The energy transition requires massive investments in a very short timeframe. This poses a short-term challenge to renewable companies and long-term opportunities for investors.

1. The problem | The financing challenge

In the early 80s, the song “Money for Nothing” by Dire Straits sarcastically judged the morality of modern times where there is injustice – even absurdity – in how wealth is distributed for “doing nothing”. At first sight, some might think that investing in the renewable energy sector today calls for a similar degree of cynicism.

First and foremost, the energy transition means one thing: decarbonizing the production of electricity. This requires the construction of renewable energy generation facilities, i.e. wind and solar plants.

Yet, herein lies the challenge: renewable companies must finance massive investments in a relatively short timeframe against a cash generation capacity that will not fully materialize until several years into the future. And this must occur in an environment of high interest rates, input cost inflation and supply chain constraints.

This has turned equity investors away. As market valuations have been depressed, skepticism around the ability of the renewable industry to create value from future investments has been growing.

Is investing in the renewable energy sector really “money for nothing”? We beg to disagree. We believe the renewable sector presents a compelling long-term investment opportunity for both equity and bond investors. The key to seizing that opportunity is a clearer understanding of the sector’s intertemporal cash profile and funding needs.

Source: Bloomberg Finance L.P., data as at 18/09/2023

2. The perfect storm | Chasing net-zero against macro headwinds

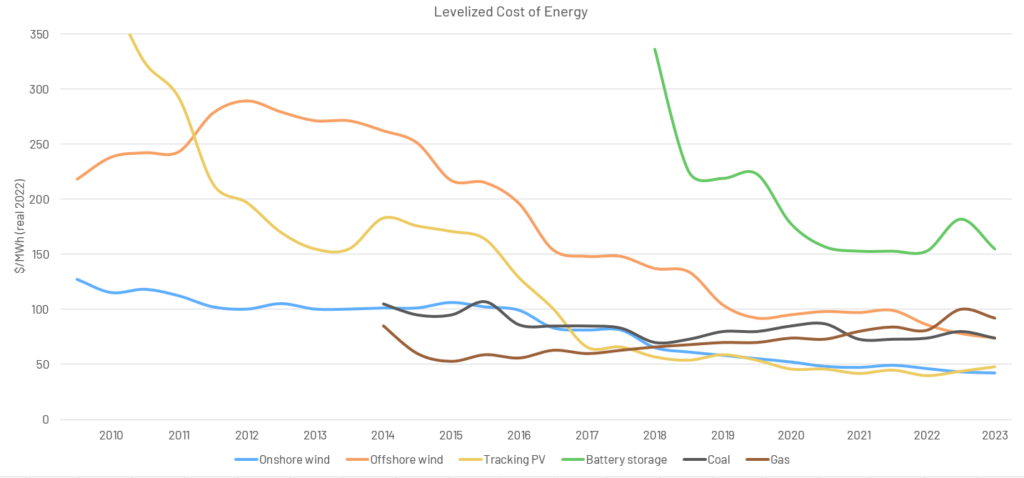

The transition out of an economic system where energy needs are mostly met by fossil fuels towards a new normal where net-zero electricity will be the largest energy source is imperative to stop global warming. Renewable energy sources (RES) have also become increasingly cheap over time. Today, the cheapest way to produce electricity is by wind and solar.

Source: BNEF, data as at 30/06/ 2023

At the same time, the previously unquestioned reliability of fossil fuels has proven to be vulnerable to geopolitical risks. The recent invasion of Ukraine by Russia has added a clear sense of urgency to the need to diversify away from fossil fuels, while increasing public awareness about the vulnerabilities of our current energy regime.

Governments around the world have now acknowledged this as part of their policy priorities. Across major global economic jurisdictions, we have seen a rush to provide unprecedented incentives and subsidies to clean energy players and the entire supply chain that stands behind them. The US Inflation Reduction Act (IRA) pledges USD 400 billion for climate change, with funds targeted to clean energy, climate and air pollution, clean mobility, clean manufacturing and agriculture. The European Green Deal is expected to provide tax credits, accelerated depreciations and/or subsidies oriented to the net-zero age industry, with total funds of around EUR 390 billion.

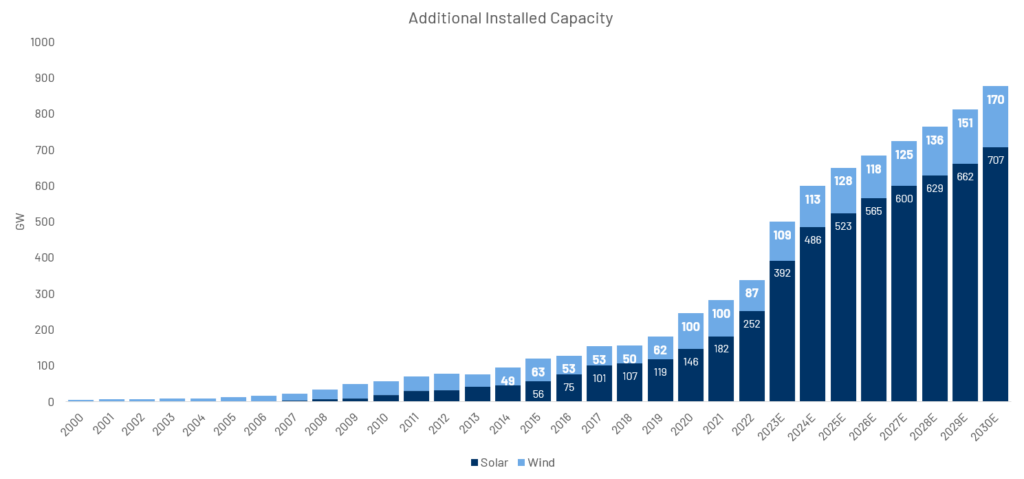

As a result, renewable energy annual capacity additions are estimated to more than double from today’s level, where c.850 GW p.a. could be built by 2030. Almost 80% of this capacity increase is expected to be in the solar sector (Fig. 3).

Source: BNEF, 2023. Future projections may not materialize.

From an investor’s perspective, the problem is that renewable capacity needs a long time to be built and therefore to generate cash. For example, the experience of Iberdrola – a leading player in the renewables space – suggests that the construction of an onshore wind farm can require 4 to 8 years, while an offshore wind farm can take 7 to 11 years. The payback time is on average 7 to 10 years from start of operations against an estimated lifetime of more than thirty years.

Source: Orsted, 2023.

This stretched intertemporal cash flow profile has pushed renewable players into a perfect storm.

The increase of interest rates has raised the cost of debt, exactly at the time when unprecedentedly high levels of debt were needed to finance the capacity expansion demanded by the net-zero transition. The resulting increase in the cost of capital has led to concerns among investors about the effective returns on investments that were sanctioned in the age of near zero interest rates.

At the same time, the cost of raw materials and components required for new capacity has dramatically increased over 2020-22. Cost inflation has been a very rude awakening that has caught the entire renewables sector by surprise: companies in this space are used to yearly double-digit reductions in input costs and have therefore never been very careful in hedging them. The consequence of this has been a decrease in the expected returns of projects under development, whose future revenues had been fixed upfront based on the expectation of much lower capital expenditures.

Fonte: Li, Chen, et al. (2022) Dati economici della Federal Reserve

Finally, supply chain constraints have delayed the completion of projects under development, which obviously causes a further delay in cash generation.

Examples of the havoc caused by the perfect storm include the USD 2.5 billion impairment taken by Orsted on a single project in the U.S., and the cancellations or freezing of new projects in the UK and the U.S. by Iberdrola and Vattenfall.

3. Setbacks do not mean the industry is broken

While investing in renewables may at first sight look like “money for nothing”, as market valuations have been depressed and equity investors have by and large shunned the sector, we believe that the underperformance of the renewable energy players year to date is not fully justified by long-term fundamentals.

Source: Bloomberg Finance L.P., data as at 18/09/2023

First of all, the dramatic surge in both interest rates and input costs of the last two years are most likely to remain “exceptional” – and impact only 2021-22 legacy projects. New projects are likely to incorporate cost projections in line with the current macroeconomic environment, hence reducing the risk for companies to take drastic moves such as the recently observed impairments.

Secondly, renewable capacity has very low operational costs once built, and revenues are largely secured by long term purchase agreements – often signed directly with government owned counterparties. Therefore, future cash generation remains safe.

Third, financing needs are not a problem. Rates are most likely close to peak levels, which means financing costs are going down and returns are going up. But most importantly, companies operating in the renewable energy sector can successfully engage in asset rotation. The assets on the balance sheets of renewable players can in fact be sold even before project completion to generate cash that can then be re-deployed to finance new developments. Retaining 100% financial ownership of these assets gives no strategic or operational advantages. What is needed is operational control. On the other hand, there is significant appetite from investors like pension funds for assets that can guarantee relatively safe long cash streams. One example of a company that has extensively used a similar strategy of “asset rotation” is EDP Renewables with ca. 2 GW sold in the last couple of years with over EUR 3.3 billion in proceeds.

Last but not least, the industry seems to have steered towards a more disciplined growth strategy, where profitability has become more important than top line growth. The recent auctions for new offshore wind capacity in the UK went deserted, because the cap imposed on future revenues was deemed too low by all potential bidders. Given that the UK has committed to a vast expansion of offshore wind capacity, the government will have no choice but to raise the cap and therefore the returns of future developments. Similarly, German grid operators have been successfully challenging the Federal Regulator in court, arguing that the offered rates of return were too low for the companies to remain competitive when billions of Euros must be spent to upgrade the grid for new wind and solar capacity.

For equity investors we believe that as industry risk has now been priced in, there may be significant opportunities in the market. Free cash flows are likely to improve. Higher negotiated prices and more reasonable cost assumptions mean that the profitability of new projects should be safer than in the past. As the return on capital employed (ROCE) improves, valuations will follow suit.

For bond investors, we believe the opportunity is best played in subordinated (hybrid) bonds of renewable-heavy utilities in Europe. The industry’s relatively high leverage means that too much senior debt issuance would jeopardize ratings. At the same time, the very stable nature of revenue makes debt financing suitable. The path of least resistance is holding a portion of liabilities in hybrid securities, who have a debt-like profile but are junior to senior bonds and their call can be postponed in challenging market environments. These securities tend to come at an attractive ~300bp spread – for a rating typically just below investment grade (IG) – thus coming at a substantial discount on senior debt. We see these securities as a pocket of value with great potential in European debt markets.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2023 Algebris Investments. Algebris Investments is the trading name for the Algebris Group