“All you need is faith, trust, and a little pixie dust.”

– Peter Pan

If you are a bond investor, you have two options. You can either lose money quickly, or slowly.

The recovery is solid, especially in the United States. Demand is extending from goods to services, job gains are broadening and wages are up. Central banks, however, are stuck in a dilemma. For two decades, they have manipulated interest rates down in the attempt to kickstart faster growth and inflation through an asset-price driven wealth effect. This was necessary but not sufficient to achieve their goals. In many economies, governments were pulling the austerity handbrake while central banks were pushing down the monetary accelerator. Today, bottom-up fiscal support to incomes and infrastructure stimulus have filled the tank with rocket fuel, generating a record bounce in growth and inflation. As fiscal stimulus fades next year, the question is – will inflation stay?

The short answer is yes. Structural drivers of low inflation are fading: globalization, geopolitical stability, just-in-time supply chains and the assumption that natural resources are unlimited are proving unsustainable. Supply bottlenecks are likely to persist over the coming quarters. Consumer demand is picking up too. Against this, the Fed’s reaction function appears behind the curve. One fear is hiking too early might turn out to look like a mistake, should Covid variants spread again. Withdrawing stimulus also risks political criticism, as many economists argue the Fed should run the economy hot until every last unemployed citizen is back to work. But underlying this logic is the assumption that a monetary one-size-fits-all approach could work to fix all economic ills – from improving minority unemployment to stagnant productivity or even climate change.

Printing money isn’t a free lunch. It has generated inequalities across corporates and society. As a recent Jackson Hole paper by Main, Straub and Sufi suggests, these inequalities are, in part, the cause of declining productivity and secular stagnation. The rich get richer, and rates get lower. Investors know this well: we are left paying for the side effects of this monetary and fiscal experiment. Holding gilts over a decade means losing a quarter of your capital, using current break-evens as an indication of future inflation. Holders of US Treasuries would give up fifteen percent, and buyers of Italy’s debt would lose ten percent. Financial repression is here.

As the era of goldilocks ends, central bankers are taking us on a last ride to never never land. What’s holding everything together – the pixie dust sustaining current market valuations – is deeply negative real rates. This won’t change overnight: central banks are trapped by asset bubbles of their own creation. The room for error, however, is much smaller. Enjoy the ride – but prepare for volatility with alternatives to long-only fixed income, and with alpha.

Not-So-Transitory Inflation

The consensus central bank view is that current inflationary pressures are transitory. On the surface, data supports this view: price increases are concentrated in goods under shortage. However, a deeper look at hard and soft indicators shows that price pressures are broadening, and that demand is “very, very strong” – to cite J. Powell – and moving from goods to services. Jobs are recovering more rapidly, too. However, fiscal stimulus might decelerate next year. How will these cross-currents evolve next year?

The supply-side constraints: likely to extend in to 2022

- Supply chain disruptions: The supply chain disruptions caused by Covid will likely extend into 2022. Firstly, because of persistence in the shortage of the principal component: chips. Since the start of the chip shortage, semi-conductor foundries have continuously extended their estimate of when the shortage will end. Most recently the CEO of Intel has said its likely the shortage will extend into 2023. Secondly, there are continued delays in delivering the final end product. The lead times for deliveries, as shown in the chart to the side, has now risen to a new all-time high of 21 weeks. In part this has been exacerbated by a shortage of containers and ships. The rates for shipping between China and the US are starting to show some signs of normalization, but remain elevated and well above pre-Covid levels. The CEO of Maersk recently said he expects shipping constrains to remain into 2022 and a Maersk executive added that the main solution they saw was for consumer demand to abate.

- Labour shortages: Labour shortages should, at the very least, last over the winter. There are two drivers of the labour shortage today. Firstly, shorter term issues: for example, lower participation of women during Covid and furlough schemes that may have disincentivized some workers. These two issues should gradually resolve, though could extend over the winter given some Covid concerns. Secondly, longer term or more structural issues: for example, an exodus of labour from low paying hospitality jobs. Labour costs in hospitality are likely to remain a challenge: according to a poll over 1 in 3 former hospitality workers say they are not considering re-entering the industry and half of those not returning said a pay increase would not change their view.

- Structural onshoring: The chip and shipping shortage has highlighted the risks of offshoring to the global supply chain. We expect increased onshoring of supply chains around strategic manufacturing goods – both as a lesson-learned from Covid, as well as a way to protect intellectual property in an environment of rising geopolitical risk. This de-globalization trend will increase robustness of supply chains, but will likely increase production costs and potentially inflation. The OECD had estimated that the advent of globalization in the late 1990s decreased CPI by between a 0-0.25% per year, in OECD countries.

The demand-side boom: lower than 2021, but higher than pre-covid

- Pent up savings: Consumer spending will moderate vs 2021 levels but remain above pre-Covid levels, boosted by still high saving rates. During Covid, saving rates increased substantially both as a result of stay-at-home policies as well as unprecedented fiscal support, including direct cash transfers to people. While a significant portion of this excess savings was spent, especially amongst lower income demographics, it remains above pre-Covid levels. This is especially the case in the UK and Europe, and to some extent the US.

- Fiscal stimulus: As with consumer spending, government spending will remain above pre-Covid levels. In the US, progress on new fiscal stimulus has stalled; a final infrastructure package may be under $2tr and spent over several years. However, the US is unlikely to return to a balanced budget any time soon. Historically, large US deficits take between 4- 7 years to close, implying at least another 2 years of spending above 2019 levels. In Europe, Covid fiscal stimulus lagged its DM peers: European fiscal deficit was -7% GDP in 2020 vs -14% GDP in the US and UK. This may imply that Europe will be slower than its peers to close its fiscal gap. In fact, of the EUR 750bn EU Next Generation Fund, only 13% has been spent in 2021 with the remainder to be spent over 2022-2023.

- Green infrastructure: The transition to Green Infrastructure will create additional demand for raw material and labour. According to GS research, to meet global green-goals (net zero, clean water) $6tr in annual green capital expenditure is required for the next decade, up from around $3.2tr invested per year between 2016 and 2020. While annual capex may not reach $6tr it is likely to be higher than the pre-Covid levels, as emphasized by the $0.5tr green infrastructure spending as part President Biden’s $1.75tr infrastructure package.

Central Bankers’ Reaction Functions and the Dilemma of the Not-So-Transitory Inflation

Central banks have been behind the curve in acknowledging inflationary risks.

Almost in a “five stages of grief” fashion, the Fed’s and ECB’s narrative has shifted from denying inflation pressures outright (both), to arguing that households would not notice (Fed), to finally acknowledging it and stating the institutions are “soul-searching” and need to understand these transmission channels better (ECB).

That said, central banks are facing a dilemma. On the one hand, withdrawing emergency stimulus might look like a policy mistake, should Covid variants kick in again. On the other hand, persistent negative real rates are unwarranted given the current level of price increases and job gains and might lead to misallocation of resources and asset bubbles later on.

So far, the fastest to act have been the central banks in commodity-exporting economies with accelerating house prices: the Reserve Bank of New Zealand (RBNZ), the Reserve Bank of Australia (RBA) and the Bank of Canada (BoC). Their actions have included hiking rates (RBNZ), abruptly ending asset purchases (BoC) and signalling an end to yield-curve-control (RBA).

The Fed, the ECB and the Bank of England in particular, remain in denial.

The Fed has been slightly slower but is now acknowledging inflation and signalling to act, albeit gradually. In its tapering announcement in November, J. Powell pushed back on the idea that maximum employment was near. However, recent jobs data shows both job creation and wages are improving – while workforce participation remains sluggish. This suggests a tighter labour market than pre-Covid, and we expect the Fed to acknowledge that in the first half of next year.

At the ECB press conference in October, Lagarde unsuccessfully talked down the market implied odds of hikes in 2022, arguing the ECB was actively discussing inflation, but reiterating the ECB view that inflationary pressures are transitory – albeit for longer than anticipated.

The Bank of England has perhaps shown the least consistency in discussing inflation trends. Today, the UK shows the most negative interest rates against expected inflation across developed markets. Not only is inflation rising from a strong recovery, but also from structural bottlenecks in goods and labour markets, which are unlikely to disappear unless Brexit is overturned. The BoE first talked rates up and signalled a hike this year, even before the end of its asset purchase programme, and then delivered nothing.

There is, however, a price for financial repression, negative real rates and credibility – and that is the loss of credibility. We expect the Fed to start hiking in mid-2022, the BoE to deliver 1-2 hikes next year, and the ECB to wait until 2023.

The Anti-Goldilocks Portfolio

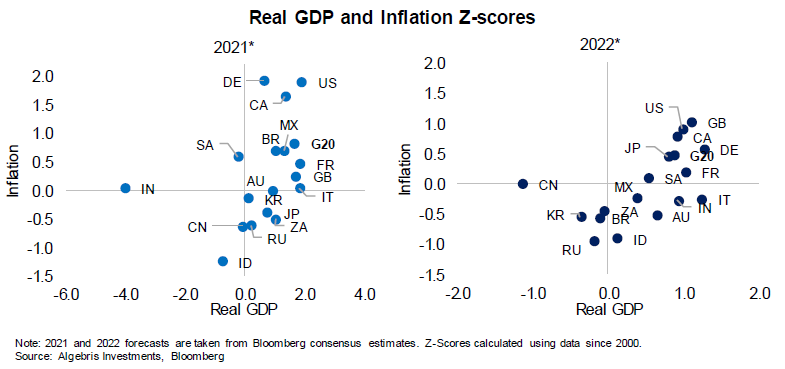

Global inflation surprises remain strong, while economic data is deteriorating. The market has entered a debate on whether 2022 will be characterized by stagflation. While the “S” word may be a bit strong: data suggests we are not in stagnation. US and European growth remains strong – with the UK the only exceptional candidate for stagflation, due to self-imposed bottlenecks. However, markets are likely to move away from the goldilocks environment experienced over the past decades, made of strong growth and low inflation. A stagflation-lite environment would be bad for bonds and stocks, making asset allocation difficult.

From reflation to stagflation

2021 started with big hopes for economic reopening and growth-led reflation. As the global economy bounced back from the worst recession in three decades, real growth picked up strongly. With massive fiscal and monetary policies supporting incomes, inflation bounced back too. In 2021, global growth will hover around +6%, the highest in 20 years. 10y inflation break-evens in the US moved from 1.6% to 2.7% in the past 12 months, reaching a two-decade record. In fact, most countries globally displayed both growth and inflation substantially above their 20y averages, led by the US. In summer though, clouds appeared on the horizon. Covid variants made the reopening process bumpy, the China property crackdown opens risks for global growth, and supply / commodity bottlenecks darkened the outlook for consumers: economic surprises turned negative, together with a slowdown in ISM/PMI surveys, indicating a loss of momentum. Despite these economic bumps, inflation remains strong. US CPI spent the past 6 months above 5%, and Europe hovers around 3%. Emerging markets see peaks of 7-10%, with less credible – or more proactive – central banks forced into hikes. Global inflation breakevens are higher than summer level despite growth forecasts being much lower. In 2022, most countries will likely see persistent inflation and slightly lower growth than this year.

Away from goldilocks

Are stagflation fears exaggerated? It is true that we are far from a 1970s-like context, both structurally and cyclically. After all, 2022 should still see global growth above 4%, a newly approved $1.2tn infrastructure stimulus in the US, and still above 5% growth in China. That said, there are some headwinds on the horizon. As fiscal stimulus gradually fades, consumer demand will need to step in: this is starting to happen in the US, as shown by recent ISM data. One major risk remains China’s crackdown on credit and property, which is now spreading well beyond the Evergrande group. So far, Chinese policymakers have moved from hawkish to tentative support measures, but we would expect more easing next year, in light of the upcoming National People’s Congress.

The result is a context with slower growth momentum but persistent inflation. This poses a dilemma for both central bankers – which we will discuss below – and for investors.

The anti-goldilocks portfolio

Asset allocation in a stagflation environment is harder than usual. When growth and inflation slow, investors should focus on bonds. When the economy reflates, equities tend to outperform. In stagflation, there’s no right choice. In an anti-goldilocks environment, investors are better off moving away from traditional asset allocation blocks and focusing on more specific investments or ad-hoc solutions. In the past century, stagflation periods have been concentrated between 1960 and 1980, when supply limitations hit commodity markets in various waves, which in turn hit growth. In those instances, real estate, commodities and volatility were among the few places to hide. Equities tend to be rangebound, with value typically outperforming growth. Among the losers, bonds are in a worse position than equities, due to less favorable initial conditions: surprisingly, the level of initial yields remains still the major long term driver of returns in bond markets.

Commodities and real assets

In the 70s, political noise over the Suez Canal turned into a massive supply squeeze in energy markets. The picture is relatively similar today, with the squeeze coming from supply disruptions related to the pandemic. Supply limitations took a decent toll on gas and energy prices in the past months, and may persist for longer than expected, with Opec+ leaning against output increases. Production bottlenecks in Asia take time to resolve, and the backlog of 2020-21 orders affects time to market. In energy markets, Russian gas may flow back to Europe only slowly, as politics adds up to physical limitations. OPEC+ is also in no rush to ease market pressure, as larger producers benefit from higher oil prices. So, the commodity rally may not sustain recent momentum, but supply squeezes will support high levels in the coming months. Energy and commodities assets will thus keep performing, and remain relatively cheap. Energy stocks in Europe are up 25% YTD, vs oil and natural gas, respectively at 70% and 140%. The energy index is one of the few still below pre-Covid highs, despite energy commodities being all through the highs. In credit, HY energy names have been lagging, and offer 5-9% yields (depending on jurisdictions/subsector) despite improving balance sheets. Commodity-linked currencies, such as the Norway Krona or the Russian Ruble, are performing but still cheap to what their oil beta would imply.

Misery means volatility

Stagflation tends to raise market volatility, as higher inflation and low growth compound. The “misery index”, which combines unemployment and inflation, shows a tight correlation with cross-asset volatility during the 15 years between 1970 and 1984, a time characterized by high inflation, growth concerns and rallying commodities. The index was subdued during the 90s and 2000s, but is coming back up sharply in 2021. After 10 years of QE, markets are not used to volatility. Since 2010, rates and equity volatility has remained subdued, with only occasional spikes. Volatility has been concentrated in a few “bad days”, which soon turned into an opportunity to buy risk, especially in credit. A high volatility regime naturally favors flexibility and less reliance of market direction, at the expense of market beta.

Alpha is back

High volatility means high dispersion, which raises the value of alpha or asset picking within asset classes. This is especially true in an environment where both equities and rates suffer, and hence the value of beta is limited. With stagflation, energy, consumer and healthcare tend to deliver positive equity returns, while tech, industrials and materials tend to suffer. Financials and utilities are more mixed as slow growth offsets high rates. At a country level, energy importers and countries that heavily rely on borrowing abroad, like Turkey, tend to suffer, while energy exporters with a solid external picture, like Russia or S. Africa, tend to fare better. Thorough country and sector selection is thus more important than usual.

Conclusions: Stay Defensive on Paper Assets, Buy Upside on Real Assets

The recovery is solid, particularly in the United States and Continental Europe. We expect a turn towards bottom-up stimulus from China, where policymakers are positioning for a long-term game. This is likely to come not in the form of large-scale rate cuts and QE, but rather with topical policy decisions to support the housing market and services.

Against this backdrop, we expect inflation to stay elevated – as we have argued since earlier in the year – due to persistent supply bottlenecks and a pick-up in demand, combined with economic reopening and new measures to combat Covid.

If this view is correct, then many Western central banks remain behind the curve – the Fed for one, as well as the Bank of England, and the European Central Bank. The dilemma is that these institutions have trapped themselves in an asset-bubble of their own creation. Whether it is stock valuations in the US, property in the UK or BTP yields in the Eurozone, central banks won’t be able to accept a prolonged negative price action.

For investors, this means interest rates will remain persistently below inflation. At the same time, the structural drivers of low inflation over the past decades – globalization, geopolitical stability and the ability to consume planetary resources without caring for the environmental cost – are changing rapidly.

As a result, we are positioned defensively in paper assets. Our longs in government bonds and credit are selective and with limited duration, yet still yielding substantially more than inflation. At the same time, we are positioned for upside convexity in instruments backed by real assets: convertible debt, equities and commodities.