2022 has been a year of increasing and hightened tensions. Supply bottlenecks, the energy crisis and central bank tightening all happening within a few months. As always, tensions explode where vulnerability is highest. In 2022, this pressure point was the bond market, following ten years of easy policy that had removed risk premium. The move was fast. Global inflation rose from 2% to 10% in the space of a year. Risk assets crashed. US Treasuries lost 15%, the worst one-year return of the past century. Bond markets quickly rotated from one extreme to the other.

2023 will likely be characterised by a reversal of this tension. In July, we pointed to excessive fears being priced in credit. Since then, tensions in bond markets relieved meaningfully. Supply bottlenecks eased, driving a 20% drop in global producer prices. Europe managed to fill gas storages, leading to a normalization in commodity prices. Spiking mortgage rates are helping a drop in global house prices. The new bond anomaly looks set to unwind as quickly as it happened. In the process, monetary policy turned tighter. The unwinding of this tension will come at a cost – a slowing economy – but that is not a bad thing for bonds.

We believe inflation has peaked. Headline CPI is 2% off the highs in the US, and has stopped rising in Europe. Leading indicators point to further downside. Slowing macro and tighter policy will continue to push core inflation lower. We see US inflation at 5% by July 2023 (core at 3%). The Fed will bring policy rates to 5% in 2Q23, and the next debate will be on rate cuts. The extent of disinflation is less clear, but supply shocks fade quickly. During the OPEC crisis in 1973-74, it took one year for US inflation to halve from its 12% peak. Our US model gives roughly the same prediction for the current situation.

Global growth will slow but not slump. European PMIs are pointing to a contraction, but not a deep one. Gas facilities have been filled and gas prices have eased. US household wealth is falling but remains well above trend. In 2022, US and European macro data fared better than projected during the summer, and 2023 forecasts are bottoming. Absent negative shocks, real growth may hover around 0% in the US and Europe next year.

China is the main source of potential upside for 2023 growth. The re-opening of the economy, that started in October, will be bumpy as growth in Covid cases triggers occasional lockdowns. Restrictions are being lifted at the local level, however, suggesting a positive trend. Trade and macro data are weak, adding to the case for a lift-off. Re-opening is likely to reach meaningful levels by next summer, and the macro environment will benefit in 2H23. In this scenario, China may grow 5% in 2023, leaving the gap with US the highest since 2013.

Falling inflation and slower growth means rate hikes are over. In 2023, central banks will deliver the hikes they promised markets but no more. A few early hikers (in Latin America and Eastern Europe) will be able to cut. As inflation keeps falling and higher rates start biting, the debate will move from hikes to cuts, likely in 2H23. The US will lead the way, as the Federal Reserve hiked the quickest and the most and inflation is less energy-driven.

This macro environment naturally benefits credit. Spreads tightened since October, but levels are still attractive. High yield spreads imply 7% annual default rate, a level which only materialized in 2009. Distressed ratios are pricing a deep recession rather than a mild slowdown. Add that to falling inflation, and expected total returns look attractive. Historically, current levels of spreads tended to predict strong 12-months returns.

Within credit, we favor quality. Outflows have been strong across the board, and high rated credit tends to attract the earliest inflows when the tide turns. As growth slows and rates stabilize, investment grade and defensive sectors will outperform. Financials are set to benefit, given they are well represented in IG indexes and fundamentals are strong. Emerging market debt is interesting again (on a selective basis), as positioning is light and benefits from rates stability. China re-opening and bearish positioning in Europe means non-US assets will outperform.

Inflation | Pointing south

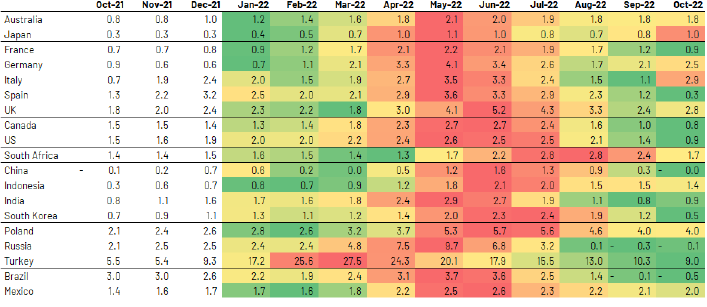

During 2022, global inflation rose from 2% to 10%. The jump was due to the combination of easy policy and supply shocks. In the past six months, both factors have reversed quickly, paving the way for disinflation in 2023.

In the US, supply pressures eased, as China’s covid policy stopped focusing on production. US PPI fell from almost 20% in June to just over 10% in October. Commodity prices eased too, as global chains have re-organized to gain independence from Russia. Broad commodities are 20% lower compared to their summer peaks, with oil 40% lower. Tighter policy plays a role too. In September, real rates spiked above 1%, the highest level since 2006. US money growth was 1% in 2022, down from 25% in 2021, and the lowest since 1994. Restrictive policy is finally impacting house prices (Chart 2).

Overall, early signs indicate that global inflation has peaked. Major economies have quarterly inflation down to January levels, pointing to a trend reversal at work since September (Chart 1). In the US, both headline and core inflation fell sharply in November. In Europe, the descent has been delayed by energy tariff hikes, but dropping gas prices means inflation will fall from January. Our own predictive models (Chart 3) see US inflation at 5% (with core just above 3%), and European inflation at 7% (with core just above 5%), by July 2023.

Data as of 23 November 2022. Source: Algebris Investments, Haver, Bloomberg Finance L.P. Note: 3m/3m headline inflation is calculated by dividing the average of the 3 previous headline CPI readings by the average of the respective 3 previous headline CPI readings. Note: For core YoY, the shading is based on a comparison of core YoY over the entire time period for each given country. Max red means highest core YoY, and max green means lowest core YoY, with yellow being the middle.

Rates | Cuts & holds

Inflation is slowing but monetary policy remains tight. Emerging markets started tightening meaningfully in 2021, and real rates are now excessive in several countries. Developed markets lagged by one year, but accelerated meaningfully over the summer. Excluding Japan, G-10 central banks have already completed 80% of their hiking cycles. The Bank of Canada has slowed down the pace of hikes, with the other G-10 central banks following in December. We see the Fed and ECB peaking, respectively, at 5% and 3% sometime in Q2. Inflation will stabilize above central bank’s target, so cuts in 2023 would be premature. A period of stable rates is a more likely the base scenario. In 2023, cuts will take place only in some emerging markets, mostly in Latin America. Looking at the relation between real rates and inflation (Chart 4), the US and Canada stand out as having the strongest cases for a pivot in the developed world, while Brazil, Colombia and Chile stand out in EM. The Euro Area and UK are the regions with most upside risk in rates.

Data as of 31 October 2022. Source: Algebris Investments, Bloomberg Finance L.P., Zillow, S&P. Note: Each plotted line shows the YoY change of the respective home price / rent index.

Chart 3 | More inflation downside in 2023

Data as of 24 November 2022. Source: Algebris Investments, Bloomberg Finance L.P, BLS, Eurostat. Note: Forecasts are based on a bottom-up approach that combines the forecasts of various sub-components of CPI (e.g. energy, rent) using multiple macro-economic and market-based variables.

Chart 4 | Strong pivot case in US, Canada, LatAm

Data as of November 2022. Source: Algebris Investments, Bloomberg Finance L.P, Citi

Macro | Next step easing

The case for 2023 hikes is weak because economies are slowing. High cost of living, tighter policy and the absence of China stimulus are pushing advanced economies towards a slowdown. In the US, consumer wealth accumulated during Covid helped in 2022, but will not support spending in 2023. Both PMIs and retail sales are pointing in this direction. In Europe, energy tariff hikes took place in 4Q22 and will bite in early 2023. European PMIs hover around 45, pointing to a slowdown but not a disastrous contraction. On the other hand, markets are pricing a deep recession, with US 2s10s having never been so inverted (-80bp). We expect the slowdown to be contained, with a bottom reached in the first half of 2023 and Asia re-opening helping in the second half. Growth in both the US and Europe is likely to stay close to 0% next year.

Markets | Bond anomaly unwind

A slower economy and slowing inflation mean upside in fixed income markets. Whilst it is not uncommon to see equity markets down as much as this year, 2022 was significantly anomalous for bonds (Chart 5). Flow data gives a similar picture, as capital left bonds at a much faster pace than it left equities, leaving positioning historically light. The past month has seen a strong rally in fixed income, but we think the best is yet to come. A few areas, such as IG credit, financial subordinated debt and emerging market debt remain cheap and under-owned. Historically, a slowing economy and lower US rates mean credit, Treasuries, EM debt and HY bonds outperform (Table 1). US equities, cyclicals and the dollar tend to underperform in that environment. To be clear, we do not believe markets are going back to the old world of zero yield. Inflation will stabilize at higher levels than the ones prevailing until 2021. However, the past few months have pushed fixed income to extreme levels, and macro stabilization can lead to a meaningful re-pricing in bond markets. Investors should take advantage.

Source: Algebris Investments, Bloomberg Finance L.P. Data as of 02 December 2022. Note: Accelerate/Slowing is defined by an increase/decrease in the annual GDP growth rate with respect to the prior year. Rising/Falling is defined by the difference between the interest rate in year t and t-1. Positive number = Rising, Negative number = Falling

Chart 5 | 2022 – bond anomaly

Data as of 2 December 2022. Source: Algebris Investments, FRED, Robert J Shiller, NYU Stern. Note: US equities – S&P 500 Index; US Treasury – 10y US Treasuries

FX | King Dollar steps down

2023 will bring US dollar weakness. On a real basis, the dollar has been stronger than it is now only in the mid-80s (Chart 6). US rates were much higher back then. Positioning is still crowded, while light on main funding currencies such as EUR, JPY, CNH. The Euro will continue to benefit from lower gas prices (Chart 7), a ‘better-than-expected’ recession in the Eurozone, and any upside from Russia-Ukraine negotiations. JPY will benefit from changes at the Bank of Japan, as a new Governor in April brings higher chances of exit from loose policy. Finally, the gradual re-opening in China may trigger equity inflows and benefit CNH. A less hawkish Fed together with better-than-expected macro in Europe and China will be negative for USD and positive for non-US assets in 2023.

Source: Algebris Investments, Goldman Sachs.

Data as of 15 November 2022. Note: GS USD Real Trade Weighted Index.

Source: Algebris Investments, Bloomberg Finance L.P. Data as of 21 November 2022. Note: Dutch TTF Natural Future Gas used (TZT1 Comdty)

Source: Wind, National Health Commission, as of 28 November 2022. Note: Total daily new positive cases reported by China’s National Health Commission, which is the sum of daily new asymptomatic cases and daily new confirmed cases.

China | Getting out

In China, authorities are slowly loosening the very strict Covid restrictions in place since 2020. In the aftermath of the October Party Congress, testing and quarantine restrictions were eased. As a result, Covid cases skyrocketed again (Chart 8), crossing April highs. The process slowed down, triggering wide protests and a subsequent re-loosening. Re-opening over the next few months seems inevitable. China has been the only country with strict restrictions for more than a year now, and consumption remains subdued, as highlighted by recent PMIs well below trend. Export growth in 3Q22 has been the lowest ever since 2020. Economically, incentives to re-open have never been so strong, and post Congress, the political cost has reduced. However, the process will be bumpy. Exit from zero-Covid policy means more local waves and stop-and-go episodes. The path to re-opening will therefore be intermittent, and we do not expect a full re-opening before summer 2023. China re-opening while the US slows down means a rising gap in relative growth. If China could reach 5% growth in 2023, the gap could be close to 500bp, the highest level since 2013.

Ukraine | Stalemate

Ukraine remains the biggest unknown for 2023, but also the biggest upside risk. Both the war and negotiations appear to be at a stalemate, hence market expectations are low. As of late November, territory liberated by Ukrainian forces is roughly as large as the portion of East Ukraine having been conquered by Russia. As a result, neither is close to prevailing. US-Russia contacts intensified recently, but the US is in no rush to reach a deal, especially as the G7 is intensifying sanctions via oil price caps. On the other hand, Putin is publicly open about a deal, given the lack of alternative solutions. In November, President Zelensky detailed a 10-point peace plan. Most points are unacceptable to Russia, but Ukraine never opened to a non-military solution before. The situation remains deadlocked, but all parties are displaying a higher appetite for a discussion. Russia’s position becomes weaker over time, as European energy dependence from Russia falls. A resolution is not around the corner, but signs are emerging, and markets are priced for a protracted war.

Source: https://www.ft.com/content/4351d5b0-0888-4b47-9368-6bc4dfbccbf5

Data as of 24 November 2022

Davide Serra

Founder & CEO

Sebastiano Pirro

CIO & Financial Credit Portfolio Manager

Gabriele Foà

Global Credit Portfolio Manager

Silvia Merler

Head of ESG & Policy Research