“Always make the audience suffer as much as possible.”

Alfred Hitchcock

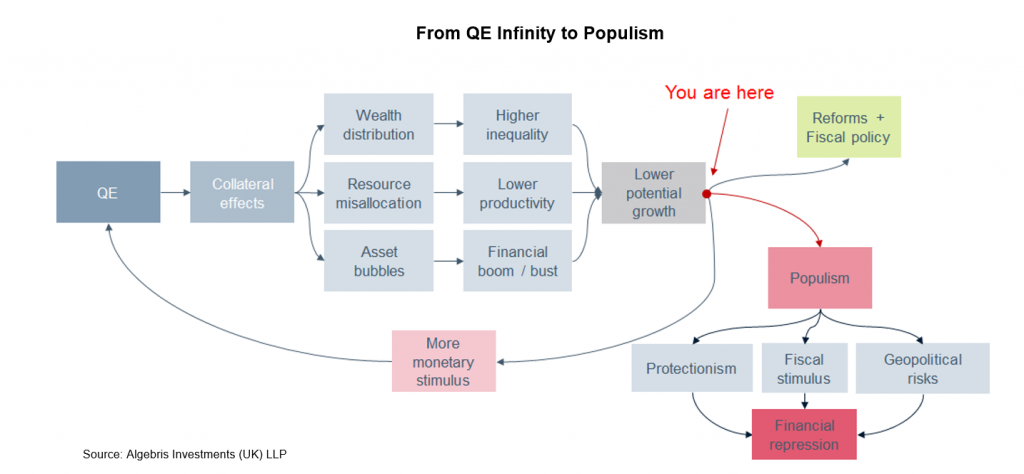

As 2016 draws to a close, the sensation is similar to being spectators of a Hitchcock movie. The curtains of QE stimulus slowly come off, and all of a sudden the political and social tensions that had been building up over the past eight years of crisis come to the fore, all at once. There are three main actors we see playing in 2017:

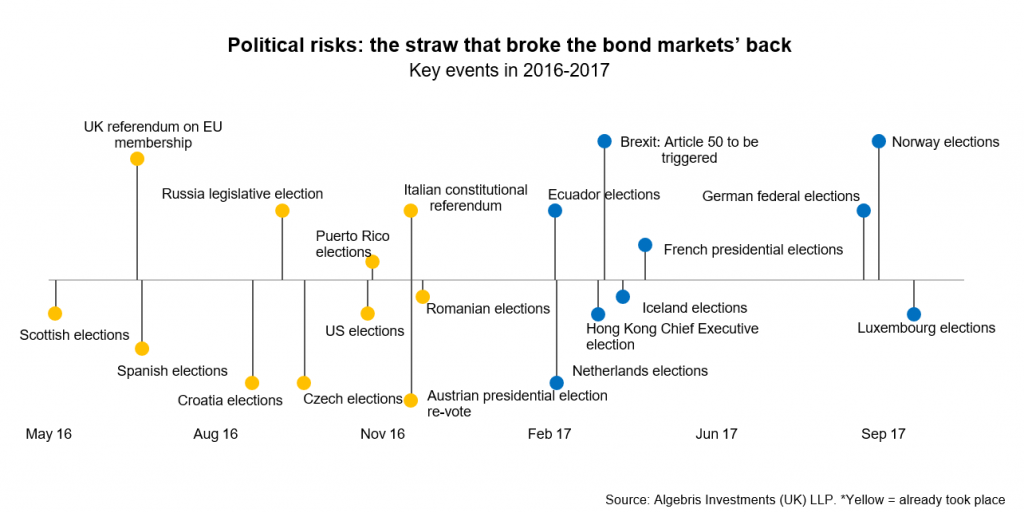

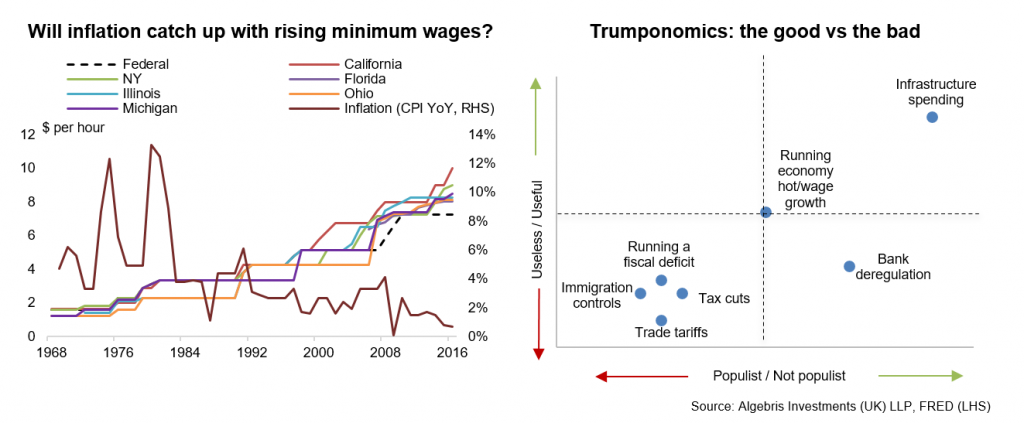

The first one is populism. We have been flagging the rise of inequality within developed countries for years, yet only a few investors cared in the past. This year, inequality has provided fertile ground to Trump, Brexit and No votes in the US, UK and Italy. Next year Europe will face four elections: in Italy, the Netherlands, France and Germany. The emergence of protest politics will mean more fiscal stimulus, protectionism (trade tariffs, curbs to migration) and rising geopolitical risks.

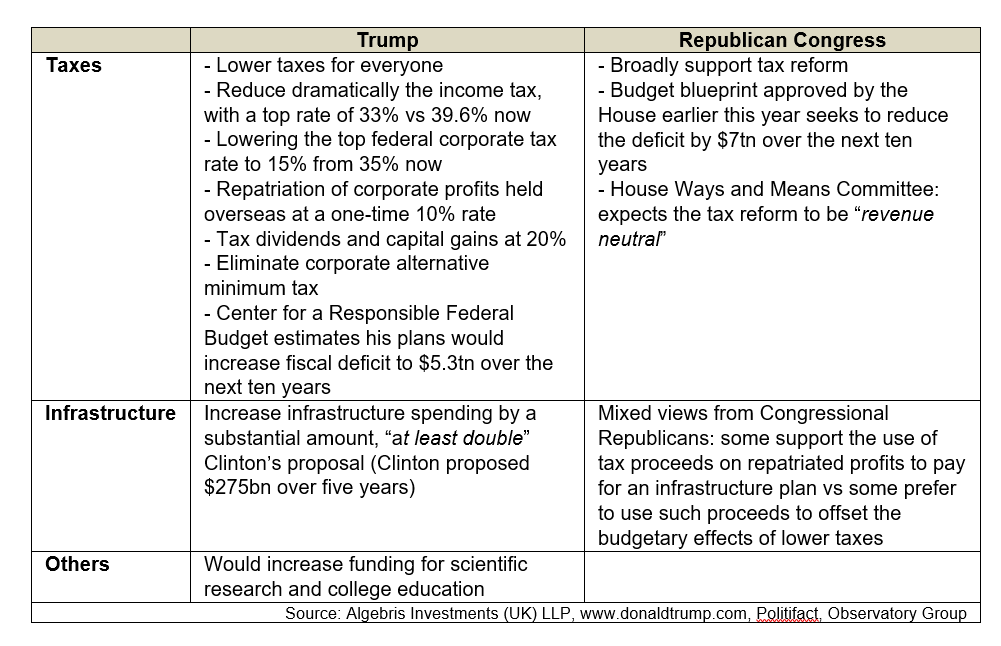

The second actor is fiscal stimulus. The US, UK, Japan and to a lesser extent, the Eurozone are all going to expand their fiscal spending, shifting away from austerity. In some cases, spending plans will boost the economy – like infrastructure spending in the US – which will also help to absorb some of the unemployment left over in the construction and energy sectors. In other cases, stimulus will be less effective, like tax cuts to high-income earners.

The third actor is monetary policy, whose powers are gradually fading. While central bankers have driven markets over the past eight years, the tide has turned now, as we have highlighted since the summer. For central banks the mantra is now less is more, for two reasons: they have realised that QE infinity is self-defeating in bank-centred financial systems like Europe and Japan, and they are coming under increasing pressure to normalise interest rates from savers, insurers and pension funds.

We know the cast. How will 2017: The Movie look like?

- The Leopard (1963) – the muddle-through scenario. The US is likely to benefit from infrastructure investment and an aligned government-congress. US growth rises to over 2.5%, pushing the Fed to hike up to three times and US Treasury yields up to 3%. The Euro depreciates vs the Dollar to parity, boosting German exports and Eurozone inflation up to 1.6-1.7%. Bunds widen more than Treasuries. Le Pen, Grillo and Geert Wilders come close to winning, but they lose. However, they influence mainstream policies, adding additional spending. The UK gets a staggered Brexit deal and Greece a small debt extension. Everything must change, so that everything stays the same.

- Reservoir Dogs (1992) – the worst case scenario. The Trump administration implements not only domestic spending, but also imposes heavy tariffs on Chinese imports and limits migration from Mexico. China retaliates with a sudden depreciation of the Yuan, which falls by over 10%, dragging down other EM currencies with it. This hurts EM sovereigns and corporates, which have heavily relied on hard-currency funding over the past years. Russia-backed Front National and Five Star Movement win elections in France and Italy, reviving Eurozone breakup fears. As a result, the Euro falls below parity with the Dollar, boosting inflation in Germany and putting even more pressure on the ECB to curb its stimulus. The UK is granted a relatively benign Brexit deal. There is lack of agreement on Greece between the IMF and Eurozone creditors. Russia continues to expand, projecting its power further across Eastern Europe. Turkey rejects its deal on migrants, adding to economic pressures in Southern Europe. The ending is not pretty: a less stable, de-globalised world with unsustainable populist policies in place. If you shoot this man, you die next.

- The Big Lebowski (1998) – the best case scenario. Mr Trump’s foreign policy implementation comes out to be a lot more balanced than his pre-electoral speeches. Germany wakes up to the threats Europe faces by re-engineering a Juncker plan that is credible and of appropriate size, rather than the current 0.1% of GDP spent. Italy reforms its electoral law, electing a stable government. Le Pen fails in France. The UK reverses course on Brexit, accepting associate membership and agreeing to pay for access to the single market. Greece gets a serious debt restructuring/extension equal to 10% of net present value. After thinking you’re entering a world of pain, there is a happy ending.

Our base case is a combination of the first two scenarios. However, in all three, bond investors are worse off. Rising populism, fiscal expansion and fading monetary policy stimulus mean higher interest rates and inflation and higher volatility. This calls for more defensive strategies, able to monetise gains from a difficult investment environment.

In Europe, we expect economic growth to remain resilient. However, the main risk will be political, as France, Italy, the Netherlands and Germany will face rising support for populist parties at elections. We believe the ECB has set the ground for further tapering next year, especially as higher oil prices push up inflation and a weaker euro boosts German exports. We remain short core rates, and expect further widening in French government spreads as the risk of a Le Pen victory rises ahead of April’s French Presidential elections.

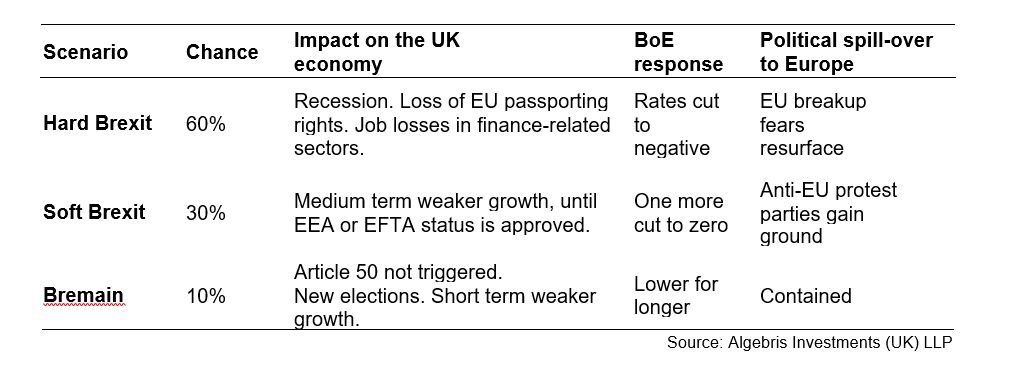

In the UK, we expect Brexit concerns to intensify again as the government triggers Article 50 in March and enters negotiations with the EU. Our base case is for a hard Brexit, with the UK losing EU single market access and passporting rights. This means structurally weaker Sterling, more import-led inflation and potentially deteriorating sovereign rating or a loss of reserve currency status. Gilts appear the most vulnerable to these risks.

We expect growth and inflation to accelerate in the US, supported by stronger stimulus under Trump’s administration. The Fed is on track to deliver at least two hikes in 2017, maintaining a dovish outlook. However, there is a risk of falling behind the curve against wage growth and political pressures for higher rates. This means Treasury yields have further room to widen, as inflation rises and markets adjust expectations.

Emerging Markets may be at the centre of a perfect storm next year. EM credits face a triple-threat. First, growth could decline on trade tariffs imposed by populist DM governments. Second, capital outflows could hurt EM assets on higher than expected Fed rates and a stronger Dollar. Third, hard-currency debt may come under pressure for issuers with local currency revenues. We remain cautious on EM economies that are exposed to three economic vulnerabilities: dependence to US exports, on hard commodities and on trade links with China.

Until 2016, investors bought equities for yield and bonds for capital gains. We continue to shy away from all ‘low-for-long’ trades and enter 2017 short on rates risk, long on inflation and financial equities and moderately positive on credit risk.

Our Views Across The World

Eurozone: Break-up Fears to Resurface

Next year, the fate of the Eurozone will depend on whether the balance of power shifts from Eurocentric towards Eurosceptic leaders. That is, while an isolated protest party’s victory would be insufficient to trigger Euro-break up fears, if two or more happen, then breakup risk could resurface. Absent that, we expect Eurozone growth to be 1.5% or higher.

Support for European protest parties will rise in 2017. We expect Euro-break up fears to resurface next year, as populist parties run in French, German and potentially Italian elections. In our view, the market is currently underpricing the chance of a Le Pen victory in France’s April Presidential elections. We expect Le Pen’s FN party to campaign on a Eurosceptic platform and to gain in polls leading up to the elections. Similarly, in potential Italian elections, Renzi’s PD party may lose seats to the protest party M5S, and in Germany’s October elections, support for far-right AfD party may rise.

The Eurozone economic recovery has so far remained resilient despite political uncertainty. With macro data pointing towards accelerating growth towards year end, consumers and businesses have been unfazed by rising political uncertainty. Spain was among Europe’s fastest growing major economy in 2016 despite the constant threat of re-elections, and Italy’s growth accelerated even as it became clear that the incumbent PM would lose the constitutional referendum.

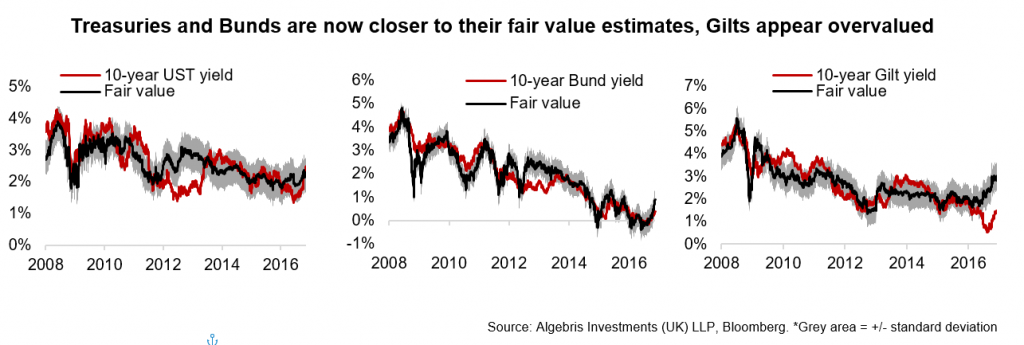

ECB President Draghi has set the stage for further tapering, next year. At the ECB’s December meeting, President Draghi’s speech was dovish, but his actions were clear: “risk of deflation has largely disappeared” and the case for expanding monetary easing is diminishing. In our view, Draghi’s decision to allow purchases below the deposit rate was merely to ensure smooth implementation of the existing QE programme. We think this decision overshadowed the hawkish QE-extension with a reduction in the monthly purchases and the increase in the 2017 inflation forecast, but we believe the ECB is biased towards doing less, not more. Therefore, we remain bearish core European rates, and think German 10y bund yields could rise another 20-30bp next year. We expect tactical steepening in sovereign yield curves, but remain bearish on German 5y which we think are now vulnerable to inflation acceleration, especially if OPEC production cuts are implemented and oil continues to rally.

The UK Will Neither Have Its cake, Nor Eat It

We expect Article 50 to be triggered next year, with a Hard Brexit as our base scenario. While the Supreme Court in January may rule in favour of a Parliamentary vote on Brexit, we expect MPs to vote in line with their constituents. We think the probability of a Hard Brexit has risen considerably, following PM May’s strong statements on immigration and withdrawing from the jurisdiction of the European Courts of Justice, at the Conservative party’s conference in October. While UK growth has remained resilient since the Brexit referendum, we think the economy is set for a stagflationary shock under a Hard Brexit. We estimate the direct economic cost of a hard Brexit at £140bn or around 7.5% of UK GDP, with the currency depreciating leading to higher inflation as the UK imports 46% of its energy and 50% of its food (The Silver Bullet | The High Price of a Hard Brexit).

Rising Inflation + Higher Deficits = Short Gilts. Under a Hard Brexit scenario, with higher inflation and slower growth, the most vulnerable asset is UK government bonds in our view. Despite inflation expectations rising above 3%, Gilt yields have remained anchored with 10y Gilts at below 1.5%. Gilts’ suppressed yields are on expectations of further BoE expansion which, in our view, the BoE can’t deliver. First, Gilts cannot be insulated from rising bond yields globally. Second, the BoE may temporarily look through above target inflation, but ultimately would need to act. Thirdl, the UK’s high pension deficit would be worsened by falling yields. Finally, Chancellor Hammond’s post-Brexit Autumn statement highlighted £59bn in additional borrowing over the next five years, implying further Gilt supply.

US: Make Inflation Great Again

Stronger fiscal stimulus should support growth and exacerbate inflationary pressure. The US economy expanded +3.2% QoQ annualised in Q3, suggesting the economic recovery remains well on track. Since the crisis, the US has been able to more quickly restructure its debt and re-start credit growth to support investment and consumption, thanks to deeper capital markets and more flexible bankruptcy laws.

This was despite a divided Congress under the Obama administration which made large fiscal stimulus difficult. With more forthcoming spending and tax cuts under Trump, growth is likely to accelerate, so is inflation. There has already been a pick-up in core inflation over the past months, helped by rising wage growth amid continued tightening in the labour markets. In addition, the gradual phase-in of minimum wage rises presents another tailwind.

The Fed is at risk of falling behind the curve. The Fed is likely to remain dovish on its policy rate outlook. In its September projections, the dot plots showed median forecasts of two 25bp hikes in 2017 and three each in 2018 and 2019, with the long run natural rate at 2.9%. This still indicates a much shallower hike path and lower terminal rate compared to previous cycles, while unemployment rate has already fallen to levels comparable to previous troughs. With stronger fiscal stimulus and oil prices turning into a tailwind, there is a higher risk of inflation overshooting the Fed’s target. In the worst case, the Fed could be forced to make snap upward adjustments to its policy forecasts.

Treasury yields have further room to widen as inflation rises and markets price in a faster Fed hike path. 10-year Treasury yield at around 2.5% is close to our fair value estimate now, but does not compensate for the risk of inflation overshooting. In addition, despite the Fed’s already shallow policy rate path projection, markets are pricing in even slower rate hikes. Hence we remain bearish on US rates.

Emerging Markets: at the Centre of a Perfect Storm

In 2017, emerging market credits will likely be at the centre of a perfect storm: a combination of fundamental growth deterioration triggered by potential tariffs and protectionist policies in developed markets, coupled with potential capital outflows as domestic bond markets become more attractive, and a stronger Dollar raising interest cost on hard-currency debt.

We are cautious in particular on countries which:

- Have high export exposure to the US and trade with the US under collective, rather than bilateral, agreements

- Export predominantly in hard commodities

- Would need to competitively devalue vs CNH, as the country either exports to China or competes with China on trade

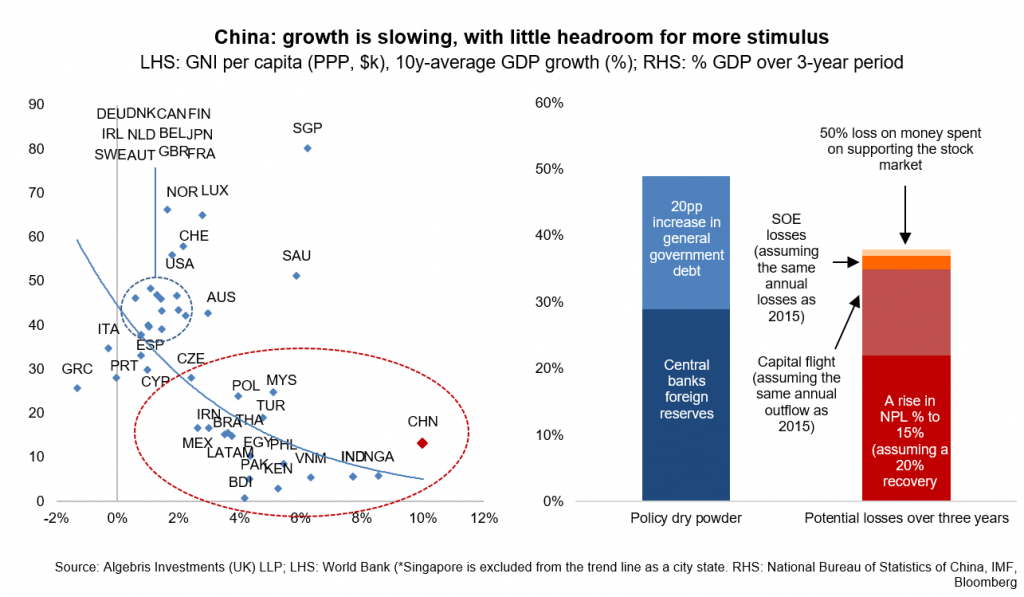

China is walking a tightrope between deflating its credit bubbles and maintaining growth. This paradox has led to political discord between its top leaders and policy inconsistencies in 2016. At the start of the year, a series of mini-fiscal stimulus and relaxations of credit standards had contributed to a housing market boom and boosted growth. These coupled with a stabilisation in capital outflows and the exchange rate reduced markets’ concerns about China risks, even though the country’s credit bubbles had just grown bigger during the period – we estimate total public and private debt at around 300% GDP now. However, both fiscal and monetary policies have taken a sharp turn in H2, with measures to curb house price growth introduced since October and the PBoC tightening liquidity supply to control leverage. In our view, while China has taken a right step to delever the economy, the risk is that short-term growth will fall and slowdown fears will kick in again as stimulus effects fade. This means more Yuan depreciation, which has already been happening in H1 and worsened since Trump’s election victory. So far there has not been much contagion to other EMs, which could start to happen if China’s slowdown or Yuan’s depreciation accelerates.

Mexico: a resilient 2016, yet external fears today may turn into domestic economic pain in 2017. Mexico’s economy is likely to weaken next year as the MXN devaluation will be insufficient to offset potential shocks to US-Mexico trade (the US consumed 73% of Mexican exports, in 2014). Even before Trump’s policies have been formulated, confidence in Mexico’s economy has declined: consumer and business confidence have fallen 9% and 6% in 2016, according to the INEGI. Additionally, while the oil rally will benefit Mexican government finances given Mexico is a net exporter of oil, higher oil prices combined with the weaker MXN will likely lead to higher inflation. Mexico’s economy is now forecasted to grow 1.8% next year (Bloomberg consensus) vs a 2.2% growth forecast by the IMF before US elections.

Brazil is on its way to recovery, but the Caipirinha Crisis could return with a China-lead BRL devaluation and political infighting. We think growth in Brazil is set to benefit next year from positive domestic conditions: interest rates are falling as inflation abates and the currency strengthens; consumer confidence is returning as unemployment plateaus; and government finances – though still abysmal – will likely improve as the lower house passed new fiscal consolidation rules in November. However, Brazil remains vulnerable to lower commodity prices resulting from a China slowdown, and higher inflation if a China devaluation forces Banco Central do Brasil (BdB) to devalue as well. Additionally, political infighting could rise early next year if Temer vetoes a controversial bill which would allow judges to be tried for ‘abuse of authority’, which in effect has been tabled by legislators to curtail the power of the Operação Lava Jato investigations.

Argentina’s external shocks and financing needs may weigh on investors’ minds, as domestic headwinds materialise in 2017. Argentina’s return to the markets in 2016 unleashed a flood of debt with the country issuing around $22bn in international debt (4% of forecasted 2016 GDP). Despite investors’ exuberance, an economic recovery has yet to materialise. Recent data showed that recession is biting deep into the country’s industrial base – industrial production and construction were down 7% and 13% YoY respectively in September 2016. Yet 2017 also bears new risks for the country, in the form of growing consolidation within the opposition/Peronists, which could lead to lower investor confidence in Macri’s ability to implement market friendly policies.

Venezuela continues to live on borrowed time. In our view, PDVSA’s October debt exchange and OPEC’s deal may provide Venezuela with enough breathing room to meet its outstanding 2017 maturities. Information on Venezuela’s liquidity, however, is opaque outside of its reported foreign exchange reserves ($10.9bn in October). Compared to other LATAM EMs, Venezuela is relatively insulated from potential shifts in US trade policy: Venezuela lacks an export-base outside of oil, which makes it a less attractive target for Trump’s anti-trade zealotry. Also, President elect Trump’s aversion to multi country treatises (i.e. NAFTA, TIIP) should not directly affect Venezuela’s bilateral trade relationship with the US.

Russia should benefit from higher oil prices and more favourable diplomatic relations with the US, though sanctions are unlikely to be completely lifted. With the Ruble strengthening in line with oil prices, inflation has declined and capital flows have improved. Russia looks set to exit its almost two-year recession, with GDP contracting only -0.4% YoY in Q3 2016. We think this positive trend is likely to continue in 2017, with additional growth tailwinds coming from improving relations with the US under a Trump administration and potentially a partial easing of sanctions. A complete lift in sanctions looks unlikely for now given that it also depends on the EU’s stance, but the political environment may become more favourable for Russia if France’s FN and Italy’s M5S strengthen their political influences and Euro break-up fears resurface.

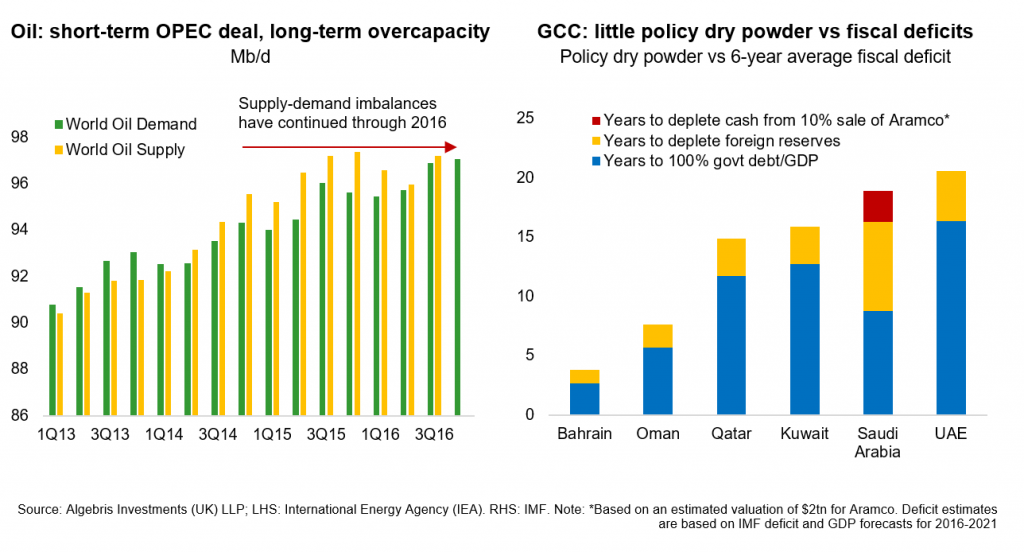

Gulf Cooperation Council (GCC) economies continue to look vulnerable to us, especially in an environment where oil price vulnerabilities persist, US-Middle East relations worsen under Trump, and discontent grows amongst locals on planned austerity programmes. Since the oil price decline began over two years ago, GCC economies have done little to reduce their dependence on oil, aside from Saudi Arabia spending nearly $1.2bn in consulting fees in FY2015. Saudi’s ‘Vision 2030’ plan to shift its economy away from the oil sector looks ambitious, and we continue to expect more blockbuster debt issuance from the Kingdom in order to fund its fiscal deficit. Amongst GCC countries, we see Oman and Bahrain as being the most vulnerable if oil prices fall again: these countries have the lowest firepower (low foreign reserves, and ability to raise debt) to fund their fiscal deficits, which are projected by the IMF to be the highest amongst GCC countries.

India: “Very Good, Very Bad”. India’s “positive-EM” story, which has persisted since PM Modi’s was elected in 2014, is now at an inflection point, in our view. On the one hand, the Indian economy is more resilient to external-shocks today than it was 4 years ago, during the first taper tantrum: India’s current account deficit has declined to almost flat, inflation is low at around 3.5% and rates have been cut by over 150bps. However, on the other hand, Modi’s ‘de-monetisation’ decision will likely slow the economy in the near term, while the benefits in the long run are unclear and may ultimately cost him the next election.

Escaping QE Infinity: Our Views Across Asset Classes

Rates: We think rates could go wider on higher inflation and a normalisation in term premia. We expect curves to steepen, as central banks shift from QE Infinity to polices that implicitly target yield curve slopes so as to restore bank profitability and improve monetary transmission. US Treasuries and are now within one standard deviation from our fair value estimates, but there is room for further yield widening in Bunds and Gilts. Gilts in particular look vulnerable vs additional fiscal spending and rising inflation. The post-Brexit Autumn Statement highlighted £59bn of additional borrowing required over the next five years, which means more debt issuance. Gilt yields, at 2pp below 10-year inflation expectations, do not fully compensate bondholders, also given additional risks from a deteriorating sovereign rating and potential loss of reserve currency status for Sterling. The other rates market that appears vulnerable is France, where political risk is rising as we get closer to the French Presidential elections (the first round is due on 23 April and run-off is on 7 May 2017). Front National’s (FN) Le Pen has been gaining consensus and is the runner-up in recent polls. As Brexit, the US elections and the Italian referendum results have shown, polls have a tendency to underestimate the risk of protest votes.

Inflation: After years of deflation fears, we think the risk for inflation has finally turned to the upside. In the US, stronger fiscal stimulus and likely accommodative monetary policy should push up prices, especially as labour markets tighten. With uncertainty over Brexit negotiations, the Pound will likely continue to face selling pressure, resulting in import-led inflation. The recent strong surprises in Chinese PPI could also mean China shifts from exporting deflation to exporting inflation. The Eurozone will not be isolated from this global reflationary backdrop: as other central banks tighten policy and the Euro depreciates, this will boost exports and prices. In addition, the OPEC agreement on production cuts, albeit small, should provide near-term support to oil prices and headline inflation. Lastly, additional inflationary pressure could come from populist policies like higher minimum wages, trade tariffs and immigration controls.

Credit: Spreads in developed markets should remain broadly stable, underpinned by a low default rate environment and ECB/BoE purchases of corporate bonds. In particular, bank and insurance credits should perform better on higher rates and steeper yield curves. EM debt will be vulnerable to weaker local currencies and higher DM rates, despite some short-term support to oil names from the OPEC deal. That said, EM fundamentals and growth remain broadly positive. Cash bonds appear more attractive than credit default swaps, which have been squeezed to record tight levels into year-end after consensus fears around Italy’s referendum turned out to be overblown.

FX: We think the Dollar will continue to strengthen against other developed market currencies as the market prices in a rate hike path faster than the current dot plots suggest. In addition, we expect more Yuan depreciation, as China slowdown fears come back and capital outflows accelerate. These two forces will weigh on EM currencies, especially as they remain vulnerable to potential protectionist measures in developed countries.

Equities: The end of QE Infinity, stronger fiscal stimulus and a normalisation in yields should benefit banks, insurers and cyclical sectors while hurting utility and staple stocks, which had been heavily bought as bond proxies when yields were low.

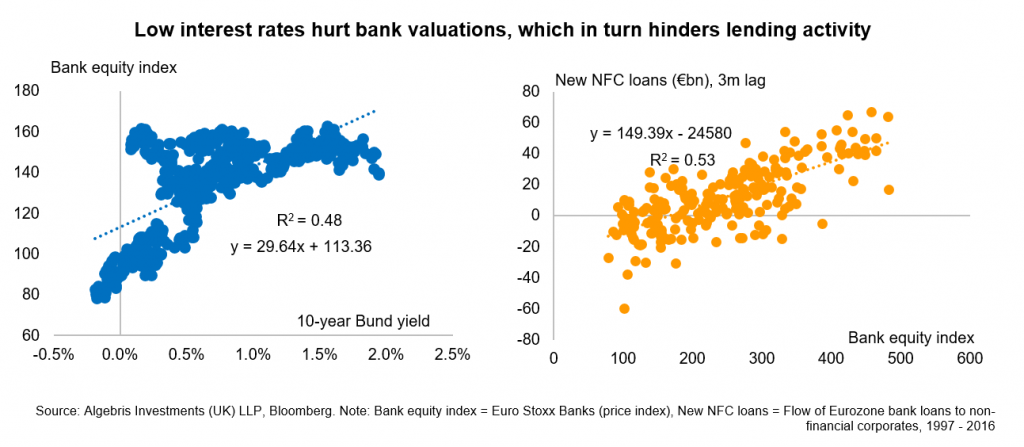

Banks have been the biggest victims of QE and negative interest rates. As the BIS and we have argued before, low interest rates provide banks with a one-off gain on their government bond holdings, but erode profitability and equity valuations. This in turn means higher cost of capital and lower ability to lend, creating a vicious cycle and the need for more easing.

The shift in central bankers’ focus from unlimited easing to improving the credit transmission of stimulus is creating an inflection point for banks. Central banks know that both bank revenues as well as valuations increase with positive long-end interest rates – and that higher valuations are linked to stronger lending flows. While QE infinity was becoming self defeating for banks, the new monetary policy regime means less is more. In addition to this, banks are now structurally stronger than before the crisis, with more capital and smaller balance sheets. In Europe, bank CET1 ratios have more than doubled since 2009, to 12.6% in 2015, and non-performing loans have steadily declined since mid 2013. Total bank assets for Eurozone banks have also shrank from over 350% GDP at the peak in 2012 to just below 300% now. Secondly, banks should also benefit from the tailwind of a pause in regulatory tightening, as the Maximum Distributable Amount (MDA) of profits has been redefined and softened, and Basel 4 has been recalibrated lower. Finally, European bank valuations remain near all-time lows (price-to-book ratios of around 0.4x).

Commodities: For hard commodities, we continue to remain bearish not only because supply overhangs persist, but also as demand may ease next year from the world’s largest metal consumer – China, with the country likely to curtail fiscal stimulus next year. Similarly, while we remain tactically bullish on oil as firmer global growth and greater fiscal stimulus boost demand, we expect supply side pressures to return in 2017. Firstly, OPEC production targets historically have not been adhered to. Saudi remains incentivised to boost output as it has become evident this year that the Kingdom’s targets to reduce oil dependency by 2020 were overly optimistic. Secondly, while sanction restrictions on Russia may potentially ease under changing US/European administrations, Russia continues to require higher oil output to help the country exit its almost two-year recession. Finally, oil prices are reaching levels which have traditionally been the break-even levels for US shale producers, increasing the risk of higher shale supply next year.

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.