Inflation’s higher than your bond rates

That’s what I was fearing

So your savings account

Is slowly disappearingDogecoin Rap, Remy, 2021

One year ago, markets were in panic. Bonds from large government-backed corporations offered record returns to investors willing to bet on their survival. Today, we are in a state of euphoria. Not only have markets priced in a much lower likelihood of such end-of-the-world scenarios – they have moved to reflect a goldilocks environment, a combination of strong growth and subdued inflation.

The underlying consensus assumption – reiterated from the Fed Chair down to most sell-side economists – is that inflation pressures will be temporary and that central banks will be able to keep policy loose, leaving the punch bowl out and the party going.

What if they are wrong?

After two decades of QE infinity asset-based monetary stimulus, which together with corporate tax cuts, had little effect on inflation – economic policy has finally turned the corner.

Financial markets are no longer the only priority: the real economy is. President Biden’s Congress speech from last week highlighted key measures to rebalance society: more spending for families and higher taxes on top percentiles of wealth. This is a drastic change from QE infinity, which as we have been arguing since 2015, increased wealth inequality and was in some cases deflationary. Europe too is accelerating its distribution of anti-Covid vaccines and boosting spending through its Next Generation EU Recovery plan.

Milton Friedman once said that nothing is more permanent than a temporary government programme. Before being a monetary phenomenon, inflation is a political one. We believe governments will not easily be able to quit from spending and high deficits. Today’s spending programmes will likely result in higher structural demand for commodities as well as services, while increased geopolitical tensions are likely to bring production of strategic goods back on shore, reversing. The result is likely to be continued depreciation of fiat currencies against real assets.

Coming from a multi-decade bull market in bonds, it is easy for investors to stay in the lull of their allocations. However, about 60% of global bonds now yield less than one percent. Most bond portfolios, balanced portfolios and fixed income funds are positioned the wrong way. All contain bonds which yield less than inflation and no longer provide much protection in market sell-offs, as we have seen over the past quarters. Investors can either lose money slowly against inflation, or quickly, in a re-pricing.

Valuations are too high and volatility too low. We believe demand will bounce back quicker than expected. This, coupled with supply bottlenecks, will likely bring volatility back across inflation, yields and risk assets. But temporary volatility is only the beginning of the story. More government spending is ahead of us, and central banks are ready to support it with even looser policy over the coming years, including yield curve control and central bank digital currencies.

From Panic to Euphoria

Reopening: A story of divergence

Global economies are re-opening, but a full re-opening will likely take until 2022. At the start of the year, we expected a near-normal 2021 summer across developed economies. High vaccine efficacy rates and large national contracts initially aimed to bring near-full immunity by the summer across developed economies. However, with operational challenges and some skepticism around side-effects, the vaccine roll out has turned out to be slower than anticipated. With the exception of the UK, the US and Israel, almost no developed country today is set to have 60% of its population vaccinated with at least one dose by June, we estimate. In Europe, by our estimates, it is likely that 60-70% vaccine rates will only be reached in August. Vaccination rates will likely be slower in other developed economies like Australia, New Zealand, Korea and Japan.

COVID has amplified divergences across countries, with the US outperforming the rest of the world, especially emerging markets – with the exception of China. Over the past fortnight, around 30% of total new COVID cases came from India alone. Despite only 8% of the population being vaccinated, the Indian government had decided that the economy could no longer suffer the burden of a lock down. This premature reopening led to a resurgence in cases, and has now caused a second lock down. The EIU estimates that only 60% of the Indian population will be vaccinated by mid-2022, thereby limiting India’s ability to meaningfully reopen the economy until then. In contrast, in the US nearly 70% of the population has had at least one dose and the country is set to have a near-normal summer. This contrast between India and the US is an example, but is illustrative of the divergence between EMs and DMs in terms of their vaccination roll out rates and, therefore, paths to economic recovery. This divergence was illustrated in the IMF’s latest growth forecasts of April 2021: while developed markets’ growth was revised higher by 0.8pp and 0.5pp in 2021 and 2022, emerging markets’ growth was revised higher by only 0.4pp in 2021 and was unchanged for 2022.

Annual vaccination requirements and COVID variants increase the risk that this divergence persists. While eventually both emerging and developed economies will have an equal vaccination rate, the time period to achieve this is further stretched by the need for repeat doses. Also, as seen with the variants in South Africa and Brazil, the efficacy of the vaccine could be impaired. This would lead to new product cycle timelines and potentially further delivery time differences amongst nations.

Inflation: Some central banks are cautiously tapping on the brakes

“We find ourselves in a situation here where we’re on the roof, and there is no risk-free path. We’ve got to jump.”

− Jerome Powell, 2013, Fed minutes on tapering discussions.

Higher or higher-for-longer inflation is the key risk against current market valuations. “It may be that interest rates will have to rise a little bit to make sure our economy doesn’t overheat” – US Treasury Secretary Yellen said earlier this week – yet, markets could not take it, and Secretary Yellen had to quickly backtrack on her statements. Today’s belief in lower-for-longer interest rates, contained inflation pressures and a loose central bank reaction function underpins record-high valuations in equity markets, and record-tight risk premia across long term government debt and credit.

The consensus expectation amongst central bank economists and investors is that while inflation may be higher, it will be transitory. Neither investors nor central bankers are prepared for a permanent or extended regime shift towards higher inflation. Some central banks’ projections however, are already proving to be too optimistic. The Fed and Bank of Canada are projecting inflation to remain around 2% until 2023 and the ECB project it to remain below 2% until 2023. However, in recent weeks, PPI (the price levels received by domestic producers for their production) in China, the US and Europe has reached around 4% YoY. In part, this rise is due to a large YoY change in commodity prices – both in hard and soft commodities, partially due to supply disruptions caused by COVID. But even excluding commodity price base-effects, there has been a positive trend in PPI. As seen in German PPI excluding energy, prices are rising by over 2% YoY and, breaking multi-year highs. In April’s US ISM survey, eight out of ten respondents reported paying higher prices for materials, up from just 6 out of 10 respondents in January. While historically the passthrough from PPI to CPI has been mild, it could be stronger this time. One catalyst for this stronger pass through could come as the economy reopens and unemployment falls: higher goods-inflation could start to pressure an increase in wages which would further increase CPI. In the US, higher consumer prices could be around the corner: on recent earnings calls, US company executives have warned of price increases to come. For example, P&G said prices on certain products would be increased by mid-to-high single digits from September and that they would review other products shortly. Likewise, Whirlpool said it was planning price increases of between 5-12%.

There are also early indications of new inflation catalysts. On the one hand, some of these drivers are temporary but could last until year end: for instance, the global chip shortage was initially expected by investors to last only a few weeks, but could now last for most of 2021 – or past 2022, according to some more bearish expectations. For now, this chip shortage has resulted in reduced production / inventory rather than increased prices, but as the shortage extends and inventories continue to fall, it is likely prices will begin to rise. For instance, Goldman Sachs estimates that the shortage is likely to increase 2021 US CPI by between 0.1% to 0.4%. On the other hand, there are also new inflation drivers which are more structural: like onshoring supply chains and production, despite higher costs, both as a lesson-learned from COVID, as well as a way to protect intellectual property in an environment of rising geopolitical risk. This de-globalisation trend will likely increase production costs.

Which central banks are likely to pull the punch bowl first? Some policymakers have already started to gently tap on the brakes.

The Bank of Canada became the first G10 central bank to start tapering its pandemic asset purchases. Last week, the BoC announced its asset purchase tapering as it forecasted stronger Canadian growth, and for inflation to remain persistently above or near 2% until 2023. The BoC’s hawkish stance may be unique in the global context: despite resurgent virus cases, the commodity-linked economy has been boosted by higher commodity prices. In addition, the BoC has a singular mandate to control inflation, as opposed to the Fed’s dual mandate which also focuses on achieving full employment. As a result, and unlike the BoC, other central banks have chosen to wait, rather than tapping the breaks. But this might mean that they will have to hit the brakes harder later on, if inflation overshoots become more persistent.

The Fed is likely to begin discussions around exiting its pandemic asset purchase program in H2. As Fed chair Powell said at the last meeting, tapering will depend on the US showing substantial progress towards achieving maximum employment. This is likely to come by year-end, as employment picks up in reopening-linked sectors like travel and hospitality.

The Bank of England may be the next candidate to consider a hawkish shift. An announcement of a gradual tapering from 4Q21 may come as early as August. This could be triggered by an upward revision in the growth and inflation forecasts. The BoE’s current economic assumptions were made prior to the fast roll-out of vaccinations in Q1. That said, the BoE’s board remains largely dovish, and might bark more than bite.

Other G-10 central banks may be slower to introduce tapering discussions. In Europe, the ECB recently dismissed tapering discussions as “simply premature”. The ECB is likely to also be under less pressure than the Fed to taper given Europe’s slower vaccination roll out and fiscal spending. However, some of the ECB’s hawks have already broken ranks, and consensus on keeping the PEPP going might start fading after the June meeting.

The RBA and RBNZ are unlikely to discuss tapering until 2022 given slow vaccine roll out, fraying relations with key trading partner China and systemic risks from high house prices. Likewise, in Japan, there is almost no pressure to discuss tapering as inflation remains low, despite the base effects from last year.

Geopolitics: China and Russia test the Biden administration

A key risk for the reminder of the year is the potential re-inflammation of geopolitical tensions. In fact, the new US administration is proving more hawkish than broadly expected. Ahead of elections, Biden was broadly seen as a dove in international policy based simply on the contrast with Trump’s unpredictable approach. The first few months of 2021 make clear this common wisdom was wrong: Russia received long-awaited sanctions in the first three months of Biden term, and the stance on China is not softening much outside trade. Turkey may be next in line. As a new global leader is now at the White House, other global powers are likely to continue testing boundaries. As a result, we may be set up for a few noisy months. Geopolitics can cause clusters of volatility, as markets try to second-guess the next area of tension once one is exhausted.

Russia has been playing war games, and for US-Russia relations, this has been a rocky start. Navalny’s poisoning triggered a round of personal sanctions, and election interference finally pushed an extension of sanctions towards sovereign debt. While the latter restrictions came in a milder-than-feared form, it launches a powerful message. The US is monitoring Russia’s bravery in global affairs, and is ready to touch painful areas. On its part, Russia is keen to challenge the new US leadership. Putin’s comments on Biden have been provocative and troops amassed at the Ukraine border made it clear Russia still wants to be seen as the regional leader in Eastern Europe. In the next few weeks, a relaxation is likely as sanctions have been announced and Russia is already retiring troops. Still, the rough start is a clear sign of more confrontation going forward, meaning more tit-for-tat and potential market pain.

China turns out to be another open front as tensions at the border with Taiwan rise and technological competition with the US intensifies. Semiconductor shortages exacerbate the long-standing issue of technological competition with the US, while tensions with Taiwan have the potential to require a clearer US stance towards the region. Also, signs of China-Russia cooperation are increasing, adding to Washington headaches. Overall, tensions between the US and China are less likely to have an immediate market impact: there is no open confrontation as there is with Russia, and after Trump the US has moved past trade wars. Still, a gradual deterioration will make occasional tensions more likely and will increase polarization in terms of global bilateral relations.

Geopolitical tensions are also likely to increase further in Turkey. Beyond domestic volatility, Ankara’s relations with the EU keeps nosediving, and the first Biden comments have not been positive. With the US, Turkey holds quite a long “open bill”: both retaliation for S-400 purchases and the Halkbank fine are yet to be seen, and Erdogan’s comments on the US continue to be hawkish. While the former US administration never stepped-up economic warfare with Turkey, a parallel with Russia suggests we should be more wary under Biden. Financial/economic measures against Turkey are likely to have a much stronger market impact than in Russia, given the strong reliance of the country on foreign capital.

Geopolitics and markets – when it rains, it pours.

Geopolitics and markets: Growing underlying risks

Over the past decades, macro tailwinds from monetary and fiscal policy have usually overshadowed geopolitical shocks. However, persistent tensions between China, Russia and the US could go beyond news headlines.

The first knee-jerk reaction from geopolitical tensions is of course market risk-off. Today, valuations discount a very calm environment, with valuations from EM credit spreads to equity volatility at record lows. But beyond that, evidence from the IIF, on the left, shows that only companies in the US, China and Taiwan are able to pass higher input prices, on average. A combination of longer supply chain times and onshoring of production at higher costs might end up squeezing corporate profits too.

Is there nothing left to buy?

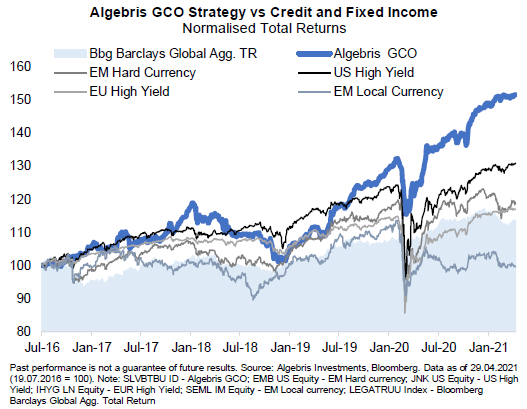

Tight spreads, rising rates and a flurry of summer risks are a tricky combination for fixed income investors. High yield and emerging markets now yield less than 5% in USD terms, and index duration is at the highs post the 2020 boom in issuance. As a result, even small moves in rates have the potential to turn into negative returns. In February 2020, before the Covid crisis, we warned investors that there was nothing left to buy in the market. Today, the upside-downside for bonds is definitely skewed against bondholders – only a few areas of value remain.

Based on our decomposition of credit returns by risk factors (see Appendix I), a significant portion of returns for IG and HY indices since last year were attributable to better liquidity, which could start to reverse soon with central banks changing tone. Today the risk premium from liquidity is gone, and credit presents a very asymmetric risk-reward profile. In a good scenario, investors can make carry and enjoy limited spread tightening, while in a bad scenario drawdowns in high-risk bonds have historically been close to 10-15%. From an asset class perspective, credit is a bad deal.

We see opportunities in selected cyclical single-B rated credits in developed markets. Airlines, cruises and some carmakers are still discounting skepticism on economic re-opening, even in cases where government support is strong or liquidity abundant. The risk premium is higher in Europe – while most of US re-opening sectors have now priced a recovery.

In emerging markets, we remain broadly cautious, but we find value selectively in situations with strong external support despite high yields, like Pemex, Naftogaz and Air Baltic. Another area of value is property developers in China: the sector offers yields uniformly in the 7-10% range despite very big differences in fundamentals. Relatively high quality developers can offer 6-7% yields despite low gearing and sometimes systemic dimensions.

Finally, we remain positive on convertible debt, especially in energy / re-opening sectors. High grade issuers in high beta sectors continue to offer a positive convex upside-downside profile to investors. Issuers with healthy balance sheets in hospitality, energy, or travel sectors can see a strong equity re-pricing in a positive scenario, but have little credit risk in a negative one. As such, the presence of convertibles in a bond portfolio can make up for the negative asymmetry offered by credit markets. Examples including Dufry, FNAC, Accor, TUI and Campari. Convertible debt is currently our top asset class, with around a 20% allocation.

Conclusions: Rethinking Bond Investing

Rockets, moon shots,

Spend it on the have nots

Money, we make it

Fore we see, you take itInner City Blues, Marvin Gaye, 1970

Created in 2013 as a parody to mock bitcoin and offer digital alternative currencies to a wider audience, Dogecoin’s market cap is now worth more than Ford Motor Company. It is easy to dismiss this as just another example of a speculative bubble driven by loose monetary policy. History shows us that in times of crisis, governments use currencies to ensure their survival. At that point in history, currencies no longer become a reliable store of value. The Dollar remains the world’s reserve currency, for now – yet the U.S. government is likely to continue on the road of war-time stimulus. This war is not waged outside, but inside our countries. Our economies have become incredibly imbalanced, after decades of QE infinity and tax cuts, which have benefited the haves over the have-nots and created asset-rich but wage-poor recoveries. Today’s war is not against an external enemy, but against inequality.

As a result, we believe investors should consider alternatives to their allocation.

In the words of bond investor veteran Dan Fuss’ recent FT article titled Bond investing needs a complete rethink:

“Any major jolt that hits the markets, however, could undo the base for the substantial investor leverage that has made its way into them. It is assumed that leading central banks would race to support markets and that is, in most cases, a valid assumption. But leverage depends on confidence. Should confidence start to unravel, the excess liquidity would rapidly depart. Central banks are watching this carefully but might not be able to control it.”

In the second half of the year, we believe inflation volatility and discussions around tapering might bring back volatility to risk assets. Bonds and credit are the sleeping giant, with valuations at all-time highs and returns now barely compensating for historical risks.

Longer term, however, we believe investors should consider a scenario where policy becomes even looser – potentially with a change of Fed Chair – and the introduction of even more dovish policy measures. These include yield curve control, and eventually central bank digital currencies (CBDCs). We believe CBDCs, already used in China, could bring a sea-change in policy. The monetary policy transmission mechanism might change from top-down, from the central bank down to commercial banks and firms – to bottom-up, with direct monetary injection into sectors and firms.

We expect higher inflation, persistently negative real yields, higher taxes and more government intervention in economic sectors. Investors should look for alternatives. In our Global Credit Opportunities Strategy, we continue to be strongly invested in securities linked to real assets or real cash-flows, like convertible bonds and commodity sectors, while we maintain a neutral duration and a very selective allocation to credit.

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2021 Algebris Investments. Algebris Investments is the trading name for the Algebris Group.