Tonight, some investors in bitcoin remind me of a ruined gambler who, standing outside the casino at midnight, just realizes he lost the keys to his car.

Nassim Nicholas Taleb

Like Pixie Dust making any asset fly, loose monetary policy and negative real rates have acted as a boost for financial markets over the past decade. Until the Covid-19 crisis, however, monetary easing was acting in isolation, just like an anaesthetic administered to a patient requiring specific surgeries. Low rates and quantitative easing were ineffective to boost growth and inflation. With the pandemic, fiscal and monetary stimulus are acting in conjunction, and central bankers finally have to deal with the consequences of their actions: inflation.

Prior to Covid, the equilibrium of low interest rates, low corporate tax rates and globalisation allowed prices to stay low and profits to rise, satisfying both the elites in the West and China’s growth ambitions in the East. This low-rate, low-tax policy mix enabled asset price growth without substantial wage growth. Rather than higher wages, low goods prices and leverage kept consumers going – what Raghuram Rajan defined as let them eat credit.

Today, politics are changing. With wealth inequality at a hundred-year record, the pandemic has shifted bargaining power from asset-owners to workers. This trend is likely to persist. People born after 1985 currently own less than a fifth of all financial wealth. Left out by economic policies favouring asset growth over wages and productivity, millennials will become the median voter within the next decade, in both North America and Europe.

What do you think they will demand?

The Biden administration’s priority is no longer jobs – it is taming inflation and boosting purchasing power. The Fed, the ECB and Bank of England are behind the curve. Normally, a tightening cycle would start at a time of rising growth momentum. This time around, however, central banks are likely to tighten as fiscal stimulus fades.

In 2022, Jerome Powell will have the most difficult job in financial markets. The Federal Reserve will have to choose between keeping asset prices, or their credibility, afloat. Markets are currently pricing in four hikes this year, but we believe more might be needed to tame inflation, as geopolitical risks and energy prices continue to rise. This means the Fed might have to hike faster, suddenly slamming on the brakes, at the risk of throwing some investors through the windshield.

Price action so far reflects an emergency rotation into unloved value assets which benefit from inflation and higher rates and out of crowded growth assets. The move has been relatively orderly – and yet, the tightening cycle has not even started. After many years widespread asset gains, we are preparing for volatility and dispersion in 2022.

1. What is the outlook for Covid restrictions in 2022 and the potential market impact?

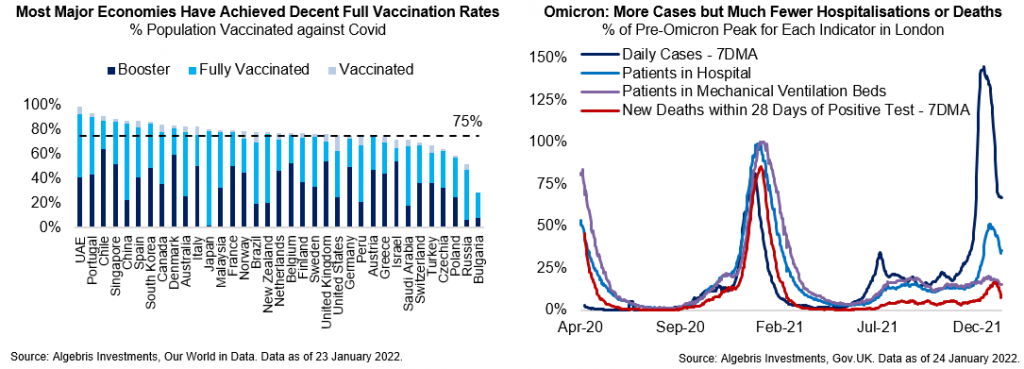

We think most major economies except China are on their way to easing restrictions and reopening. The dominant Covid variant today has become more infectious but much less fatal, more people having acquired immunity through vaccines or infection. Moreover, we now have better Covid treatment knowledge and tools, like the Pfizer and Merck antiviral pills.

Since late December, the fast spread of Omicron led to an explosion of cases globally and triggered tighter restrictions or pauses in reopening in some countries. However, more evidence has emerged to suggest that Omicron infections tend to be milder and less likely to cause hospitalisations or deaths. In London, the first Omicron epicentre outside South Africa, daily cases shot up to near 1.5x of pre-Omicron peak, while hospitalisations only rose to 51% of previous peak. Moreover, hospitalised patients are less likely to need ventilation support and much less likely to die. As a result, more governments are turning to ease restrictions despite still rising cases. For example, the US, the UK and several EU countries have shortened Covid self-isolation periods. Italy scrapped its quarantine requirement for vaccinated people who come in close contact with positive cases. France will ease travel restrictions for travellers from the UK.

The move towards co-existing with Covid means the Omicron disruptions to growth and labour supply are likely to be temporary across developed countries. It should also boost reopening sectors as international travel further recovers. The exception to this transition is China, which so far has not indicated any likely shift from its zero-Covid strategy, as we discuss below. There also remains the tail risk of a more deadly new variant emerging, though rising global vaccination coverage and immunity acquired through widespread Omicron infections should reduce that probability.

2. What is the outlook for inflation?

Inflation is likely to persist and stay above central bank targets in the US and UK, as supply bottlenecks persists in goods and labour markets and demand recovers. Inflation will be lower but sticky in the Eurozone too.

In the US, the Fed is expecting inflation to remain above 2% until 2024. We think US CPI will remain persistently above target at around 3-4%, even into year end, due to the combined impact of both supply side constrains and, to quote Fed chair Powell, “very, very strong” demand.

On the supply side, firstly, we expect supply chain issues to persist, as highlighted by the still-rising lead time for chips, long wait times at LA ports, and Maerk’s recent report on continued global delays. Secondly, labour shortages should ease relative to 2021, but we expect the labour market to remain tight. The unemployment rate reached a near all-time low of 3.9% in December, as the participation rate remains low. This is due to both temporary issues, like Covid-related sick leave, and structural issues like workers exiting the hospitality industry. Finally, Covid highlighted the risk of relying on an international supply-chain and we expect the onshoring trend to continue. The OECD has estimated that the advent of globalization in the late 1990s decreased CPI by between a 0-0.25% per year, in OECD countries.

On the demand side, firstly, pent-up savings have declined from their Covid highs but still remain in line with pre- Covid levels. Secondly, fiscal stimulus will ease in 2022 vs 2021/2020, but remains above pre pandemic levels, as we detail in the answer to question 4. Finally, the transition to a greener economy is inflationary through creating additional demand for labour and raw materials. GS research estimates that $6tr in green capex is required globally over the next decade vs only $3.2tr spent between 2016-2020. Even if $6tr is not achieved, the expenditure is likely to remain above the pre pandemic level. Our research shows that had CPI globally included the cost of paying for our CO2 emissions, the price level today would be 50% higher than it is estimated to be.

In the UK, the BoE expect CPI to remain above 2% until end-2023 and we also see persistently higher inflation. The supply and demand side drivers of inflation are worse than the US. On the supply side, in addition to global shortage issues, the UK continues to be affected by labour shortages caused by Brexit. The government has attempted to increase labour supply from non-EU countries, but this has had a limited impact thus far. On the demand side, UK household savings rates and wealth still remain higher than pre-pandemic levels providing additional impetus to persistent inflation.

In Europe, we think inflation will remain higher than pre-pandemic levels but might less sticky than in the US or the UK. The reason is that unlike UK and US inflation, European inflation is almost entirely due to supply side constraints and higher energy prices. That is, services have not significantly contributed to inflation, given still significant slack in labour markets. Or to put it simply: the larger labour market slack in Europe has meant that higher energy costs have not caused significantly higher wages and therefore services inflation. However, this could change if European growth and demand continues to strengthen, buffeted by higher than pre- Covid savings rates and the transition to green energy – as recently highlighted by ECB board member Schnabel, the green-transition is inflationary and not fully accounted for in the ECB’s current inflation forecasts.

3. How many times will DM central banks hike and how will that impact risk assets?

Central banks are behind the curve in fighting inflation. We expect over four Fed hikes in 2022, which will challenge risk assets, particularly in emerging markets.

In the US, we think the Fed might have to hike more than four times – which is current market pricing – to tame inflation. In Europe, the market is pricing nearly 20bp of hikes this year and nearly 30bp next year. We believe the ECB will try to delay their first hike to next year but might have to accelerate hike at least twice in 2023. In the UK, the market is pricing over 100bp in hikes, with the next hike in February. With real rates the most negative in developed markets, 100bp of hikes would be less than half what’s needed. That said, with overleveraged consumers and a weak growth outlook, coupled with supply bottlenecks due to Brexit, we believe policy normalisation will be difficult in the UK.

Higher real rates will hurt asset prices globally. We see three scenarios playing out:

Worst case: weak China growth and persistent supply bottlenecks in DM. Chinese authorities tightened policy aggressively last year, targeting both listed firms and the property sector. Absent further stimulus, China’s economy might hover near 4% growth. If supply bottlenecks and lockdowns persist – not our base case – then central banks might be forced to hike more against slowing global growth. Risk assets should behave like in 2018 in this case with persistent spread widening, while yield curves will flatten further.

Best case: China stimulates further, economic bottlenecks ease. In this scenario, the Fed might stop at 4-5 hikes, while China stimulus will maintain growth closer to five percent. We still see headwinds for risk assets, albeit more due to rotation from growth to value.

Middle case: bottlenecks ease but China growth slows: In this scenario, EM risk assets will underperform further both in hard and local currency. DM rates will continue to widen. This widening combined with weakening China growth may start to weigh on DM risk asset prices.

The balance of risks points to more volatility and more downside in emerging markets, on tight valuations, slowing China growth and rising geopolitical risks in Eastern Europe and South East Asia.

4. Will global fiscal stimulus fade in 2022?

Global fiscal stimulus will decline this year remains above pre-pandemic levels.

In the US, while progress on new fiscal stimulus has stalled, the US is unlikely to return to a balanced budget any time soon. Historically, large US deficits take between 4 – 7 years to close, implying at least another 2 years of spending above 2019 levels. We could also see fiscal stimulus re-accelerating to near 2020/2021 levels – but only in the unlikely scenario where Democrats retain both the House and the Senate, as we discuss in the point below.

In Europe, Covid fiscal stimulus lagged its DM peers: European fiscal deficit was -7% GDP in 2020 vs -14% GDP in the US and UK. This may imply that Europe will be slower than its peers to close its fiscal gap. In fact, of the EUR 750bn EU Next Generation Fund, only 13% has been spent in 2021 with the remainder to be spent over 2022-2023.

Outside DMs, the key question is if Chinese leaders will stimulate their economy in 2022 and how large the stimulus might be if they do. Thus far, the CCP and the PBOC have maintained their stance for only targeted stimulus and downplayed the need for larger, broader stimulus.

4. Will global fiscal stimulus fade in 2022?

Global fiscal stimulus will decline this year remains above pre-pandemic levels.

In the US, while progress on new fiscal stimulus has stalled, the US is unlikely to return to a balanced budget any time soon. Historically, large US deficits take between 4 – 7 years to close, implying at least another 2 years of spending above 2019 levels. We could also see fiscal stimulus re-accelerating to near 2020/2021 levels – but only in the unlikely scenario where Democrats retain both the House and the Senate, as we discuss in the point below.

In Europe, Covid fiscal stimulus lagged its DM peers: European fiscal deficit was -7% GDP in 2020 vs -14% GDP in the US and UK. This may imply that Europe will be slower than its peers to close its fiscal gap. In fact, of the EUR 750bn EU Next Generation Fund, only 13% has been spent in 2021 with the remainder to be spent over 2022-2023. Outside DMs, the key question is if Chinese leaders will stimulate their economy in 2022 and how large the stimulus might be if they do. Thus far, the CCP and the PBOC have maintained their stance for only targeted stimulus and downplayed the need for larger, broader stimulus.

5. What are the potential implications of US midterms in the Fall?

We think investors should prepare for a further contraction in fiscal stimulus next year in the likely scenario where Democrats lose the House of Representatives.

In all but two instances of mid-term elections since WW2, the ruling party has lost seats in the House. With President Biden’s approval rating at new lows, it is likely that the Democrats will lose the House. It’s unclear if they will also lose control of the Senate.

Therefore, our base case scenario is that Republicans win at least the House majority and could also win the Senate majority. In this scenario, we expect a political stalemate and for discussions on fresh fiscal stimulus to stall. Some political commentators have suggested that if the Republicans control both the House and the Senate, they could approve some fiscal stimulus like cutting corporate taxes. We think this is unlikely as the Republicans are incentivised to not co-operate with President Biden and increase their odds of winning the 2024 elections.

In the unlikely scenario that the Democrats retain majority in both the House and the Senate, we could see a push for fresh fiscal stimulus – potentially the infrastructure deal could be revived. The odds of this passing, however, ultimately depend on whether inflation at the time has declined substantially from the current unpopular level of 7% YoY. If this hasn’t happened, the odds of fresh fiscal stimulus are lower.

6. What is the likely direction of political change in Italy and France and how will it affect European stability? When will debt worries be back in the Eurozone?

We believe European politics are likely to remain stable despite key elections in France and Italy. Debt sustainability concerns are likely to return in 2023, however, on higher policy rates.

In France, Presidential elections will take place in April. Macron is leading in polls, as his approval rate turned stronger during the Covid crisis. The populist front, very strong in 2017, is now faring worse, as Covid fiscal stimulus reduced the appeal of anti-European positions, and immigration is less of a key theme post-pandemic. In fact, Marine Le Pen’s polls are close to Republican Pécresse, suggesting a run-off may see a moderate win in any case.

In Italy, the Presidential election in late January will determine the future of the government. An election of current PM Draghi would open up a small risk of early elections, though MPs’ appetite for an additional year of tenure may push for another semi-technical government until 2023. The best case for markets would be a re-election of the incumbent President Mattarella, which would pave the way for Draghi to become President after his term as PM ends in 2023. A third candidate election would be a short-term positive as election risk would be removed, but would increase uncertainties for 2023. The risk of instability is therefore low, though some uncertainties may arise with Italian elections in 2023.

Eurozone debt worries are also likely to be postponed to 2023. The ECB tapering will be more gentle than the Fed one, and hikes are not on the table for now. With inflation above market yields for longer, sustainability issues are likely to arise later on, especially if 2022 continues to see moderates prevailing in the periphery. Market risks, though, are skewed to the downside. Central banks now hold a large fraction of European debt – 35% just in Italy, so that tapering will mean lack of support for the key stakeholder of European debt.

Periphery spreads remain at historical tights in face of increasing political uncertainty and reduced central bank support. Risk-reward on periphery government debt is thus strongly skewed on the downside.

7. What is the outlook for China growth in 2022 and will authorities increase stimulus?

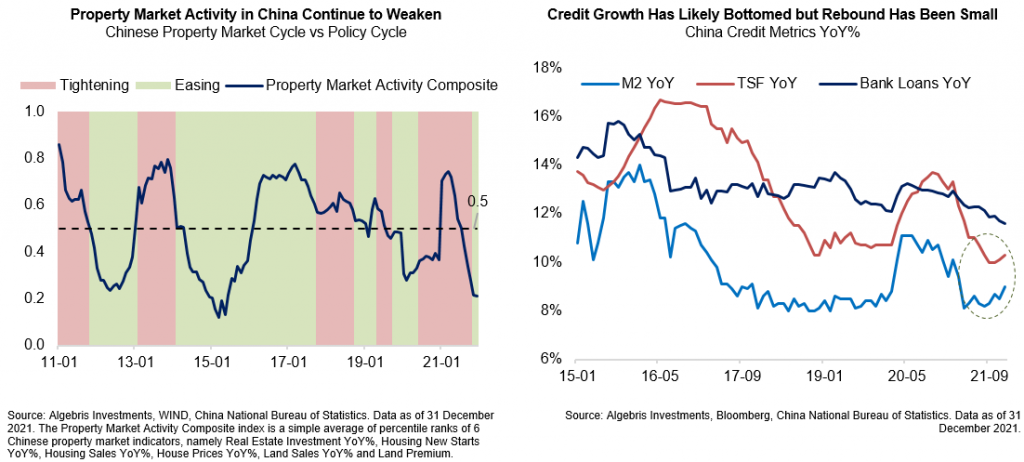

We see China growth slowing towards four percent in 2022. China growth will be challenged by a number of headwinds in 2022, namely its strict adherence to an increasingly costly zero-Covid strategy, depressed property market activity, poor policy coordination between the central government and various tiers of local governments/institutions, as well as difficulties in balancing long-term social-economic goals and short-term stability.

China’s zero-Covid policy characterised by compulsory quarantine for all international travellers, mass testing and contact tracing, as well as swift and targeted lockdowns had worked well in the early part of the pandemic. However, the highly infectious Omicron variant means the cost of sustaining such a strategy has become disproportionately high. Yet the government has shown little sign in relaxing the policy: the Chinese Civil Aviation Authority in its recent published five-year plan targeted 2023-2025 for restoring international travel, indicating likely continued border closure in 2022. More sporadic outbreaks and regional lockdowns mean greater economic disruptions when growth is already weakened by a troubled property sector. As shown below, our composite index indicates that property market activity are near historical lows as house sales slow and liquidity-strapped developers focus on surviving instead of starting new projects.

These growth challenges call for more policy easing. Indeed, the central government switched to a more dovish tone in Q4, with the December Central Economic Work Conference releasing a strong pro-growth message. However so far, all the easing measures have remained small and targeted, including a 50bp cut to banks’ reserve requirement ratio, 5-15bp cuts to various policy rates, and relaxations of house purchase restrictions/mortgage rules in some cities. On the one hand, China’s long-term goals of reducing structural imbalances and pursuing “common prosperity” makes it cautious in adopting any broad-based stimulus that could be seen as “opening the flood gate”. On the other hand, targeted and region-level measures may be prone to poor executions, especially for local governments with weak finances.

The Chinese government is likely to step up policy stimulus in coming months to maintain growth stability for the upcoming Party Congress in the fall. However, the risk is that such stimulus may not be large or timely enough to fully offset all the economic headwinds such that growth undershoots market expectations. This could hurt China-exposed countries and sectors through sentiment and trade links. In addition, continued zero-Covid strategy and frequent regional lockdowns in China mean persistent disruptions to global supply chains and slower easing of inflationary pressure for developed countries.

8. Will geopolitical tensions in Ukraine and Eastern Europe erupt into war?

Risks of further escalation have increased in the past weeks. We see 50% chances of a local conflict in Eastern Ukraine by year end, despite diplomacy still being open.

Starting in late November, Russia amassed a large number of troops at the border with Ukraine, reminding markets of previous episodes in Georgia (2008) and Crimea (2014). The escalation is a bid from the Kremlin to re-establish a clear Russian influence sphere in Eastern Europe. In fact, in late December, Russia demanded the United States to publicly subscribe a roadmap for European security, requiring hard-to-accept restrictions on NATO membership and action in Eastern Europe. The escalation was conducted in conjunction with all-time highs in gas prices, so to limit the scope for reaction from Europe.

The standoff between the US and Russia intensified in early January, when both parties held strong on their position at the NATO-Russia talks in Geneva. The unsuccessful outcome of the talks sparked a strong market selloff. Ukraine bonds reached three-year lows and now pay 10% USD yield. The Russian Ruble and local bonds have been aggressively sold on fears of economic sanctions. The broader emerging market segment started selling off aggressively in the days following the break in talks. Markets are now pricing high chances of military action.

The best case: de-escalation of tensions. For that, we would need some concessions from the US, and Russia to be included at least in the discussion for European security. A de-escalation will not happen immediately given the current state of tensions, but will take place over a few weeks via various rounds of discussions. In this case, no economic disruption would be imposed on Ukraine. At the same time, Western governments have no need to impose a new round of sanctions on Russia. In such a scenario, asset prices would recover most but not all losses since December, as some risk premia may remain in the market. We assign a 40% chance to this scenario.

The worst case: full invasion. In this scenario, the Russian army invades Ukraine and marches towards Kyiv. The final outcome of such a case is uncertain, but it would certainly cause major economic disruptions within Ukraine, causing a massive increase in credit risk. US and Europe would respond aggressively, imposing sanctions on Russian debt and cutting the country out of the swift system. In this case, Ukraine would suffer a major economic disruption. Stronger fundamentals suggest the downturn may not be as deep as in 2014, but a contraction in the order of 5-10% is plausible. In this case, Western financial support would continue to be plenty, but it would not avoid material credit risk for the bonds. In this scenario, US and Europe would strongly react against Russia, with new sanctions on sovereign debt and a likely cut-out of Russia from the swift system. Russia’s economic performance is unlikely to be materially hit in this scenario, but bond markets and the currency would face steep losses. We assign a 10% chance to this scenario.

The middle ground: local conflict. case is more aggressive actions that fall short of a proper war. We find this the most likely outcome, with 50% probability. Aggressive actions could include an occupation of selected areas of Eastern Ukraine, or air strikes across the region. In this case, Ukraine credit risk would increase only moderately as mild economic disruption would be offset by the strong financial buffers the country has built over the past three years. Moreover, Western financial support would stay strong. US would hit Russia with some sort of sanctions, but a swift cut-out in this scenario is ultimately unlikely, as European cooperation would not be warranted. Some extra restrictions on bond markets and individual sanctions are most likely in this case. Volatility in Russia and Ukraine assets would thus increase but permanent losses are less likely.

9. Will Turkey’s new monetary policy work or will it burst into a major crisis?

We believe recent policies will not work to address Turkey’s fundamental vulnerabilities. In fact, structural fragilities make Turkey one of the countries most exposed to the Fed tightening cycle this year.

Starting in September 2021, Turkey’s CBRT pursued an aggressive policy of monetary easing, with 500bp in cuts up to December. The cuts came despite inflation above 20% and global monetary tightening. As a result, the Turkish lira slumped, depreciating more than 50% in 2H21. A weak lira and high inflation triggered a confidence crisis from domestic savers, with dollarization reaching all-time highs in November. In late December, the government thus decided to introduce a new scheme aimed at discouraging dollarization. Under the scheme, the government pays back any FX losses depositors incur by holding domestic currency deposits, de facto guaranteeing 14% lira returns to savers using public funds.

The scheme has some appeal, as Turks have more than $200bn in dollar deposits and government debt is low at 40% of GDP. In fact, the Turkish lira stemmed some of its losses since the deposit was introduced and found some stability in early 2022. Still, we don’t see it as a long-term fix: guaranteed rates are well below inflation, which is likely to rise to 50% later this year. As such, the rate is unlikely to incentivize much conversion from dollar deposits. Moreover, the currency slump triggered strong intervention from the central bank late last year, which resulted in a much lower reserve buffer. Turkey’s reserves net of resources owned to local banks via currency swaps are now below $10bn, worryingly low for a $700bn economy.

We believe dovish monetary policy, thin buffers, rampant inflation and unorthodox measures will prove a bad mix for Turkish assets in 2022. Stimulative policy is also likely to get more aggressive as 2023 elections get closer. Turkish assets are thus likely to continue to suffer: the currency will gradually depreciate in line with inflation, and credit will remain under pressure as FX depreciation hurts the country’s buffers and banks’ balance sheets, especially in an environment of higher US rates and USD strength. Both local and global conditions point to Turkey as one of the main potential market casualties of 2022.

10. Will elections in Brazil destabilize Latin America’s politics?

We think it is possible, as this is the key event in the region for 2022 and the outcome is very open.

Brazilian general elections will be held in October. Both the President’s job and all seats in Congress are up for grabs. The election is particularly uncertain as former leftist President Lula announced his candidacy. Lula’s tenure was characterized by heavy non-market policies, such as aggressive fiscal policy and a wave of SOE nationalizations and mismanagements. For now, the stance and staff of Lula into the upcoming campaign is unknown. Some analysts see him taking a more moderate stance given the extreme positions of current President Bolsonaro on many topics. On the other side, even a somewhat more populist Lula may have a chance given Bolsonaro’s poor track record during the pandemic. Polls currently see Lula’s approval at 40% vs Bolsonaro’s 25%, with moderate candidate Moro in the single digits. Recent developments suggest Lula may be picking a moderate VP, in an attempt to conquer the centre. This would ultimately moderate tail risks from his election. The political arena thus remains quite open, and the campaign starting in April may bring volatility.

Brazilian assets have fared poorly in 2021 and some macro risks are fading, namely the breach of the spending cap was avoided and inflation is starting to fall. The Brazilian real is at 5y lows in real terms, and long-end yields have widened 400bp in 2021, ending the year 200bp above inflation. As such, markets have started pricing in a notable negative scenario, which might not materialize ultimately, especially if Lula plays the moderate game.

Shorter term, election uncertainty can still create some volatility, especially in currency and credit, should Lula run with a lefty platform. Post pandemic, the political balance in Latin America has gradually shifted to the left, with turns in Peru and Chile last year, and possibly in Colombia this year. Argentina and Mexico have already turned nationalist in the past three years. A turnaround in Brazil would thus mark a final step for less market friendly government in the region, with negative implications for the region’s economic outlook and stability.

Conclusions: How do we think about bond investing?

Monetary policy normalisation has key portfolio implications. First, a rotation from low volatility, high multiple assets into ones which can withstand higher rates or higher prices, like financials and commodity producers. Second, a potential regime shift in bond-equity correlations, due to persistent inflation volatility. This might favour barbell portfolios, for example, over the typical balanced portfolio or its leveraged version, risk-parity. Third, after many years of subdued volatility, policy normalisation might spark a rise in tail risk in both rates and equities.

In this context of policy normalisation and higher interest rates it is fair to ask the question: why should you invest in bonds at all? The answer is investors need to re-think fixed income strategy, as veteran bond investor Dan Fuss argued recently.

One reason is we are not out of secular stagnation. Fixing decades of underinvestment in infrastructure, education and high inequality might take more than one infrastructure plan. Today’s macro narrative is all focused on strong demand and rising inflation – but policy tightening might eventually mean risks for growth. At wider valuations, income assets should still be part of your portfolio.

Another reason is that with today’s compressed valuations, active managers can find very inexpensive protection against idiosyncratic tail events in bonds and credit. Some examples of potential tail risk come to mind: in Turkey, where the Erdogan administration is struggling with inflation rates of over thirty percent, the government has expanded FX swap loans and is using state banks to sustain the Lira, while at the same time keeping interest rates at less than half the inflation rate to support demand until elections. MicroStrategy, a business intelligence and software services companies with around $500mn in revenue and below $100mn profits, issued over $2.5bn of debt to acquire bitcoin.

As in previous situations characterised by low volatility and compressed valuations, we have de-grossed our strategies and added protection in capital structures which we deem unsustainable.

The next months won’t be an easy ride, but higher volatility and dispersion will surely provide opportunities.

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2022 Algebris Investments. Algebris Investments is the trading name for the Algebris Group.