“We are at war.”

– Macron, President of France

“If we start now, we can be ready for the next epidemic.” Five years ago, in 2015, Bill Gates warned the world about the lack of an organized system to deal with global health risks. Today, policymakers around the world have found themselves unprepared to deal with Covid-19, with the virus winning the first rounds of a longer battle.

We have been cautious since January on macro and markets, raising a high proportion of liquidity across all funds. To navigate this storm, we are looking at three developments: first, the impact from the virus; second the policy response in particular from governments, as central banks have almost exhausted their ammunition; third, investor behaviour and valuations. Unlike when we wrote The Silver Bullet I Nothing Left To Buy, earlier in February, markets are now ripe with opportunities.

What does a Covid-19 recession look like?

We can think of recessions of three kinds. The first happen when a financial system overhang falls, like in 2008 – a financial crisis. The second, when policymakers make an error, like central banks taking out the punch bowl too aggressively – this is a policy recession. The third because of external economic shocks – a real economy recession.

The good news is economic shocks caused by external catastrophes tend to last less and are followed by a quicker recovery, compared to financial crises, where debt overhangs remain in the system for years.

The base case is therefore of a deep but short recession, with Q2 experiencing -8%/-10% YoY growth, followed by a V or more likely a U-shaped recovery, depending on the size of fiscal stimulus at play.

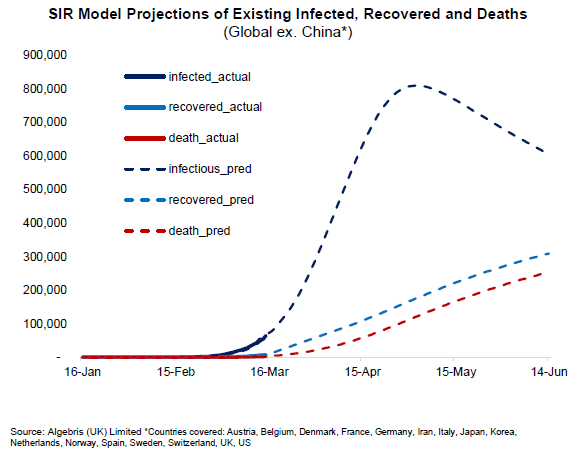

Projecting global spread of the coronavirus: a SIR model

It is difficult to accurately predict the course and eventual scale of the Coronavirus outbreak, given migration flows and evolving policy responses. To better understand how the outbreak might unfold, we use a classic epidemic model to simulate the potential rates of spread of infections globally, outside of China. Based on the current trends, our models suggest that:

– The number of new daily cases is likely to continue increasing over the coming weeks, reaching a peak around early April.

– The number of existing infected cases is likely to peak around the start of May.

– The total number of infected cases cumulatively could be close to 1.1mn.

In addition, our models suggest a likely change of infection epicentre from Europe to the US in the coming weeks. As shown left, the projected peak in daily new cases in the US lags major EU countries by about three weeks and lags the UK by slightly over one week. Within major EU countries, our models suggest that Italy is likely to peak first, followed by Spain, then France and Germany.

Fiscal policy: the key to recovery

In addition to healthcare measures to contain the virus, fiscal spending is paramount to minimise its economic impact and to avoid falling into a deeper demand slump. For fiscal spending to meaningfully impact the economy and financials markets, it needs to be announced soon and it needs to be large.

We think timing is critical. The longer fiscal spending is delayed, the greater the damage to demand might be due to subsequent effects such as companies closing and large-scale layoffs.

At the same time, the package needs to be big. We estimate that the impact to global Q2 GDP from Covid-19 could be almost -8% for the quarter, or around -2% for FY2020, implying that a package needs to be at least of the same magnitude to be relevant.

Put simply, we need Europe and the US to approve around a $400bn package each, within the coming weeks. We think governments will deliver, though the timing is uncertain.

The US government may pass its second Covid-19 bill this week, bringing total stimulus to $8.3bn. But recent announcement by Treasury Secretary Mnuchin discuss a bi-partisan $850bn package, which could reach as much as $1.2tn. This expanded package could include direct cheques to individuals, tax-relief or delays, loans to severely affected sectors and support to SMEs, according to Politico. While the details on the package size and its constituents is too early to comment on, the magnitude being discussed is certainly of a size which could help cushion the US economy. In terms of timing, major legislation would more likely pass after the Easter recess, but if the situation in the US deteriorates rapidly, we could see a bill presented as early as the next two weeks.

In Europe, following the European Council Members meeting in March, the Eurogroup has supported fiscal measures at 1% of GDP, in addition to 10% of GDP in liquidity facilities (including deferred tax payments) and automatic stabilisers. However, these measures are to be coordinated and implemented at the national level, as seen by Italy’s potentially €28bn (2% GDP) package, France’s €45bn (1.6% GDP) package, Germany alluding to a €550bn “bazooka” (13% of GDP) and Spain announcing an up to €200bn (20% GDP) package. The Eurogroup also welcomed the Commission’s proposal for stimulus at the European level backed by the European budget, including €8-20bn in liquidity facilities for SMEs and between €37bn-€65bn in investments across healthcare, small businesses and other vulnerable sectors. Though it is yet unclear how much of this is new vs existing funds.

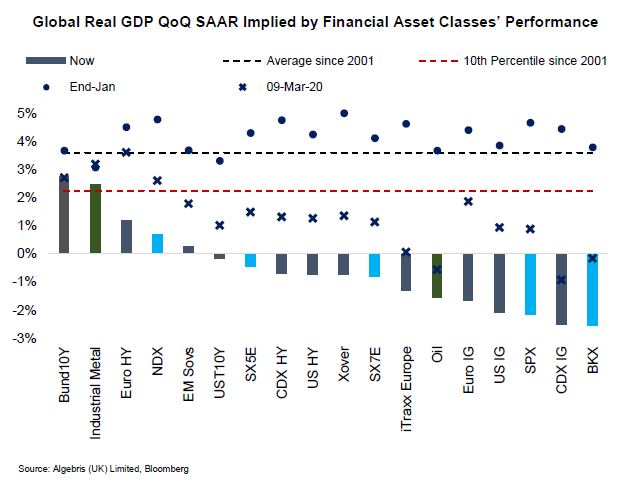

Market valuations: pricing in a recession

While the outlook for the virus spread remains uncertain, risk assets have already priced in a severe economic downturn. In some areas like credit, the economic shock has been compounded by unwinding of leverage and a liquidity shock, also evident from stress in short term funding markets. We long argued about rising fragility in financial markets, for example in our Silver Bullet | The Age of Fragility. The good news is valuations reflect the sharp deterioration in global growth and have overshot in many areas, as shown below. The bad news is the size and duration of the unwinds may be take longer, given the proliferation of leveraged strategies and carry trades over the past ten years of QE.

Oil markets and geopolitical risk

A failure to agree on production cuts by OPEC, as well as expansion in Russias production have further depressed valuations in credit and sovereign markets. Low oil prices are likely to persist for a few months, in our view, but will eventually normalise.

It is not clear why the OPEC+ meeting failed, but one possible explanation is that Russia is taking advantage of already weak oil to impose a fatal hit to US shale oil. Many US shale companies have production breakevens around $40-50/bbl and a leveraged balance sheet. Russia, on the other side, has a strong financial position: high reserves, a conservative fiscal policy, and a flexible exchange rate regime. In this environment, Russia can wait longer.

However, the same can’t be said about the original members of the OPEC cartel: Saudi Arabia, the Gulf States, and African and Latin-American producers. Such countries tend to have low production costs, but use oil as the sole resource to feed the whole economy. As a result, these economies lack diversification and have very high oil fiscal breakevens. Many OPEC members would face serious financial stress if current oil levels would persist for 12 months. Saudi Arabia is no exception, as reserves have been challenged in the 2014 oil slump and they still need to defend an overvalued peg of the exchange rate. As such, post an initial confrontation, chances of a cut in production from OPEC members seem quite high.

What are the permanent consequences from the epidemic?

There are permanent implications from what we are living. The risk is that short-term quarantine may turn into long-term isolationism, both within societies, across industries and countries.

First, social distancing may become part of our daily lives until a vaccine is developed. The transport and retail industry may face structural transformation as a result.

Second, industries will likely adapt to diversify their supply chains, similar to what happened after 2008 – where the survivors diversified their sources of funding. The reliance on offshoring production to China could diminish in a trend of geographical diversification and deglobalisation.

Third, politics will also likely change. Some of the hardest-hit countries may remember who gave or didn’t give them support at times of crisis. A recent survey in Italy shows 67% of Italians considers the EU a disadvantage, up from 47% in 2018. This increase may be further fueled by the fact that while Europe is now on track for some amount of common fiscal measures, the initial approach remains a state by state piecemeal strategy.

What we are doing right now?

In our previous Silver Bullet from early February, we warned investors about market complacency and high valuations across risk assets. As a result, we decided to reduce risk and to keep a very high proportion of our portfolios in cash.

Our approach to portfolio construction in an overvalued/complacent environment has been the following:

1. Reducing longs and raising cash to over half of the Macro Credit Fund.

2. Adding systemic protection in credit indices and equity indices.

3. Adding shorts in single names vulnerable to a slowdown in transport and tourism – including airlines, shipping and hotel companies.

With a net invested amount below 50%, excluding hedges, we ended February flat. However, our portfolio suffered in March on the Saudi-Russia oil war, with some emerging markets and a few corporates we own being directly or indirectly hurt by lower oil prices. That said, we still hanged in vs most competitors and fixed income indices, down between -15% and -25% this month. We also have the benefit of plenty of dry powder to deploy.

We think current market valuations are becoming attractive.

As one of our investors put it we have gone from “nothing left to buy” to “everything on sale” in just three weeks. This means that most asset classes today are pricing in a heavy recession, including those which are directly targeted by central bank purchases, like European investment grade credit.

Armed with lessons from 2018, we are aware that market volatility can last for some time. We are watching three developments to become more positive.

The first is the virus contagion dynamics. Our models tell us the virus would peak in around 4 weeks, however, much depends on the lockdown/social distancing strategy adopted by each country.

The second is the economic policy response. Monetary policy has reacted quickly and aggressively, with both the ECB and especially the Fed ramping up asset purchases and the potential to do more in the credit space, as suggested by former Fed Chairs Yellen and Bernanke. This suggests a relatively limited risk of tail/large scale defaults in investment grade firms. However, fiscal policy remains behind so far, with the US and Europe still figuring out the final amounts and the contours of private sector support. Until fiscal policy takes the lead, we remain cautious on high yield firms. Gradually, we see a combination of monetary and fiscal policy taking the lead, moving what we described as QE infinity to a different level. Most fiat currencies will depreciate, and real interest rates will likely stay negative.

The third factor is investor behavior. Over the past few days, we have seen disorderly price action: safe-haven assets like gold sold off and rates widened with risk assets down. These moves suggest a rapid unwind of leveraged strategies like risk parity. The size of these strategies can be substantial, even when compared with central bank balance sheets – we estimate around $1tn in risk-parity strategies globally, unlevered. In addition, the microstructure of fixed income markets has become more fragile, as we wrote in the past in The Silver Bullet | The Age of Fragility. ETFs with a relatively illiquid underlying and liquid liabilities also sold off very rapidly, trading well below their NAVs.

For investors with a long-term horizon, current market dislocations offer value.

Even though the virus spread may lead to a recession, price discounts across most asset classes provide a large cushion for negative scenarios. Across all our Algebris funds including Macro Credit in particular, we have accumulated ample liquidity. Over the coming months, we will gradually deploy this dry powder and lock-in selective opportunities in high quality assets, which may benefit from future fiscal stimulus and persistent low interest rates.

“With the enemy’s approach to Moscow, the Moscovites’ view of their situation did not grow more serious but on the contrary became even more frivolous, as always happens with people who see a great danger approaching. At the approach of danger there are always two voices that speak with equal power in the human soul: one very reasonably tells a man to consider the nature of the danger and the means of escaping it; the other, still more reasonably, says that it is too depressing and painful to think of the danger, since it is not in man’s power to foresee everything and avert the general course of events, and it is therefore better to disregard what is painful till it comes, and to think about what is pleasant. In solitude a man generally listens to the first voice, but in society to the second.“

– Leo Tolstoy, War and Peace

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2020 Algebris Investments. Algebris Investments is the trading name for the Algebris Group.