Looking at the evolution of US rates, one may think the world has changed in just three months. In October, market priced 5% Fed funds rates by end-2024, and US high-yield spreads implied 6% default rates. Now, market stands around 4% rates, and spreads normalized.

The pricing for 2024 has shifted from no landing and potential credit stress to a comforting soft landing (Chart 1), a scenario where central banks cut despite healthy growth. Markets decided we now live in a land of doves.

In fact, data have changed little. US core inflation is just below 4%, like in October. Activity slowed, but leading indicators point to a re-acceleration. Labor markets are tight and there is only modest sign of loosening, despite lower growth. Our macro models suggest US core in mid-2% by year end, despite real GDP growth trailing 3%.

The US macro environment is consistent with three cuts in 2024, and terminal rate reached in 2025 somewhere between 3.5% and 4%. We held this view in October, when it was a dovish one. We hold the same view today, but it calls for a more cautious positioning.

Risks around our view are skewed on the upside for rates. Credit spreads and long-end yields have done some of the Fed’s job, and financial conditions have eased substantially in 4Q23. The US has been running persistent fiscal deficits since 2020, and high rates make them costly. The US election outcome is uncertain, but budget pressure is a certainty. Bond vigilantes may be on the look-out soon enough.

Opportunities are still plenty in credit, they are just harder to find. As the 2024 cuts trade played out before the year even started, we turn cautious on duration and beta. Investor focus should be on alpha. 10% of global bond markets yield above 7% in EUR, while 50% yield less than cash. Active credit selection is thus required. We see value in selected areas of corporate credit, subordinated financial debt, and emerging markets.

Source: Algebris Investments, Bloomberg Finance L.P. Data as of 13.02.24. Note: implied landing odds from SFRZ4 options.

Fed Pricing | Recession cuts at odds with data

The market is now pricing five Fed cuts in 2024, and a terminal rate of 3.5% to be reached in late 2025 (Chart 2). We think cuts could be slower and fewer. The US is trailing growth close to 3%, hence it is unlikely to grow below trend in 2024. If anything, the risk is on the upside, as soft indicators continue to beat (Chart 5). We are thus in a context of disinflation and solid growth, rather than through an economic adjustment. Historically, the former type of episode led to far less dramatic cuts than the latter (Chart 4). Additionally, long-end yields and credit spreads have already started doing the Fed’s job (Chart 3). We see three cuts in 2024 as appropriate.

Source: Algebris Investments, Bloomberg Finance L.P., Federal Reserve Bank of New York.

Data as of 06.02.24

Source: Algebris Investments, Bloomberg Finance L.P. Data as of 06.02.24

Source: Algebris Investments, Bloomberg Finance L.P. Data as of 19.01.24. Average of cuts in Fed Funds rate since the first cut during given 1998, 2001, 2007 and 2019 recessionary periods vs in 1995 and 1998

Source: Algebris Investments, Bloomberg Finance L.P., Citibank, Data as of 05.02.24

R Star | Data point to upside risks

Terminal rates may also be higher than perceived. The ongoing disinflation has left the US unemployment rate unscathed (Chart 6), unlike previous episodes. This points to the economy being able to tolerate higher levels of real interest rates than before. The surprisingly little amount of credit stress following 2022-23 hikes point in the same direction. The Fed’s own estimates of neutral rates have been revised higher steadily since 2010, to be adjusted lower only as models have been twisted to allow for Covid supply shocks (Chart 7). Strong data means markets could realize pre-QE estimates are not that obsolete. The 2.5% pre-QE estimate would imply 4.5% Fed funds.

Europe | The weak link

European data display a much softer picture. A deep recession was avoided in 2022, but gas-induced disruptions have impaired the manufacturing sector, which failed to recover in 2023. Sticky wages mean inflation ate into household finances, in a context of tight financial conditions. Germany continued to self-constrain fiscal spending and run a primary balance in 2023, which stands in stark contrast to the generous US deficits. As a result, US and European macro suddenly de-synchronized last year (Chart 8). Europe is trailing 0% growth. The ECB should cut before the Fed, and more deeply. The central bank’s own estimate of neutral rates is just slightly positive, and stable over time. The Governing Council will be patient to try and wait for Fed cuts, but we see chances it will be forced to move ahead faster, at the cost of weakening the currency.

Source: Algebris Investments, Bloomberg Finance L.P.. Data as of 06.02.24 Note: Unemployment Rate: USURTOT Index; values on the Y axis refer to CPI YOY Index on the left, Unemployment Rate on the right.

Chart 7 | Fed estimate of neutral rate keeps moving higher

Source: Algebris Investments, Federal Reserve Bank of New York. Data as of 06.02.24

Chart 8 | EZ macro falling behind

Source: Algebris Investments, Bloomberg Finance L.P, Citibank. Data as of 06.02.24

US Fiscal | Bond vigilantes on the lookout

Fiscal policy adds to market vulnerabilities. US deficits turned persistent post 2020 (Chart 9), as large infrastructure spending substituted for income support. In 2023, the US ran a 7% deficit, despite growth north of 2%. Pro-cyclical spending doesn’t bode well for debt dynamics. Fed hikes also didn’t help: interest costs now represent 11% of US government spending. It was below 6% in 2020. Interest rate pressure on public finances is likely to stay, as terminal rates will be higher in 2025 than in 2020 and curves may steepen. US elections are another source of risk, especially as current Trump plans project $6tn of deficits in excess of the Biden platform. Fiscal news started impacting the bond market in the past two years (eg the Truss budget in UK, or the US borrowing plan in summer 2023), after not having done so for ten years. Bond vigilantes may soon raise their head again as US elections approach.

Risk markets | Limited value in beta

Market beta rallied since October and now has little value. Credit spreads are back to pre-gas crisis levels (Chart 10). High-yield CDS rallied 150-200bp since October, and now imply default rates of 4% per year, not an excessive risk premium. Capital markets are wide open. Global corporates sold $150bn of investment-grade debt in January. US high-yield issuance was $36bn in January, 40% above January 2022. New deals in Latin America and Africa are booming. Inflows into IG bonds and equities continue unabated. Both bond and equity volatility are back to pre-Ukraine levels (Chart 11), suggesting markets have priced out tails both on rates and growth. Couple euphoric risk assets with five cuts implicit in US rates, and markets look priced for perfection. As a result, we see market beta vulnerable to a correction.

Source: Algebris Investments, Bloomberg Finance L.P.. Data as of 06.02.24 Note: Bloomberg Contributor Composite Forecasts for dotted bars.

Chart 10 | Credit spreads well below 5y average

Source: Algebris Investments, Bloomberg Finance L.P.. Data as of 06.02.24 Note: EU HY: ITRX XOVER CDSI GEN 5Y, EU IG: ITRX EUR CDSI GEN 5Y, US HY: CDX HY CDSI GEN 5Y SPRD, US IG: CDX IG CDSI GEN 5Y

Chart 11 | Tail risk has been priced out

Source: Algebris Investments, Bloomberg Finance L.P.. Data as of 06.02.24 Note: values on the Y axis refer to MOVE Index on the left, VIX Index on the right

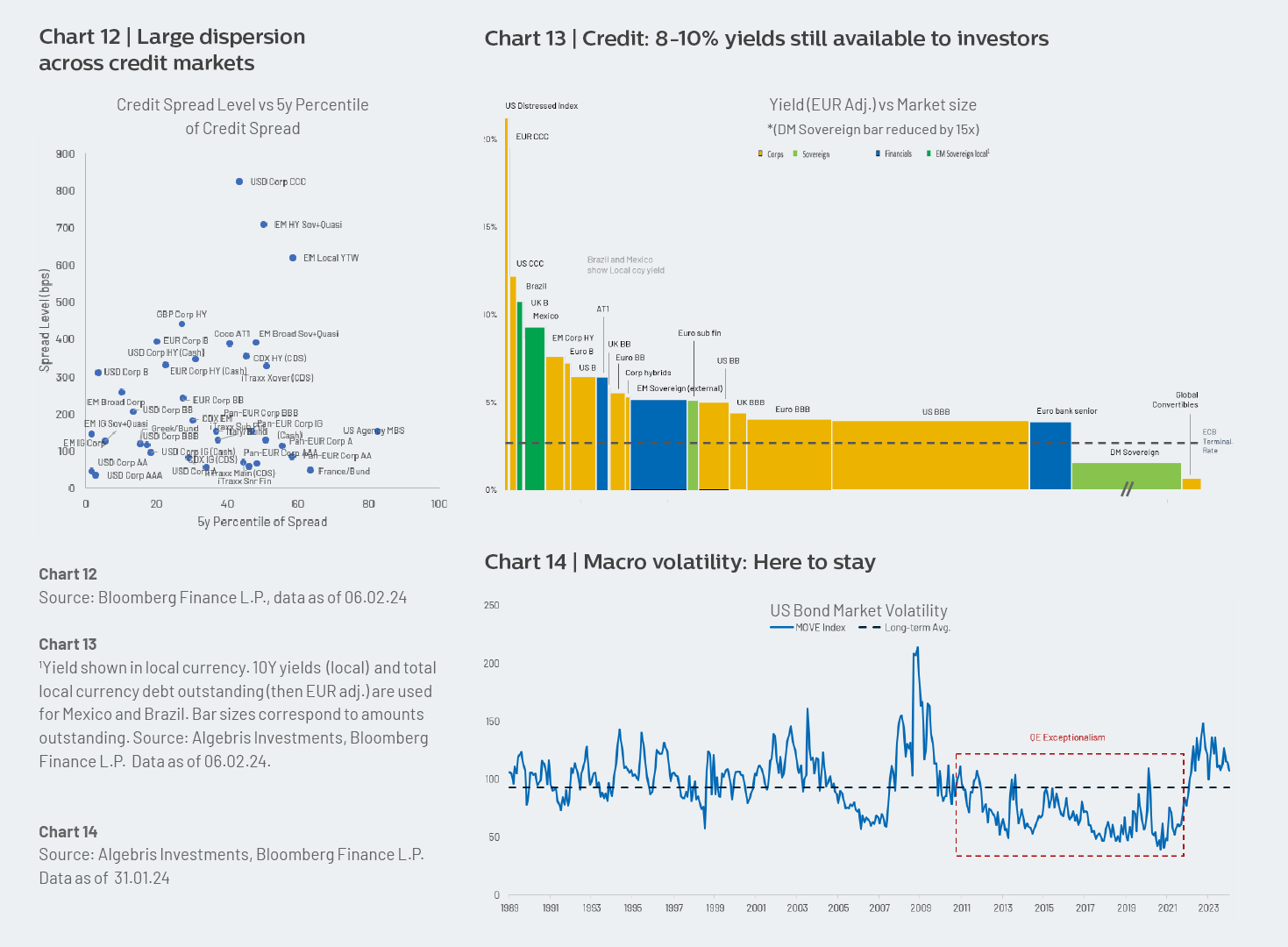

Credit | Value lies in alpha

Broad markets rallied, but some areas of credit still offer value. In fact, a few segments still need to re-gain market access (Chart 12). While index buyers are now vulnerable to market risk, bond pickers face a large set of bonds that still yield 9%+ (Chart 13). Investors should focus on these areas, while looking for protection in flow credit and rates. One example is real estate, where the market is neither distinguishing between commercial and residential nor by credit quality. We see value in junior debt of high quality Northern European issuers. In EM, selected local markets still offer 6% real yields despite their ability to cut rates. High-yield sovereigns are still paying 11-15% despite some making large adjustment steps. Subordinated debt of European banks is still too wide to high-yield despite large capital buffers. Credit markets still offer great bargains, but, as opposed to late October, one must be able to spot the right opportunities.

Source: Bloomberg Finance L.P., data as of 06.02.24

Chart 13 | Credit: 8-10% yields still available to investors

1Yield shown in local currency. 10Y yields (local) and total local currency debt outstanding (then EUR adj.) are used for Mexico and Brazil. Bar sizes correspond to amounts outstanding. Source: Algebris Investments, Bloomberg Finance L.P. Data as of 06.02.24.

Chart 14 | Macro volatility: Here to stay

Source: Algebris Investments, Bloomberg Finance L.P. Data as of 31.01.24

Macro volatility | Here to stay

The next three to five years will be very different from the previous ten in fixed income markets. Market pricing has shifted enormously in just three months, underscoring very high latent macro volatility. This is a key natural feature of rates markets, that was hidden for many years during QE (Chart 14). The 2022 inflation marked the end of this era, and a return of macro volatility. As a result, passive investing in fixed income won’t work well going forward as it has in the past. A flexible and active approach to bond investing will make a significant long-term difference for investors’ returns.

Davide Serra

Founder & CEO

Sebastiano Pirro

CIO & Financial Credit Portfolio Manager

Gabriele Foà

Global Credit Portfolio Manager

Silvia Merler

Head of ESG & Policy Research