When you see light at the end of the tunnel, it’s too late to buy.

Sir John Templeton

When fortunes are lost, fortunes can be made. Timing can make all the difference between the two. June marked an important month in the ongoing bear market, as by month-end many “buy boxes” had been ticked, at least in credit markets. Russia reduced gas flows, inflation increased further, and central banks were not budging on growth. All that could go wrong has gone wrong, and fear has taken over markets. When markets are in panic, the other side often pays off.

The current environment is the closest to proper capitulation we have seen in a long time. High yield credit had its worst month since the Covid crisis, and is now down 20%. Distress ratios in bond markets have rarely been higher. Current spread levels imply default rates comparable to the ones seen in 2001 and 2008. Bond inflows over the past two years have reversed in the space of a few months.

The second half of the year remains uncertain. Gas flows and geopolitics will determine how winter will be. Global economies will slow down, it is hard to say how deeply. A few political cycles will kick in (e.g US midterms, Italy, Turkey, Brazil). Inflation will ease, but monthly prints will remain volatile. Central banks will need to juggle slowing economies, high prices and volatile currencies.

The strongest signal comes from valuations. In credit markets, levels have turned extreme. Spreads have effectively delivered all the financial tightening Treasuries were unable to. Buying at these levels over the past 20 years has been a bargain. Spreads in line prevailing ones have been followed, on average 7% for corporates, 12% for financials, and 15% for emerging markets, over a one-year horizon. As such, now is an attractive entry point for long-term investors.

Inflation will moderate post summer. We expect supply constraints to ease in H2 meaning less manufacturing pressure, helping disinflation in both US and Europe. We have already seen healthy signs in the June prints, but volatile energy prices mean we will need to wait for September for the full impact. Peaking inflation means central banks will be less aggressive; good news for markets as the Q3 slowdown approaches.

The severity of the slowdown will depend on gas supply. However, easier-to-forecast factors point to a few silver linings. Firstly, consumer balance sheets are strong enough for a slowdown to be mild in the US. Secondly, current gas flows point to a mild slowdown in Europe too as a base case (although a cut-off would be more severe). Lastly, equity re-pricing is in line with what we have experienced in most recessions.

Europe will remain reasonably volatile, with gas risks peaking in October, and Italian risk back in the spotlight. Political fragmentation will continue to challenge ECB.

Things considered, we find this is a good time to add risk in credit markets. Uncertainty is high, but the post-summer period will bring clarity on some of the global worries. Credit spreads have already taken a very bearish view and are now pricing an extreme outcome. The opportunity looks cleanest in higher quality credit. Investors can lock in 6-7% with very low to zero chance of default. so that credit risk at 12% or higher seems unnecessary. We suggested to dip your toes back in June, but to keep your foot out of the water. We see now as the time for investors to put their whole foot in.

Credit slumps – history says buy

The June sell-off has been particularly severe for credit, turning valuations abnormally cheap. The outlook for 2H22 is uncertain, mainly because the outlook for energy security and inflation are hard to call. We have taken a step back to look at instances where spreads have been as cheap over the past 20 years as they are today. We expect investors to enjoy strong returns over the next 12 months.

Credit markets – emerging value

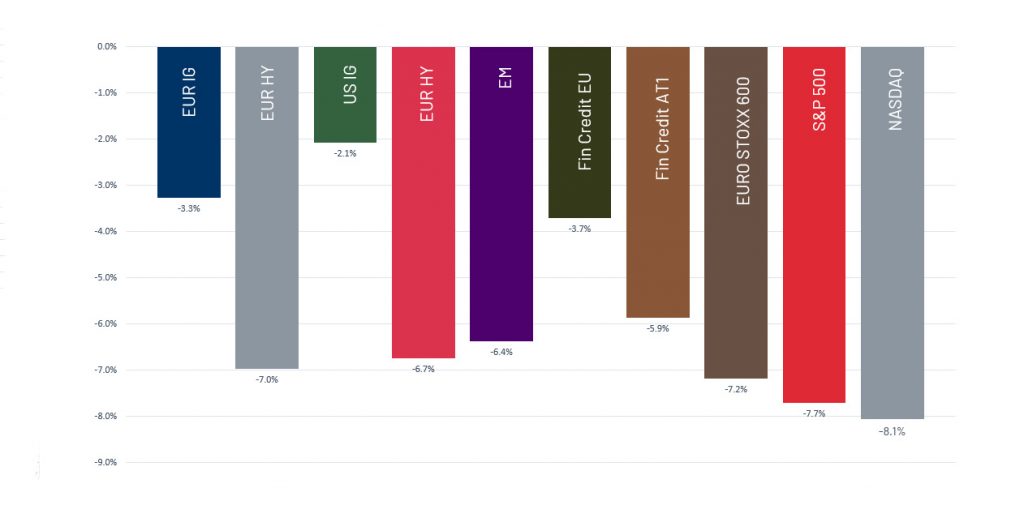

Source: Algebris Investments, Bloomberg Finance L.P., Total Return Data as of 01/07/2022

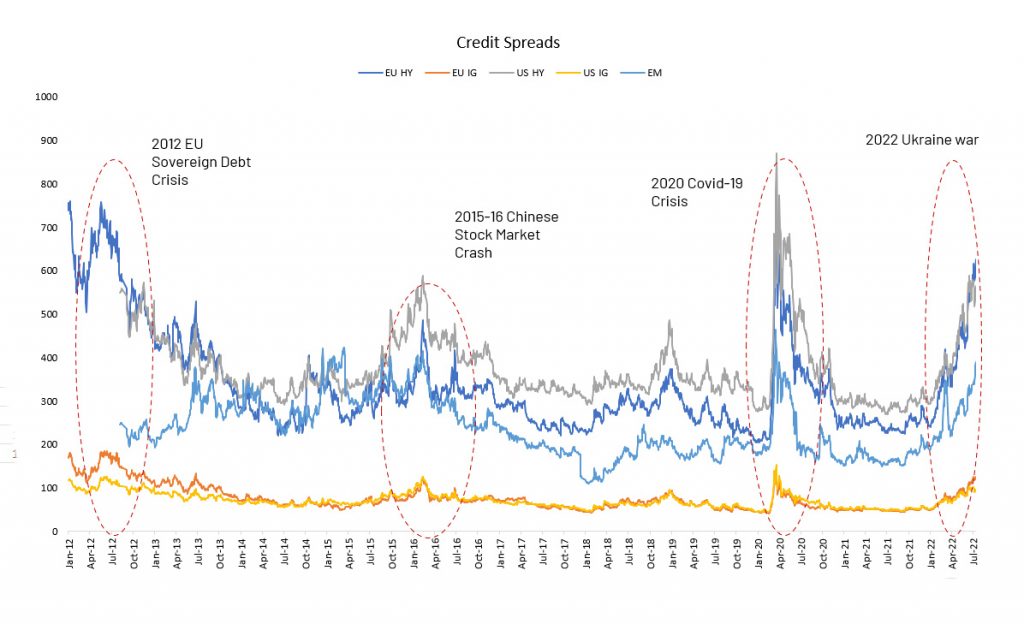

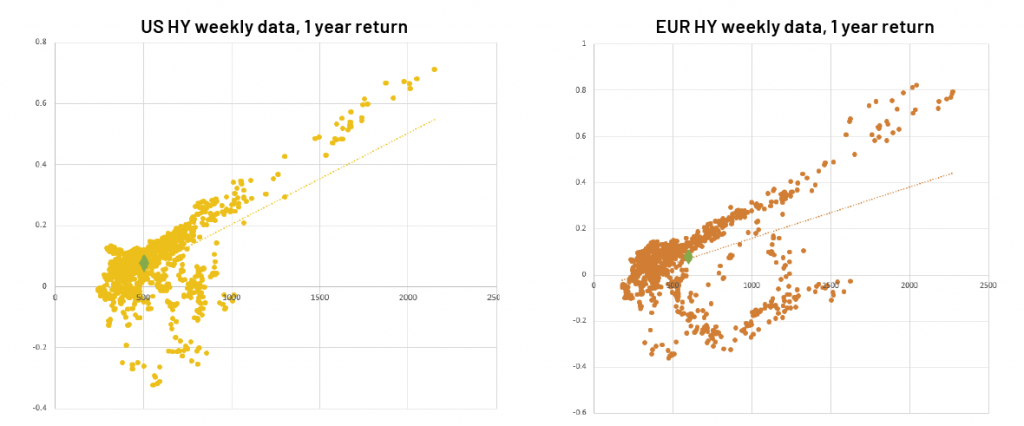

High yield performed as badly as equities in June (Chart 1), and spreads are now consistent with deep recessions (Chart 2). Credit markets have delivered all the tightening that long-end Treasuries and equities were unable to, and it is now priced for the worst. We see this as good news for credit investors. Over the past twenty years, spread levels in line with the current ones marked important entry points. On average, 12m returns from current levels have been 7% for corporates, 11% for financials, and 15% for emerging markets (Chart 3).

Source: Algebris Investments, Bloomberg Finance L.P.. Data as of 14/07/2022.

Source: Algebris Investments, Bloomberg Finance L.P. Data as of 14/07/2022.

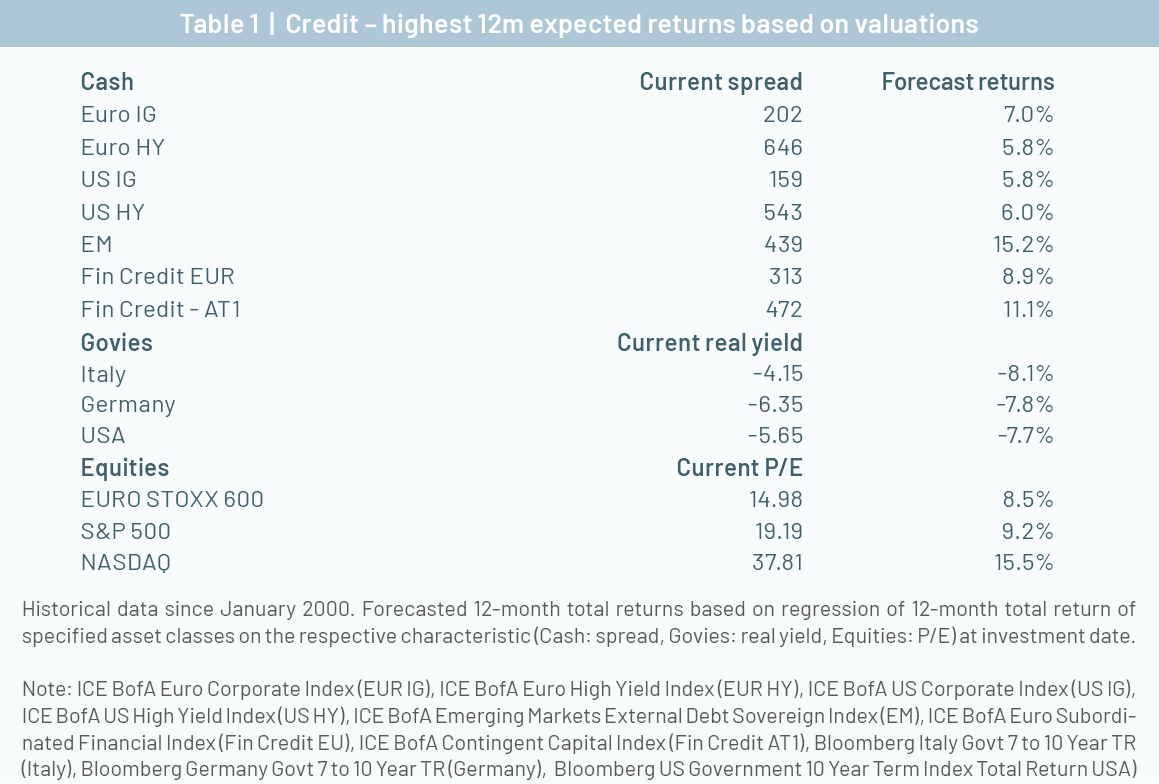

Investment grade bonds returned 5-6% on average, pointing to a relatively safe expected return. Historical attractiveness is unique to credit (Table 1). Government bonds tend to deliver losses starting from current real yields. Equity markets tend to deliver returns only as good as credit, vis-à-vis higher volatility. Valuations tell us that all the negativity on inflation and the economy is best reflected in credit, and that the amount of pessimism implicit in spreads has become excessive.

Credit valuations – stressed out

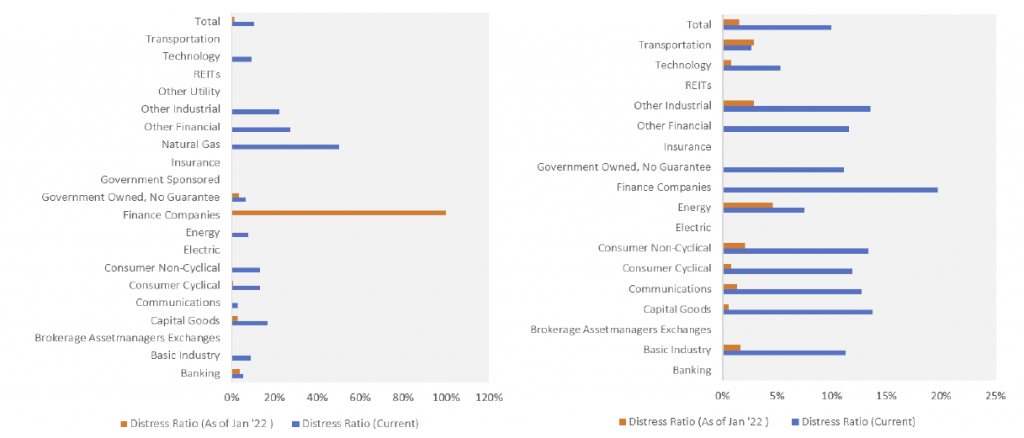

Stress levels implicit in valuations are also extreme. CDS indexes price 1y default rates of 2% for IG credit and 8-10% for high yield. IG defaults are extremely infrequent, while the high yield rate hardly crosses 3%. Distressed ratios point in the same direction (Table 2). In Europe and US, 10% of high yield credit pays more than 1,000 points of spreads, vs just 1% at the beginning of the year. In emerging markets, one sovereign in every three trades at distressed levels. Such levels of stress are consistent with a deep recession where financial conditions do not ease, a worst case for both the economy and monetary policy.

Source: Algebris Investments, Bloomberg Finance L.P. Data as of January 2022.

Flows – credit exodus

Fund flows also point to credit capitulation. ETF data show that outflows from high yield over 1H22 reversed two years of inflows. EPFR fund flows show that bond funds have seen $200bn of outflows so far this year, while equity flows remain in positive territory. Corporate credit funds have seen redemptions close to 80% of inflows since 2021. For emerging market funds, this number is closer to 150%. Credit indexes are down 15-18% YTD, not far from equities. Risk aversion is increasing mostly in credit, as investor patience for further underperformance is limited. Surveys report active credit funds cash levels around 15%.

Macro – tentatively deflating

Data worsened in June, increasing the chances of a recession. Markets are now factoring in this poor outcome. The equity drawdown we saw in the first half of the year is line with the maximum losses experienced in shallow recessions. Current pricing can be justified only by tail risk. Inflation will ease from September, paving the way for less hawkish central banks.

Recession risks – on the rise, but well in the price

Data across economies have surprised on the downside since June, triggering more aggressive pricing of a near-term recession. According to our internal model, chances of a recession in the US over the next 6 months rose to 30%, and the 12-month probability is now 60%. Similarly, 6-month and 12-month recession probabilities rose further in the Euro Area to 75% and 80%. Our model sees chances of a recession closer to 90% when using only financial variables, suggesting markets are fully pricing this outcome.

US recession – balance sheets say any recession will be “shallow“

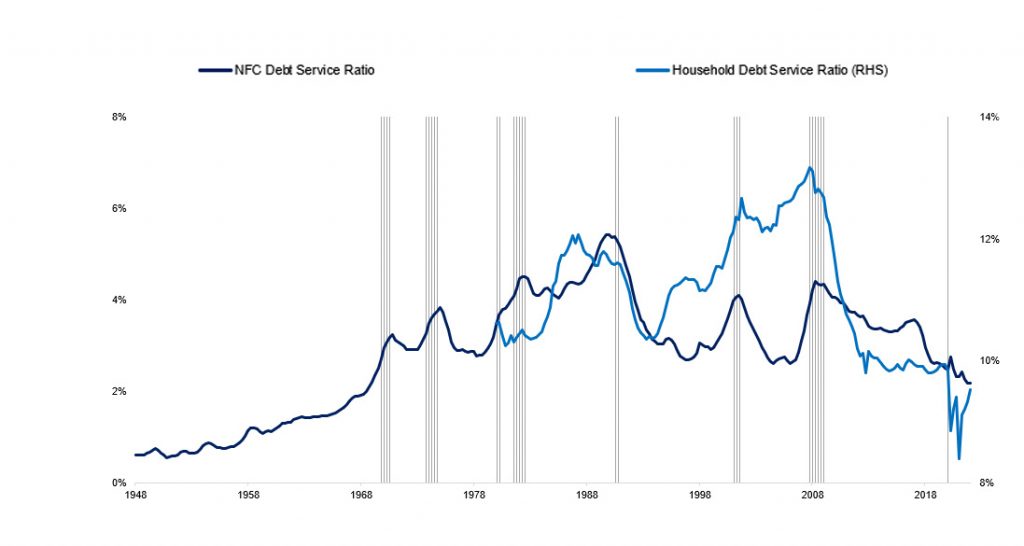

Consumer balance sheets are much stronger than they have been in previous recessions, especially in the US (Chart 5). Debt service ratios are near historical lows for both households and corporates. At the same time, households are still sitting on substantial Covid savings – by Q1 2022 even the bottom 20% have cash holdings 9% higher than their pre-Covid levels. Solid household wealth points to a higher probability of a milder slowdown.

Source: Algebris Investments, FRED, Bloomberg Finance L.P.. Data as of Q1 2022.

Shallow recessions – different animals

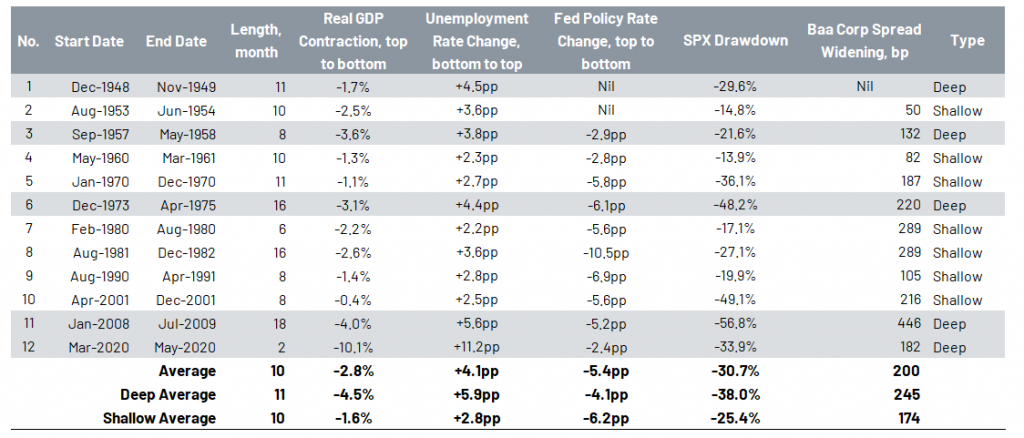

Shallow recessions tend to bring less acute market sell-offs. We studied 12 past US recessions since the 1940s and divided them into deep ones and shallow ones based on whether real GDP contraction or a rise in the unemployment rate in each instance was bigger than the historical average (Table 3). On average, real GDP contracted 1.6% in a shallow recession vs 4.5% in a deep one, while unemployment rose 2.8pp vs 5.9pp respectively.

Source: Algebris Investments, FRED, Bloomberg Finance L.P. Data as of end of June 2022.

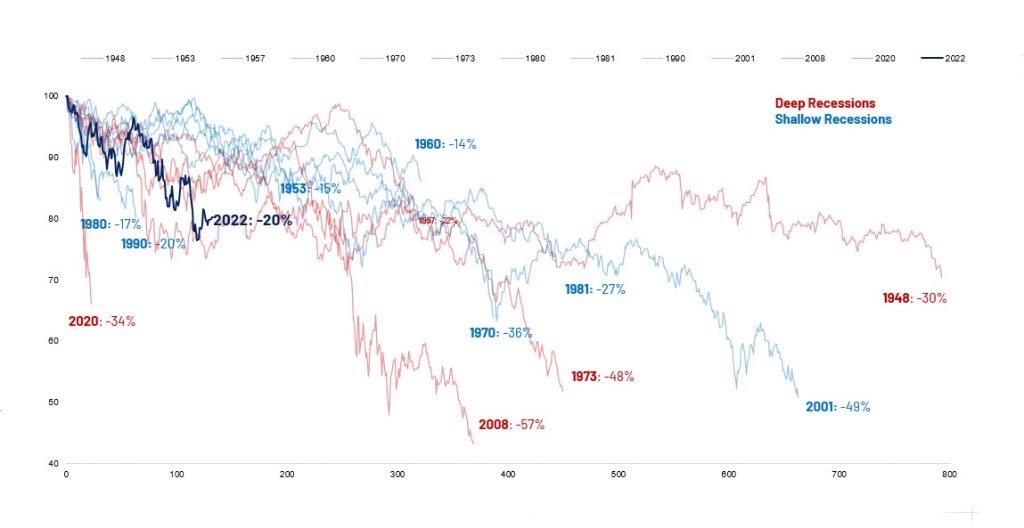

Asset performance suffered more in a deep recession, with average SPX drawdown of -38% and Baa credit spread widening of 245bp in a deep recession vs -25% and 174bp in a shallow one. The S&P drawdown experienced in 1H22 is thus already in line with a mild recession (Chart 6). The trough in equity performance tended to coincide with the shift in Fed policy towards easing.

Source: Algebris Investments, Bloomberg Finance L.P.. Data as of 11 July 2022.

Inflation – hard to believe, but we are peaking

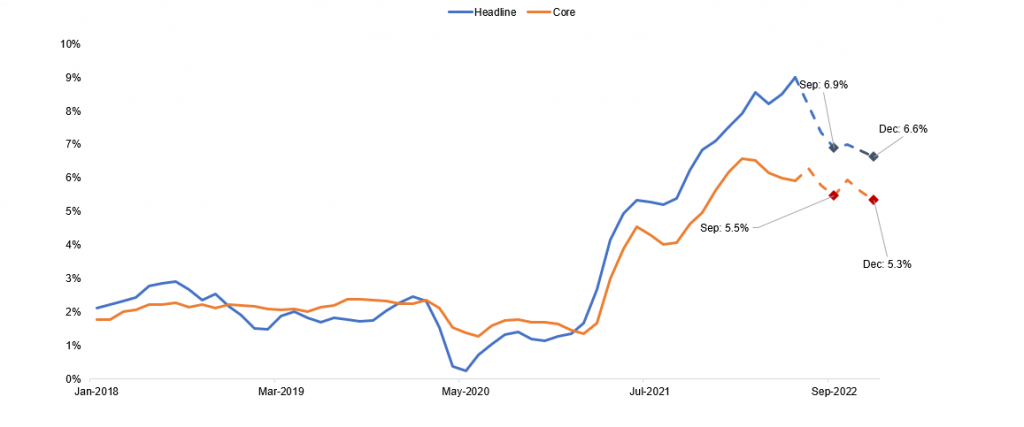

Inflation remained high in June, close to 8% in Europe and 9% in the US. Energy, however, has been the driver of the prints, directly and indirectly via core items. The median item in the core basket has stabilised in price, both in the US and in Europe. Manufacturing has seen a tentative drop, pointing to easing supply constraints. According to our model, inflation will start easing in September, with core inflation reaching 5% in the US and 3% in Europe by December (Chart 7). Disinflation momentum will trigger less hawkish guidance from central banks. Terminal rate pricing may have peaked at 4% in the US and 2% in early June.

Source: Algebris Investments, Bloomberg Finance L.P. Data as of 30.06.2022, projections as of 31.12.2023.

Europe – energy and politics

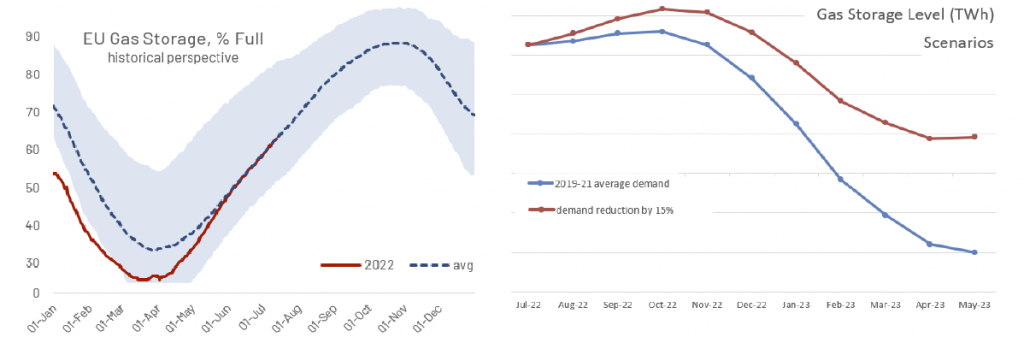

Uncertainty is on the rise in Europe due to energy policy and increased volatility in Italy. Gas remains a serious risk as current flows are only just enough to get through the winter. Any further restriction would require demand measures.

Gas – the biggest risk

Gas is the biggest risk to the European macroeconomic outlook. Gazprom has already cut-off its counterparts in 6 EU countries – for an equivalent 252 TWh. The share of EU’s gas supply provided by Russia dropped from over 40% in 2021 to just 20% in June 2022. The gap has been filled mostly by additional and more expensive imports of liquified natural gas (LNG), but there is now a risk that the Nord Stream gas pipelines may not be switched back on following the long-planned maintenance works it is undergoing this summer. If this scenario were to materialise, Europe would slide into recession and face significant pressure during the winter. In a full cut-off, storage would be completely exhausted around January or February 2023. Incentives to cut gas usage and for increased state aid is thus likely to be used extensively by the EC and national governments.

Source: Algebris Investments, Bloomberg Finance L.P. Data as of June 2022.

Conclusion

The first half of the year has seen one of the worst market slumps of the past twenty years. The hit has been especially bad in credit. Valuations, flows, and positioning all point to an attractive entry point for long term investors. As a severe case for the economy is priced in credit spreads, most outcomes should be favourable for investors. Historically, investing in credit at current levels has delivered 7-15% returns over the subsequent 12 months, depending on the market segment. We suggested dipping your toes in early summer, and see now as the time for a deeper dive in.

Davide Serra

Founder & CEO

Sebastiano Pirro

CIO & Financial Credit Portfolio Manager

Gabriele Foà

Global Credit Portfolio Manager

Silvia Merler

Head of ESG & Policy Research

Tao Pan

Head of AI and Big Data

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2022 Algebris Investments. Algebris Investments is the trading name for the Algebris Group.