Since this summer, we have warned investors of a turning tide in global bond markets, due to less dovish monetary policy, upcoming fiscal stimulus and a shift towards populism and protectionism.

First, central bankers have moved from QE infinity and negative interest rate policy (NIRP) to QE with limits, which is less beneficial to financial markets but more sustainable and better for credit transmission to the real economy (The Silver Bullet | Central bankers: the tide is turning, 7 September 2016). Second, a shift to fiscal stimulus and higher wages has rebalanced the policy mix and reduced deflation fears. Third, rising populist and protectionist pressures will boost inflation further: imposing tariffs on foreign goods, limits on migration, or exiting the EU altogether, mean higher import prices and higher labour costs (The Silver Bullet | Trick or Tantrum?, 31 October 2016).

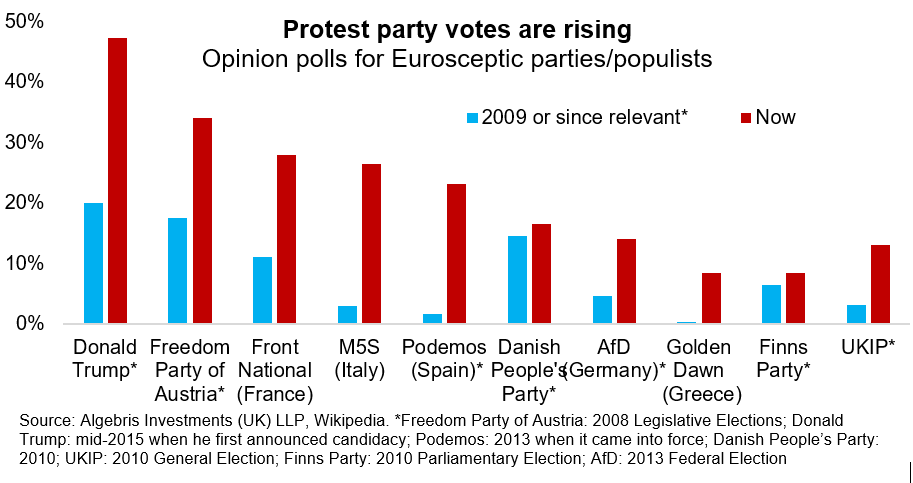

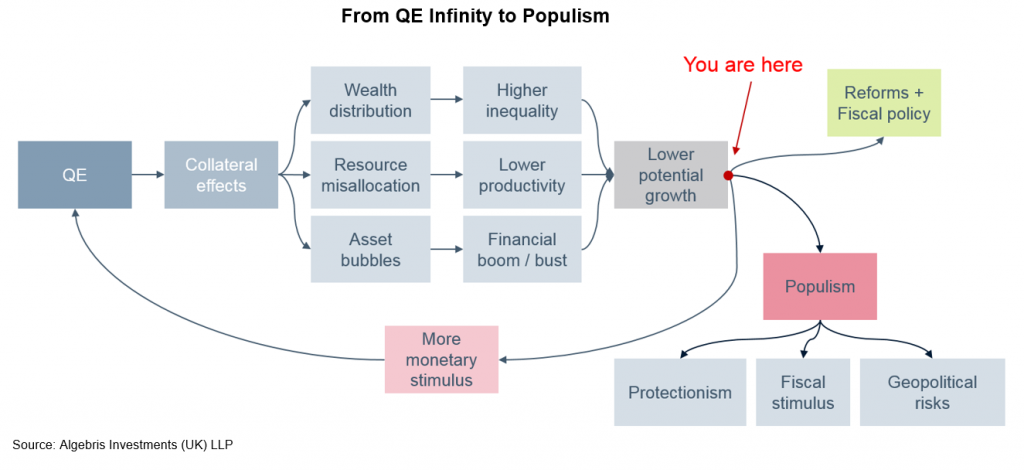

Ultimately, the straw that broke the bond markets’ back wasn’t reluctant central bankers or fiscal stimulus, but populism. The protest vote is still alive and spreading, potentially to France and Italy. Inequality and lack of social mobility provide the economic conditions for populism to spread further, as research analysing elections over the past 144 years has shown (Funke, M., Schularick, M., Trebesch, C., 2015).

We believe we are at a tipping point in markets, policy and geopolitics. Here is how we are positioned:

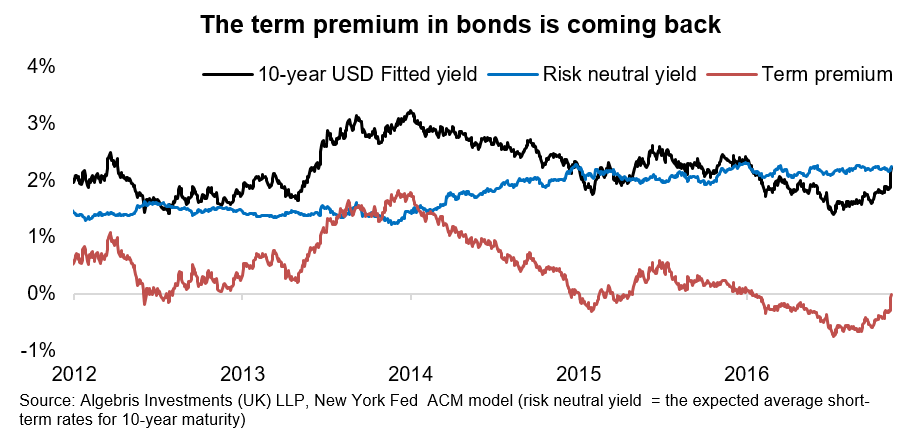

Overall: We believe long-end interest rates have more room to widen into year-end, both on higher inflation as well as on normalisation in term premia, which have just turned positive. The moves in rates markets will also impact credit, equities and currencies. In equities, we continue to see banks and insurers outperforming utilities, telecoms and staples, with banks benefiting from the additional tailwind of a pause in regulation tightening. Credit spreads remain anchored by a low default rate environment and ECB/BoE purchases of corporate debt. However, EM debt has widened in tandem with weakening EM currencies. This pressure is likely to continue in the near term, but it is also starting to unveil potential opportunities. Finally, rising US wage inflation should support Fed policy tightening and a stronger Dollar.

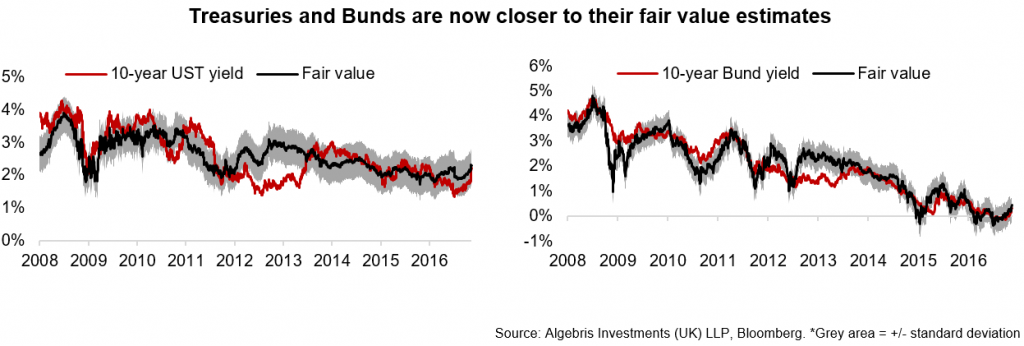

Rates: US Treasuries and Bunds are now one standard deviation away from our fair value targets. We believe rates can still go wider on a normalisation in the term premium. Gilts, in particular, look very vulnerable vs additional fiscal spending and rising inflation. Chancellor Hammond will announce the UK budget on November 24. He is likely to take a conservative approach. However, rising inflation and the cost of Brexit mean the government will have to delay their plan towards a balanced budget over the coming years, and issue more debt. Gilt yields, at over 2% below 10-year inflation expectations, do not compensate bondholders – with additional risks coming from a deteriorating sovereign rating and potential loss of reserve currency status for Sterling. The other two rates markets which appear vulnerable are France and Italy. France will see rising political risk, with Le Pen gaining consensus: elections are in May 2017 with primaries on November 20. While it is too early to estimate a probability of a Le Pen victory, we remain cognizant of the risk of protest votes, as we did when anticipating the high probability of a Trump victory (The Silver Bullet | Trumponomics, 1 June 2016). Likewise, a No vote is currently leading polls in Italy, for the constitutional referendum to be held on December 4.

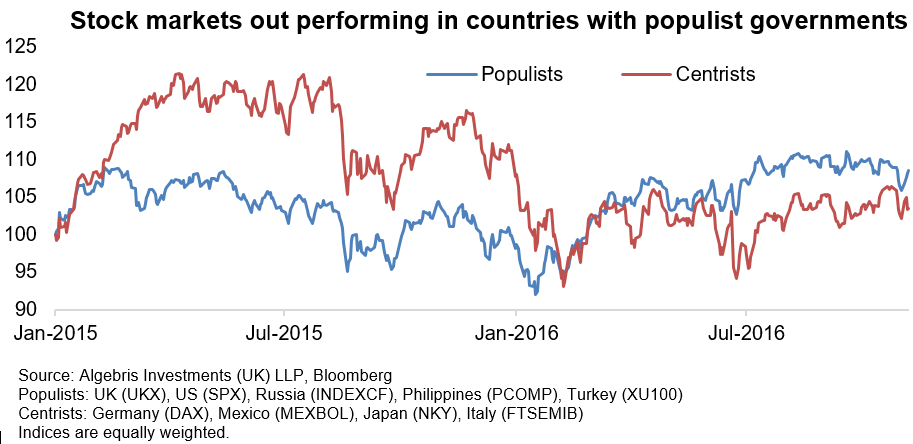

Credit: credit spreads remain broadly stable in developed markets, underpinned by central bank buying and a low default rate environment. We are cautious in the UK around the consumer and real estate sectors, and generally prefer banks and insurers, which are poised to perform better on steeper yield curves. Emerging market credit has underperformed substantially on Trump’s win. There is plenty of room for concern, particularly around Trump’s proposal for tariffs on China. The worst case scenario is a trade war, which would imply an accelerating depreciation in the Yuan, with other EM currencies to follow. EM corporates hold a large proportion of their debt in dollars, which makes many of them vulnerable to such a currency repricing. That said, we think valuations have overshot vs fundamentals, which remain broadly positive: in other words, the selloff is disorderly and has created opportunities.

Equities: For financial stocks, and especially banks, we have seen a number of inflection points during the year but in Q3 they became all the more powerful by combining together. First, there has been a shift in rates outlook, as central bankers move away from QE infinity and NIRP. Second, for the first time in years, we have seen significant positive changes in the earnings outlook where Q3 numbers were strong and did not lead to downgrades. Third, there are changes in capital and dividends, where >90% of large European banks are properly capitalised and there is a plan for the rest (MPS, UCG and DBK). Last but not least, we are seeing a turning point in the regulatory outlook, where the Maximum Distributable Amount (MDA) of profits has been redefined and softened and Basel 4 has been recalibrated lower. This should lead to reduced volatility in financial share prices as well as a slow unwind, over multiple years, of the large underweight that many investors have, especially in bank equities.

Conclusions: The current shifts in monetary policy, fiscal stimulus and the rise of protest politics are breaking the bull market in bonds. Investors in passive duration strategies face a multitude of risks similar to the experience of postwar financial repression: higher deficits, lower credit quality and inflation. Like never before, we tread carefully. Our strategies have been negative long-end duration, long volatility and long financials, benefiting from the repricing in markets.

But the potential implications of a Trump victory extend well beyond financial markets. Research over the past 144 years shows that far-left and far-right governments emerged after financial crises (Funke, M., Schularick, M., Trebesch, C., 2015). In the case of the US, a hard-nosed approach to trading relations could accelerate currency depreciation in China. Trump’s stronger relations with Russia could allow Putin’s government to extend its power projection into Eastern Europe, as it has already done in the Ukraine and in Moldova and Bulgaria, which elected pro-Russia candidates this weekend.

Ultimately, Europe’s fate will hang again in the balance. Inequality is fertile ground for populism and centrifugal forces rising in the UK, France, Italy and Germany. Against these forces, European policymakers have one last chance to implement pro-growth policies and structural reforms. The path is clear: debt restructuring for Greece, a real plan to foster future growth, and more integration in economic and defence policy. With Putin knocking at its door, Europe must hang together, or will hang separately.

Per ulteriori informazioni su Algebris e i suoi prodotti o per farsi inserire nella lista di distribuzuione, si prega di contattare il dipartimento Investor Relations all’indirizzo algebrisIR@algebris.com. Gli articoli passati sono disponibilii sul sito Algebris Insights

Questo documento è emesso da Algebris (UK) Limited. Le informazioni contenute nel presente documento non possono essere riprodotte, distribuite o pubblicate da alcun destinatario per qualsiasi scopo senza il preventivo consenso scritto di Algebris (UK) Limited.

Algebris (UK) Limited è autorizzata e regolamentata nel Regno Unito dalla Financial Conduct Authority. Le informazioni e le opinioni contenute nel presente documento hanno solo scopo informativo, non hanno la pretesa di essere complete o complete e non costituiscono una consulenza in materia di investimenti. In nessun caso qualsiasi parte del presente documento deve essere interpretata come un’offerta o una sollecitazione di qualsiasi offerta di qualsiasi fondo gestito da Algebris (UK) Limited. Qualsiasi investimento nei prodotti cui si fa riferimento nel presente documento deve essere effettuato esclusivamente sulla base del relativo Prospetto informativo. Queste informazioni non costituiscono una Ricerca di Investimento, né una Raccomandazione di Ricerca. Con il presente documento Algebris (UK) Limited non organizza o accetta di organizzare alcuna transazione in qualsiasi tipo di investimento, né intraprende alcuna attività che richieda l’autorizzazione ai sensi del Financial Services and Markets Act 2000.

Non si può fare affidamento, per nessun motivo, sulle informazioni e sulle opinioni contenute nel presente documento, né sulla loro accuratezza o completezza. Nessuna dichiarazione, garanzia o impegno, esplicito o implicito, viene data in merito all’accuratezza o alla completezza delle informazioni o delle opinioni contenute in questo documento da parte di Algebris (UK) Limited , dei suoi direttori, dipendenti o affiliati e nessuna responsabilità viene accettata da tali persone per l’accuratezza o la completezza di tali informazioni o opinioni.

La distribuzione di questo documento può essere limitata in alcune giurisdizioni. Le informazioni di cui sopra sono solo a titolo di guida generale ed è responsabilità di ogni persona o persone in possesso di questo documento informarsi e osservare tutte le leggi e i regolamenti applicabili di qualsiasi giurisdizione pertinente. Il presente documento è destinato esclusivamente alla circolazione privata per gli investitori professionali.

© Algebris (UK) Limited. Tutti i diritti riservati. 4° Piano, 1 St James’s Market, SW1Y 4AH.