over 5 years, although compensated in part by almost EUR 100 billion a year in lower energy import costs. The new investment breaks down into EUR 113 billion for renewables and key hydrogen infrastructure, EUR 56 billion for energy efficiency and heat pump, EUR 41 billion for adapting the industry to use less fossil fuels, EUR 37 billion to increase biomethane production, EUR 29 billion in the power grid to increase electricity usage, and EUR 12 billion to increase LNG imports and secure oil supply through 2030.

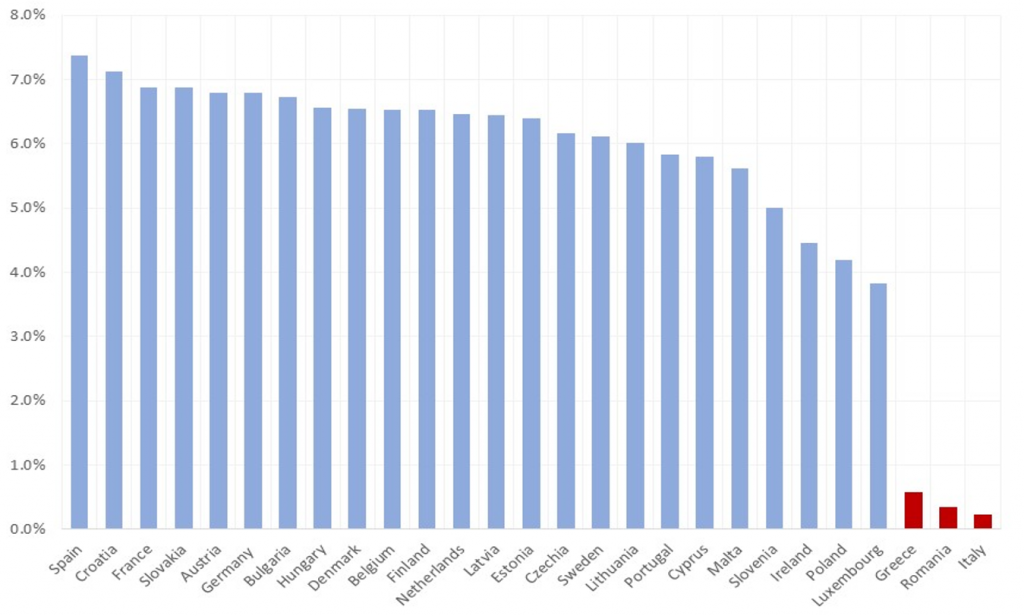

Countries can use the unclaimed loans under the Next Generation EU Recovery and Resilience Facility (RRF) for financing REPowerEU investments. These amount to EUR 225 billion and member states are allowed to request an amount up to 6.8% of GNI. At the end of 2021, only seven countries (Greece, Italy, Cyprus, Poland, Portugal, Romania, and Slovenia) had applied for RRF loans – and only Greece and Italy had requested the total amount they are entitled to.

Repurposed loans and grants will be earmarked to 6 priorities: (i) boosting buildings energy efficiency and decarbonising industry; (ii) increasing production and uptake of sustainable biomethane and renewable or fossil-free hydrogen, increasing the share of renewable energy; (iii) addressing internal and cross-border energy transmission bottlenecks and supporting the electrification of transport infrastructure; (iv) accelerated requalification of the workforce towards green skills; (v) boosting value chains for the production of key materials and technologies linked to the green transition; (vi) improving energy infrastructure and oil and gas facilities for immediate security of supply.

The European Commission also plans to issue new RRF grants to be funded by the auctioning of Emission Trading System (ETS) allowances currently held in the Market Stability Reserve, worth EUR 20 billion. Assuming that these new RRF grants are allocated using the same country shares used for other RRF grants, Italy and Spain will be the biggest beneficiaries – receiving EUR 4 billion each – followed by France, Germany and Poland. As a share of GDP, the EU will therefore make available funds worth on average 5.5% of GDP that countries will be able to use to compensate for securing energy supply and accelerate the transition over the next few years. But for those countries that have already taken all or a large part of the Next Generation EU loans, the amount available will be much less. Italy, Greece, and Romania will have access to a mere 1% of GDP in extra RRF funds to use for REPowerEU purposes.

This leaves these countries vulnerable to toughening of EU sanctions on energy and potential pressure points for Russia to leverage division in the EU. While some of the REPowerEU objectives listed above overlap to some extent with the priorities set out in the green envelope of Next Generation EU and part of the RRF loans that these countries have already taken out could be repurposed to fit REPowerEU investments, it is unclear what that would require in terms of reopening and renegotiating the already submitted National Recovery and Resilience plans and the included milestones and targets. As such, this is unlikely to happen unless the process is streamlined significantly.

Overall, REPowerEU shows that shared catastrophes (like a pandemic or a war) are best tackled together at the EU level than nationally, and it is the first tangible step the EU has taken in a long time towards the much discussed goal of strategic autonomy. Yet, implementation will be key. Similarly to Next Generation EU, the success of this initiative will depend on the willingness and ability of Member States to engage in cooperation and make potentially difficult concessions. So far, achieving a balance of different interests on energy matters is proving more difficult than it has been in the context of the pandemic response. As such, a risk remains that fragmentation yields suboptimal results in terms of energy security and competitiveness at the EU level, creating a more meaningful challenge for the Continent’s growth prospects all while weakening the EU foreign policy stance on Russia at a crucial time.

Silvia Merler – Head of ESG and Policy Research

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in

investment activity on the ground that it is being issued only to such types of person.

This is a marketing document. The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only,

and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only.

Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2022 Algebris Investments. Algebris Investments is the trading name for the Algebris Group.