We think Elizabeth Warren will likely win the Democratic primaries, and may have a substantial probability of beating Donald Trump in the U.S 2020 Presidential elections. We are still at the very early stages in the race, and there is no guarantee of a Warren win, however, there could be very disruptive consequences to markets if this outcome were to materialise.

As the US and the global economy slow, we take three lessons from recent policy and political shifts around the world – pointing us in this direction.

1. Monetary policy is stretching its limits.

The unintended consequences of easing and negative interest rates are growing, like impaired banking systems and asset bubbles. The marginal impact of easing is increasingly to absorb the left tail of economic risk, but not enough to make the economy accelerate.

2. Trade uncertainty is backfiring.

Even a short-lived rise in unemployment is enough to change consumer behaviour. While financial markets stay up thanks to low interest rates, business investment on Main Street has slowed due to persistent uncertainty. History shows that three consecutive months of rising unemployment typically thwart consumer spending: so far this hasn’t happened, yet the pace of hiring has slowed. In addition, people are increasingly worried about the likelihood of a recession, as Google data shows.

3. Time is up for populists.

After a brief honeymoon with populism, voters may be shifting towards politicians with a more pragmatic framework. Greece is a case in point of a failed populist experiment, where the country lost a quarter of its GDP during the crisis and under Tspiras’ government. Following this year’s election of PM Mitsotakis, Greece is now the Eurozone country with the highest PMI, while GGB yield are now close to investment grade levels. In Italy, the Northern League and Five Star Movement, who promised free pensions and lower taxes, were sidelined by a more moderate and pro-reform coalition last summer. Ukraine is also on a positive path, as new President Zelensky has been appointed on an anti-corruption platform.

Of course, three examples do not make a trend. However, the recent decline in Trump’s popularity, vis a vis the slowdown in the US economy may suggest that American voters, too, may soon realise the inefficacy of quick-fix policies, and look elsewhere for solutions.

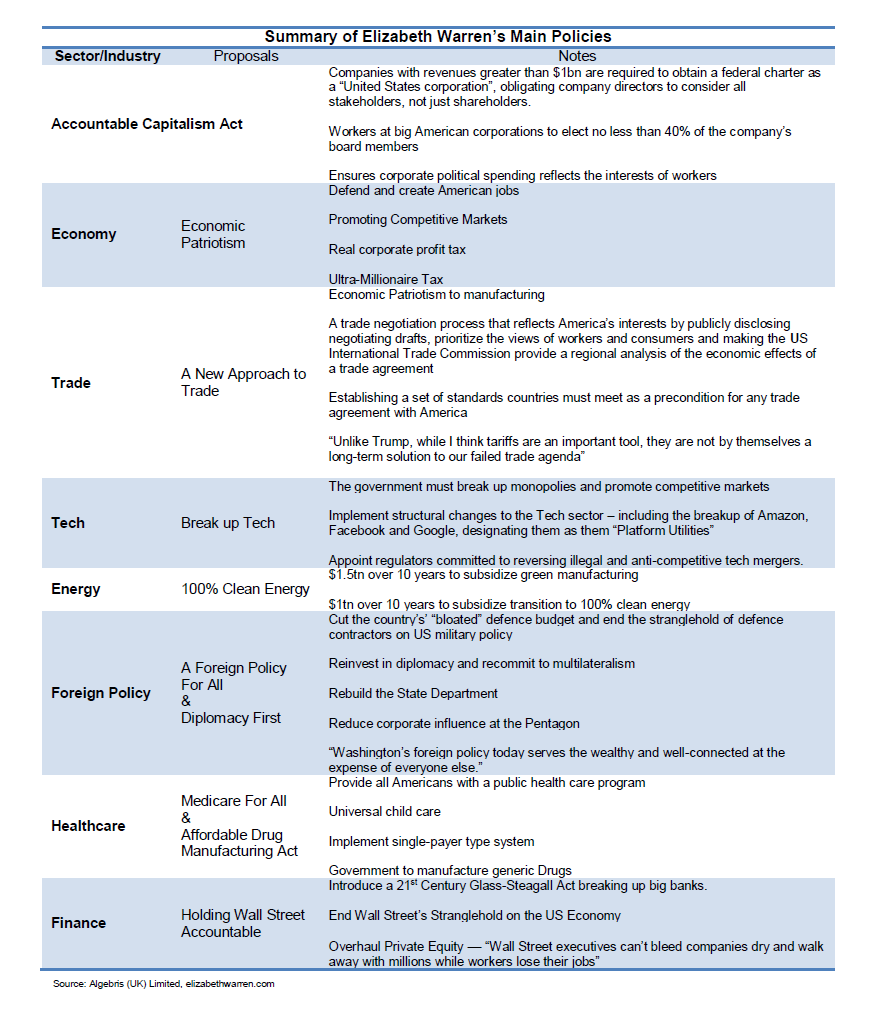

Elizabeth Warren is the most promising Democratic candidate, in our view, and the only one who would be able to shake up the U.S. economy from its structural issues. With Joe Biden marred by his recent corruption scandal and Bernie Sanders suffering from health issues, Senator Warren is also the most likely candidate, according to the most recent polls for the Democratic primaries.

How would the US and global economy fare under President Warren?

Most investors see a potential Elizabeth Warren win as a negative for markets and the economy. While that may be true, the long-lasting effects on growth and productivity may be positive.

Elizabeth Warren’s economic plans focus on pre-distribution as well as redistribution, on rebalancing the economic system to improve long term productivity and reduce inequality.

She favours the break-up of monopolies, including in the finance and tech industries, which have been a strong contributing factor to the decline in productivity over recent decades (see also The Myth of Capitalism). At the same time Warren would promote investment in infrastructure, where the U.S. spends less than Europe and China, education, and would introduce a wealth tax on the richest households.

While feared on Wall Street for her tax proposals, we think this package of measures could actually have positive long term consequences (see also Central Banks have broken Capitalism).

The result may be a mirror image of Trump’s presidency, which started with a sugar-rush fiscal stimulus, but ended with little progress on structural reforms, infrastructure investment and trade.

Which President would China prefer to deal with?

There are two schools of thought on whether the Chinese may prefer to deal with President Trump or President Warren ? and what this means for trade negotiations.

On the one hand, some believe that a weakened President Trump may be considered a “paper tiger” by the Chinese, and that China’s incentive may be not to give an inch to Trump now, as he may not be there next year.

On the other hand, people who have been closer to the President, which we met recently in New York, believe China’s incentive may be to actually keep Trump in office ? through a small deal rather than a comprehensive one? given Warren’s tougher stance on human rights and environmental regulation.

In any case, we think a mini-deal including a delay in the October tariffs and some purchases of agricultural goods, may cause a short squeeze in markets, but will not be enough to reverse the declining trend in manufacturing and business investment.

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.