The scars of others should teach us caution.

St. Jerome

The longer the party, the worse the hangover. The old adage certainly applies to 2022. The Fed’s balance sheet is 3x larger than it was in 2019, and easy money turned into all-time high household wealth. Couple that with the largest fiscal push since WWII and the worst supply shock since 1973, and something has to give. That something is inflation, and with it, markets.

Monetary stimulus and supply shocks combined into stagflation risk. In the US,the first quarter saw inflation top quartile and growth bottom quartile for the first time in 15 years. Europe’s future will be determined by energy politics, and China’s leadership continues to zero in on Covid. May data shows inflation is eating into consumer spending and corporate margins.The good news is that markets are now pricing in a bad outcome. Financial equities are dropping despite rates rising, pointing to equities pricing recession. Credit spreads have been higher only during sharp downturns. In contrast, re-opening tailwinds still support data, and the US consumer stays strong. Chinese authorities are becoming more pragmatic on stimulus measures. We may be set for a slowdown, but markets are quickly reaching very pessimist conclusions.

The bad news is that the margin of error has never been so narrow. With inflation running at 8% in both Europe and the US, central banks cannot afford to support the economy, even in a bad scenario. The ones that suggested this option have been punished with a weak currency, which in turn leads to more inflation. The start of QT and higher financing costs mean fiscal policy is severely limited. It may not be a recession, but the consequences of getting it wrong are very serious.

Markets are pricing in tightening in 2022, but terminal rates remain uncomfortably low. Investors are bracing for the “big peak” in inflation, but base effects alone won’t do the trick. Extrapolation of recent monthly inflation data over the next few quarters easily leaves US inflation close to 7%. Either something changes, or 2.5-3% terminal rates may just prove wrong.

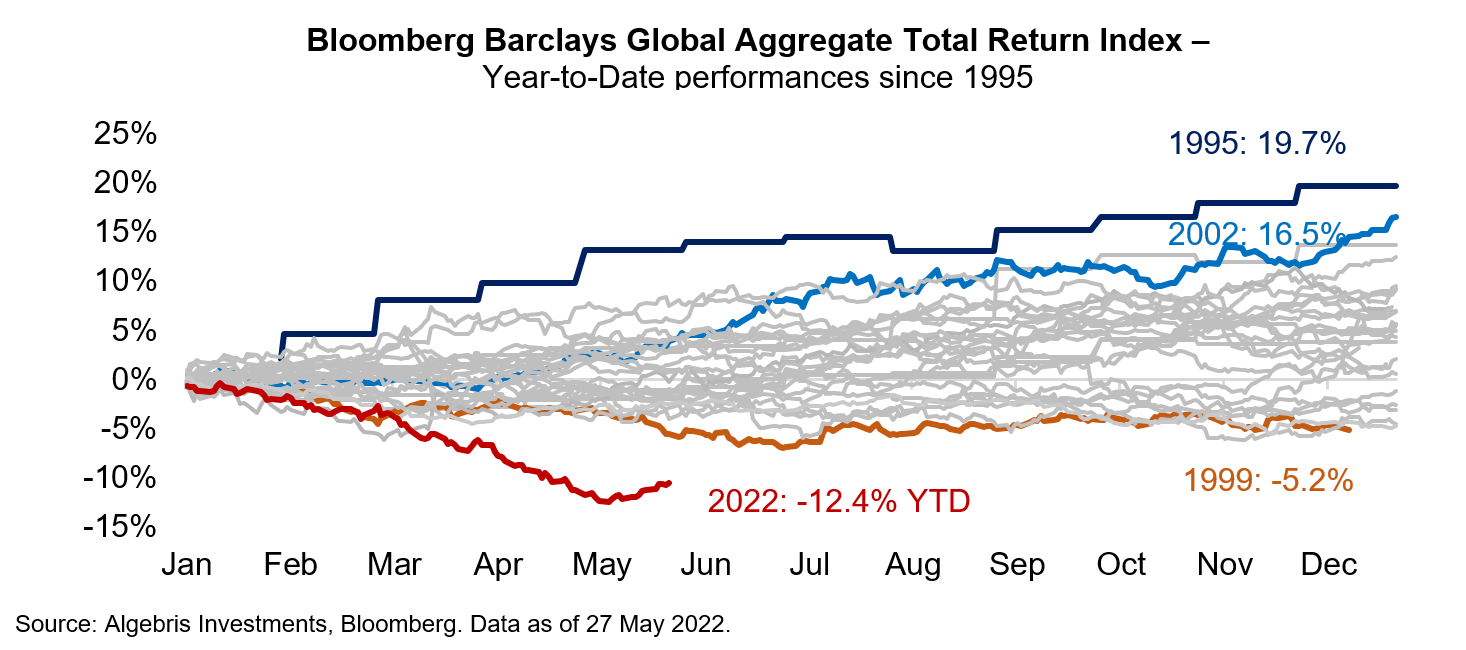

Nevertheless, bond markets feel like a much healthier place compared to six months ago. Negative yields are a story of the past, and US Treasuries just had the worst first half drawdown in history. Credit inflows from the post Covid bonanza have partially reverted, and cash levels are building up in an environment where new issuance is limited.

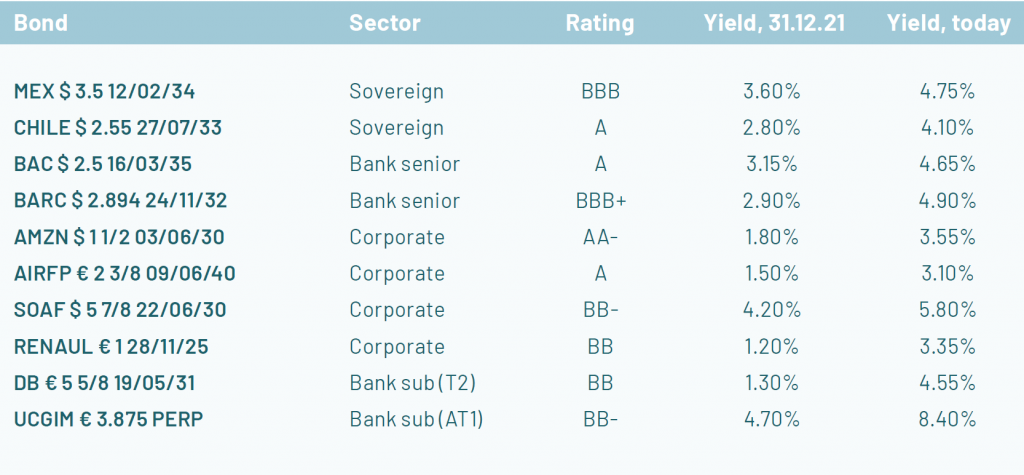

Broad pessimism and better bond technicals mean investors can dip their toes in risk assets, for the first time in a while. In our view, credit ranks better than equities. Spreads are finally attractive on relatively high-quality segments. Amazon 10y dollar bonds now pay 4%, a yield that could be found on Ivory Coast government bonds just one year ago. Locking in higher yields and the recession premium baked in spreads starts making sense, especially in solid issuers.

Opportunities are arising, but it’s not time to go all in. The “lower for longer” trade worked over the past ten years but will not work in the next three. Rising rates mean yields should be balanced with quality, and alpha generation and capital preservation remain key. Dip your toes, but keep enough of your foot out of the water. Macro volatility is back, and investors should be ready for it.

Macro – Inflated times

Inflation remains the major issue at a global level. April and May data offer little reassurance on peak inflation, hence the Fed will go full steam ahead with hikes and the ECB will start tightening. Inflation will rank firmly over growth in central bank reaction functions going forward. China is gradually re-opening, but the zero-covid policy will continue to constitute a risk over the next few months. Stimulus measures are finally picking up. Global data point to a slowdown, but macro factors suggest lower chances of a recession than priced in, especially in the US.

Inflation – shaky peaks pave the way for hawks

Inflation data remain high, as the increase in energy prices trickles down to core inflation, and goods inflation continues to be stronger than expected. Central banks have no other option but to continue with hikes. The Fed will hike 50bp in both June and July bringing rates to 3% by year end. The ECB will start with hikes in summer and deliver four hikes in 2022.

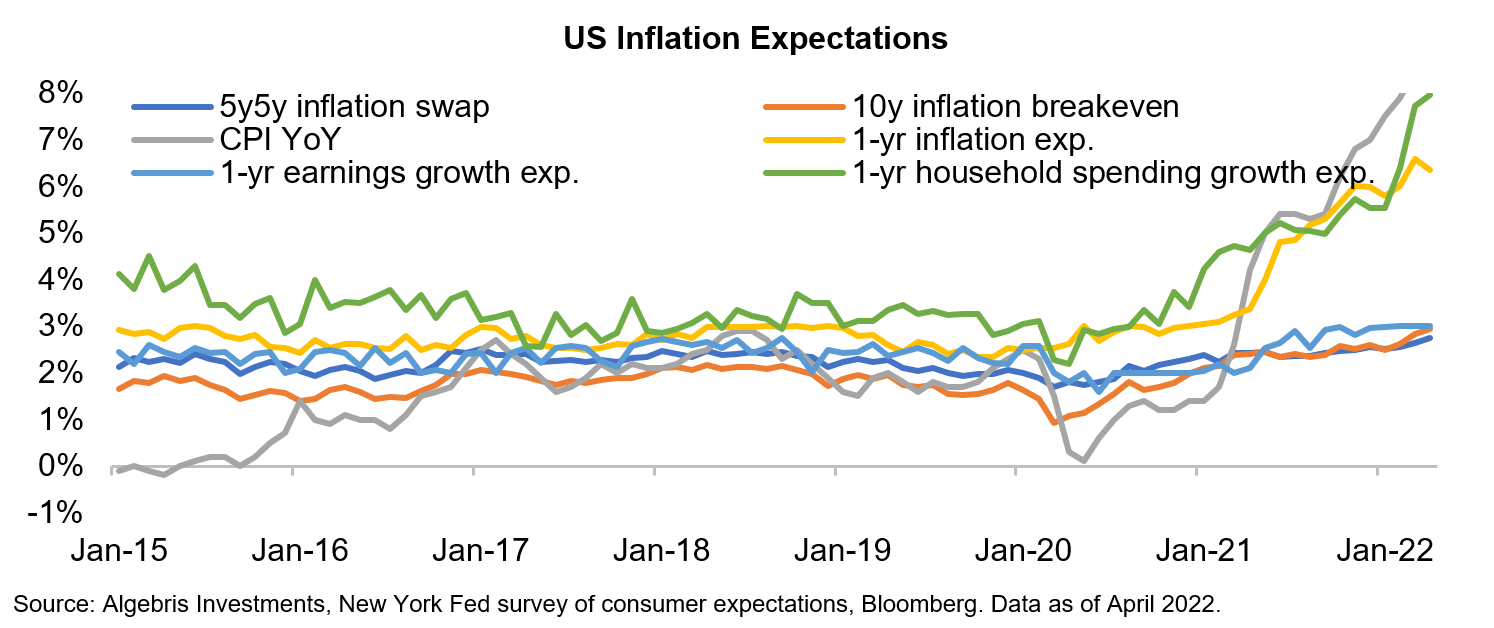

In the US, headline and core CPI grew 8.3% and 6.2% YoY respectively in April, a small deceleration from 8.5% and 6.5% in March but still above forecasts. Latest trends are in line with our previously shared view that inflation has likely peaked, but the descent may be slower than the Fed had expected. Core inflation will continue to decline in the coming months thanks to reduced supply chain stress and base effects. However, rent and core services inflation are likely to rise further due to rent growth and strong wage pressure.

All in, core inflation could be around 5% by year-end, putting pressure on the Fed to stick to a hawkish hiking path. The Fed’s balance of priorities has fully shifted to inflation, which is also becoming key in Biden’s political agenda. The US economy is also more resilient to hikes, given low energy dependence, no exposure to the war in Ukraine and strong private sector balance sheets.

In the Eurozone, inflation is still largely driven by commodity prices, with energy and food accounting for nearly 70% of headline growth. Energy price increases are also driving up production costs, with second-round effects on core inflation, which is now running just below 4%. May inflation has surprised on the upside, bringing the headline above 8%. Overall, inflation will remain above 7% in June and above 4% in 2022.

The ECB will have to catch up quickly with the Fed, as consistent upside surprises in inflation have put its credibility on the line. Comments in March and April had opened the door to a more dovish stance, immediately sending the Euro to new lows. Recent comments have re-established an anti-inflationary stance, so that action now needs to follow. The July meeting will bring about the first hike, likely 50bp, and we see rates close to 1% at the end of 2022.

Global data – landing isn’t crushing

Global economies are slowing down, as all leading indicators suggest to PMIs, but remain in expansionary territory, with readings into the low-to-mid-50s in US and Europe. Consensus forecasts for 2022 turned lower, but even the most bearish projections are above 1.5% for Europe and 2% for the US. Our models do not see chances of a US recession over the next 12 months being higher than usual. In Europe, chances are higher than usual but not extreme.

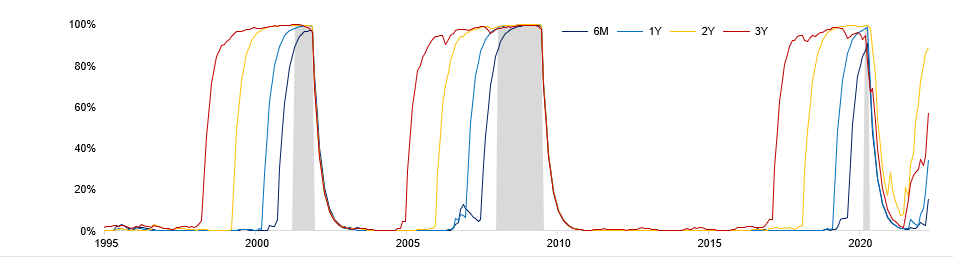

Source: Algebris Investments, Bloomberg, FRED-MD, ALFRED. Data as of end-April 2022 for economic variables and 30 May 2022 for financial variables. Data history since July 1963 covering 8 recessions as defined by NBER. Grey bars denote recessions.

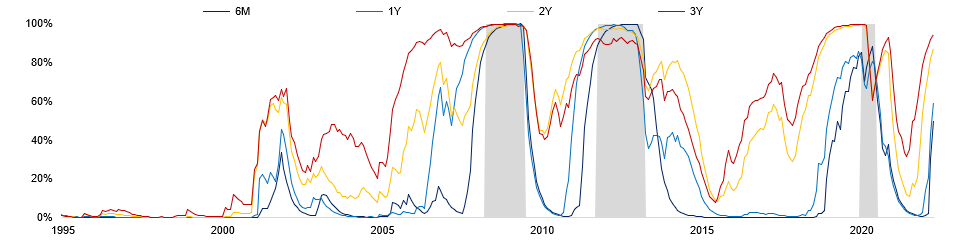

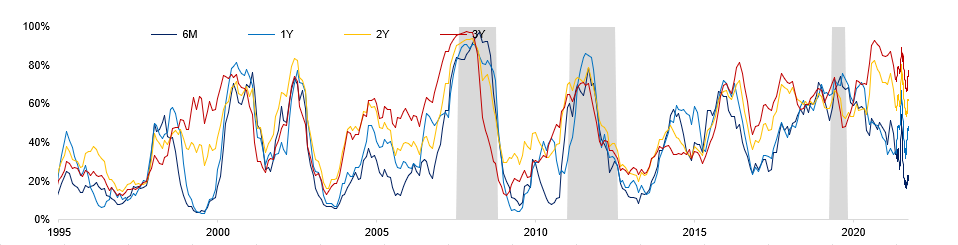

Our recession prediction models show that the chance of a recession in the US over the next 12 months has risen to around 30% in April, on par chances from any given month. Meanwhile, 24-month and 36-month probabilities are at 59% and 65%, above the respective unconditional probability. However, financial markets moved even further in pricing an imminent recession, with the 6-month probability implied by financial variables above 70%. The models suggest recession risks over the 2-3 year horizon are higher than normal, but market fears of a near-term recession are likely exaggerated for the US.

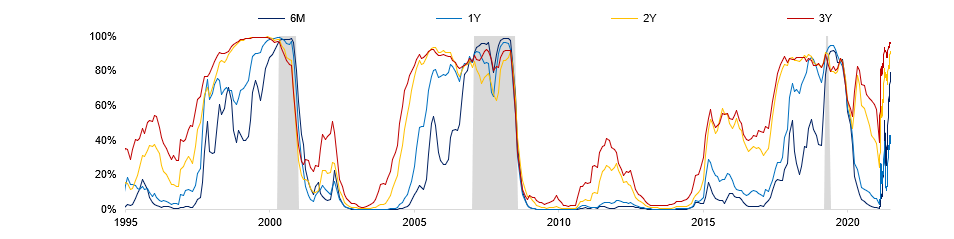

Eurozone 6-month and 12-month recession probabilities have risen significantly to 49% and 59% respectively in April, higher than unconditional probabilities. Eurozone models based on financial markets are struggling to interpret the unusual market signals, as risk-assets are selling off but yield curves keep steepening. Our models attach higher recession risks to Europe than the US. In addition to its higher exposure to the Russia-Ukraine war, the Eurozone is also more prone to a China-led slowdown given its higher export dependence.

Source: Algebris Investments, Bloomberg. Data as of end-April 2022 for economic variables and 30 May 2022 for financial variables. Data history since December 1986 covering 4 recessions as defined by EABCN. Grey bars denote recessions

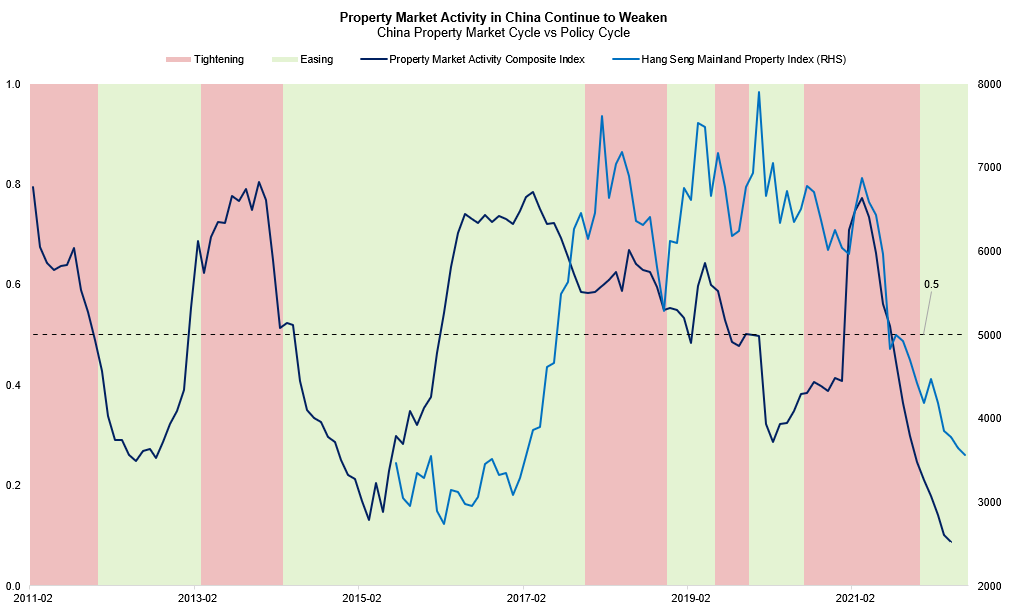

China – zeroing in

The latest Covid wave in China has largely been brought under control with nationwide daily cases dropping below 150 and the number of high-risk districts reducing significantly. Shanghai, the city that underwent the most severe lockdowns, started its broad-based reopening on 1st June. For now, it seems the worst of the Omicron disruptions is over. High frequency data such as passenger traffic, scheduled flights and road freight suggest that activity levels are recovering very gradually, unlike the V-shaped rebound we saw in 2020. May PMIs remained in contractionary territories, but show substantial improvement compared to April.

Following the drastic growth slump, the government has shifted to a policy easing mode. The PBoC cut the mortgage reference rate by 15bp on May 19th. The State Council announced 33 incremental measures to stabilise the economy on 23rd May, with focus on fiscal reliefs and infrastructure investment. Premier Li recently held a policy teleconference with local government officials to raise the urgency for supporting growth. The combined size of measures announced this year is now close to half of the stimulus size in 2020. However, the government is unlikely to depart from its zero-Covid strategy at least until the Party Congress this autumn given political considerations. Short term risks to growth therefore remain. The policy mix may become more favourable after the Party Congress, but 2022 growth will remain well below target.

Markets – dip your toes

Markets will remain choppy over the next 12-18 months. Investors have priced in hikes for 2022 and the first half of 2023, but there is complacency about medium-term inflation. Our analysis suggests that inflation risks are skewed to the upside on a two-year horizon. However, shorter term rates stability is likely to translate into a continuation of the recent relief rally. Most asset classes are now pricing a recession over the next twelve months with near certainty, and in fact economies may slow down but maintain positive growth. Credit – high grade in particular – may benefit the most as quality assets have cheapened amid yield and spread widening. In FX, we see upside in EURUSD and USDCNH. Longer-term, we think macro volatility will persist. Investors will need to remain tactical with their asset allocation and rank alpha over beta.

Rates – (too) much relax about peak inflation

Rates markets have appropriately priced in hikes for the next two years, but the degree of confidence into a quick 2022-23 disinflationary environment remains extremely high given what core data are telling us. The rates re-pricing has been aggressive on the front end, but remains more subdued out the curve. Markets are pricing a terminal rate of 1.4% for the ECB, and 2.8% for the Fed – 6% and 5% below current inflation. Markets expect a quick stabilization in inflation, which will spare central banks from hiking too much in later years. While it is hard to know whether this view is true, some early signs suggest the balance of risk is skewed towards higher inflation / rates.

First, financial conditions remain relatively loose. A flat US curve means outer tenors are well below spot inflation, with 2s10s spreads below 30bp and 5s10s essentially flat. Real rates implied by the linkers market are barely positive. Loose financial conditions despite 200bp of hikes priced in suggest the Fed has room to do more. Second, consumer inflation expectations are steadily outperforming market implied expectations, pointing to sticky spending and more pressure on wages. Finally, uncertainty around 2022 inflation expectations remain very high. Most forecasters predict a peak, but a small delay in the drop in monthly inflation matters a great deal. Ending the year with inflation above 6% would just require a continuation of recent monthly inflation trends, even accounting for (disinflationary) base effects.

Bond markets – A healthy reshuffle

Bond markets are a more attractive asset class compared to six months ago. The re-pricing of hikes has triggered the quickest US Treasury drawdown in history. A quick move brought about strong outflows, significantly improving the technical picture in several markets, especially IG and HY credit. A quick rates re-pricing triggered an equally quick widening in credit spreads, so that acceptable yields can be found high-quality segments of fixed income markets for the first time in quite a few years. US IG spreads widened some 40bp this year to nearly 80bp, with 5y US Treasuries widening 150bp to 2.7%. Major cash indexes in the sector now yield above 4%, with peaks of 5% and with virtually no credit risk. US high yield indexes offer yields above 7%. Yields and risk premia have increased uniformly across asset classes, so a portfolio with 5-6% USD yield and a very conservative risk profile is achievable in bond markets, for the first time in the past ten years.

The picture remains less rosy for developed markets government bonds, as large-scale central bank balance sheet unwinds provide headwinds. The Fed will shrink its balance sheet by roughly $6tn over the next three years, 2/3 of which is represented by Treasuries. The ECB will simply stop expanding its balance sheet, but previous purchases were skewed towards the periphery, which now needs to find new natural buyers. For Italian BTPs, for example, 30% of the stock is held by the central bank, vs less than 5% ten years ago, and 15% in early 2017.

Finally, rates volatility has been more important for markets than equity recently, so that a small relaxation is likely to trigger a rally in beaten-down areas of fixed income markets. Better valuations and cleaner positioning mean global credit has seen a substantial improvement in the technical picture over the past six months. The same does not apply to government bonds as QT headwinds remain strong.

The “R” word – too much in the price

In April, markets started pricing in the chances of a recession more aggressively.

Equity markets finally have more reasonable multiples, with cyclicals even 10-15% below the 10y average. In Europe, the correlation between bank equities and bunds has inverted since March, and earnings momentum has firmly turned to the downside across indexes.

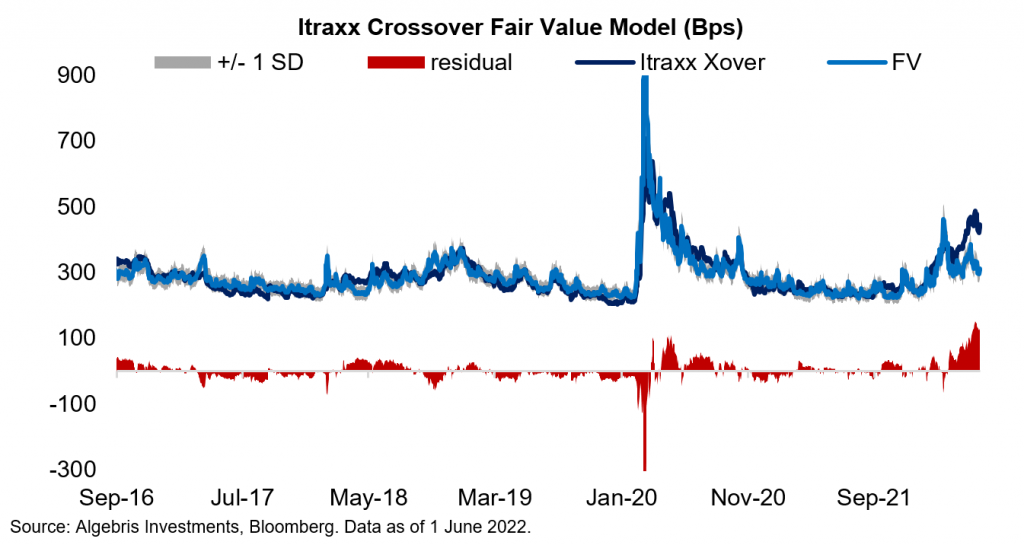

Credit spreads are at recessionary levels too. Current levels have historically been associated with a marked, and sometimes deep, global recession. European CDS indexes are trading 50bp wider than the worst levels reached in 2018. Our model suggests high yield credit spreads are the widest vs the risk implied by fundamentals since the Covid crisis in 2020.

As noted earlier, the bearish pricing is not entirely justified by data. Absent a sudden stop in gas flows, European growth will remain above 1.5% in 2022 and bottom in 4Q. The US remains strong, and China will grow above 3.5% despite a quarter of Covid-related blackouts. Higher energy costs bring some margin pressures. Still, the increases are concentrated in a few sectors – some of which are still enjoying post-Covid re-opening tailwinds, and plenty of government support. Corporate credit risk should not increase meaningfully as a result.

Stay tactical

The next two years will remain challenging for investors, as risks to central bank terminal rates are skewed to the upside and markets risk premia will re-price accordingly. In fixed income, only 4% of global bonds now yield negatively, vs 20% just a few months ago. Still, most bonds yield below their reference inflation rate, suggesting a “buy-and-hold” long bond strategy is unlikely to deliver satisfactory returns over the medium term. This is a strategy that many investors became too comfortable with.

We believe investors should adopt a tactical approach to asset allocation. The relief recently seen in markets may have another leg. Risk has turned a few weeks ago but technicals are improving and valuations are still attractive. Also, rates stability is unlikely to be challenged by more turns at central banks in the very near future. The difference between this rally and previous ones, at least in fixed income, is that relatively safe assets have historically attractive valuations as the selloff had been broad. Being long credit with ratings above BB and in safe jurisdictions is an attractive proposition at the current juncture.

Rates hedging will need to be put on before taking off risk in a stronger move. Risk assets are arguably overestimating chances of a recession, while real rates are too low for almost all inflation scenarios. So, risk remains overall more attractive than rates, and UST yield dips are an opportunity to hedge more.

Bottom-up, we see value in US IG and selected EM hard currency bonds with ratings above BB-. Those areas have underperformed credit markets and are cheap vs history and peers. In the former segment, US banks have seen substantial issuance in April and May (as opposed to all other markets), so they have less supply risk. In EM hard currency, we favor LatAm and commodity exporters. We remain negative on commodity importers in Middle East and Africa. In Europe, we favor selected industrial and re-opening names, mostly in the high-yield space. We see upside in EURUSD given the likely hawkish ECB turn.

The key macro risk – Europe and the energy problem

The key global macro risk is a sudden cutting-off of Europe from Russian energy – which would induce a 2022-23 recession and send inflation through the roof. While the recently agreed EU oil embargo has increased the chances of retaliation in gas markets, we think that a sudden cutting-off of major economies like Germany or Italy is unlikely (more so in light of their manifested willingness to abide by Russia’s new controversial rouble gas payment scheme). National policies on energy prices have averaged 1% of GDP so far in the EU, but the cost of energy independence from Russia is much higher. The EU will make larger resources available, but they may be unequally distributed across countries.

EU oil embargo – little and late

While the European block’s oil imports are more diversified than its gas imports. For Russia, on the other hand, the EU market accounts for about 50% of oil exports. The sixth package of EU sanctions including an oil embargo took weeks of negotiations to overcome a veto by Hungary – yet more proof of how controversial and politically polarising energy sanctions continue to be in the EU. The package that was agreed on 31st May is weaker than the original proposal and the difficulties in striking agreement make the prospect of a politically more controversial EU ban on gas less likely than it had appeared a few weeks ago.

The gas standoff – higher risk of retaliation

On May 18th the European Commission published REPowerEU, a plan setting out how the block will achieve energy independence from Russia by 2027. Meanwhile, the move to impose an oil embargo increases the risk of retaliatory actions on natural gas by Russia – which has already interrupted flows to five major EU energy companies for not paying according to the rouble gas payment scheme. Gas storage levels have continued increasing over recent months across the EU, storage is still far below the 80% target to be achieved by November 2022. An interruption of Russian gas supply to Europe would therefore be a significant shock for the EU’s economy – shaving 2-3 pp on GVA even assuming optimal rationing and production cuts.

REPowerEU – a test for EU coordination

Between Q4-2021 and Q2-2022, EU countries have spent on average 1% of GDP to shelter consumers and firms from the impact of higher energy prices. Achieving independence from Russia will require an additional investment of EUR 210 billion over 5 years.

Countries will be able to use their unclaimed share of loans under the Recovery and Resilience Facility (RRF) to finance REPowerEU investments. So far, only seven countries had applied for RRF loans – leaving a residual amount of EUR 225 billion. The European Commission plans to also issue new RRF grants to be funded by the auctioning of Emission Trading System allowances currently held in the Market Stability Reserve, worth EUR 20 billion. As a share of GDP, the EU will make available funds worth on average 5.5% of GDP that countries will be able to use to compensate for higher energy prices and accelerate the transition over the next few years. But for those countries that have already taken all or a large part of the Next Generation EU loans, the amount will be much less. Italy, Greece, and Romania will have access to a mere 1% of GDP in extra RRF funds to use for REPowerEU purposes – unless some other Member States decide to give up the RRF loans they are entitled to.

Conclusion

Stagflation fears and the unwind of the post-Covid stimulus has brought about a massive market re-pricing in the first half of 2022. Bonds and equities corrected at the same time, and US Treasuries lost 12%, their biggest first half drawdown ever.

There was nowhere to hide for investors, so outflows picked up across asset classes, particularly in fixed income. The “clean-up” leaves bond markets a healthier place than it has been in the past three years. Spreads are now pricing in a recession, and economies are slowing but still in expansionary territory. Higher yields and peaking spreads suggest high quality bonds will start paying attractive yields again, and positioning is cleaner.

Credit has re-priced more than equities, and looks more attractive. Volatility will remain high, so investors should maintain a tactical approach, and stay focudes on alpha and capital preservation. We see inflation as the key risk for markets, more than a recession. Rates tightening is well priced for 2022, but terminal rates are likely to rise given sticky inflation. European energy policy is the main risk for the economy. We see no signs of an imminent gas cut-off, but a sudden change would precipitate Europe into a recession as early as 2022.

Davide Serra

Founder & CEO

Sebastiano Pirro

CIO & Financial Credit Portfolio Manager

Gabriele Foà

Global Credit Portfolio Manager

Silvia Merler

Head of ESG & Policy Research

Tao Pan

Head of AI and Big Data

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2022 Algebris Investments. Algebris Investments is the trading name for the Algebris Group.