Inflation: What investors need to know

The US just printed a 7% y-o-y increase in inflation. Europe is hardly lagging though, with German inflation rising to 5.7% in December and overall Euro area inflation at 5%. What do investors really need to understand to ensure their portfolios are well protected?

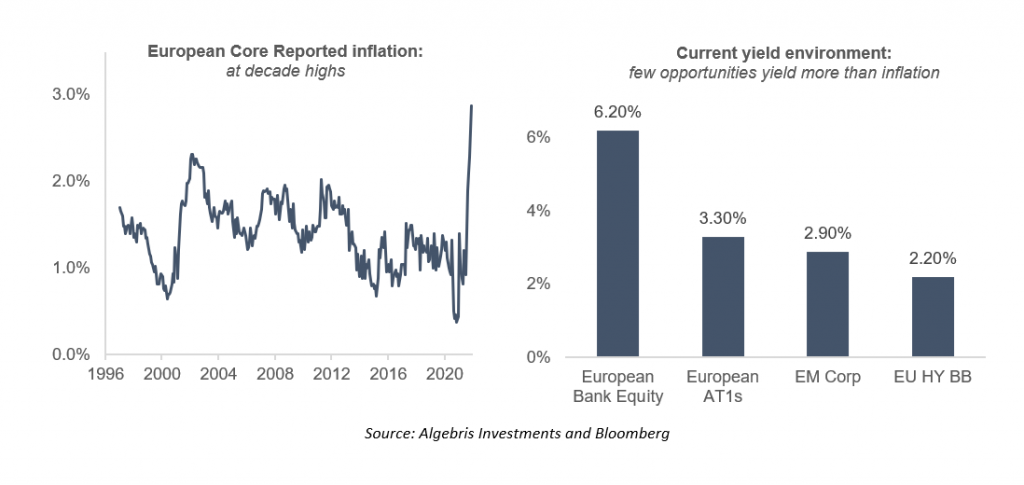

- Inflation is already extremely high

- Interest rates of -50bps in the Euro area are not consistent with 5% inflation, GDP/unemployment close to pre-Covid levels, a recovering economy/pandemic and close to maximum fiscal and monetary support

- Yes, inflation is peaking but the question investors should be seeking an answer to is: ‘What is the likely inflation level in the coming year or two and specifically, is it likely to be much lower than 2%?’ Inflation impacts market yields and interest rates which have a direct impact on bond portfolios and equity valuations

So, is there anything we can sensibly say about inflation in the coming year? There is a reasonable expectation that goods inflation, which is pushing up current inflation, will abate as demand rebalances towards services and supply chains respond. That is the good news. European inflation is coming down from 5%. However, companies are likely to pass on at least some of their current higher input costs to consumers, households have seen their real wages sink this year and higher energy costs are likely to galvanize their desire for higher wages in 2022/2023. What this means is inflation, though falling from its highs, may well be stickier and higher than the optimists hope for, especially as inflation expectations are picking up.

The US Fed is beginning tapering and the market now expects four interest rate increases this year. With the German 10 Year government bond yielding 0%, yields are likely to trend higher. With the ECB almost certainly under pressure to bring policy rates back from -0.5% to 0% and inflation expectation rising, bond holders are likely to continue to see volatility and relatively sparse returns.

Where can bond holders access reasonable returns? One area of the bond market that has top decile yields and half the duration of the overall bond market (thereby reducing any likely volatility) is financial sub-ordinated bonds. As central banks have not included these bonds in their huge QE programs, yield has been left on the table for investors.

The equity market is slightly better poised for higher yields, though the longest duration equities are beginning to experience more volatility and poorer performance eg some tech companies. The financial equity sector is one of the few sectors that benefits from higher yields. The European bank sector has 40% upside to where it was as recently as 2018, as it recovers from the Covid-19 recession.

This document is issued by Algebris (UK) Limited. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris (UK) Limited.

Algebris (UK) Limited is authorised and Regulated in the UK by the Financial Conduct Authority. The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Under no circumstances should any part of this document be construed as an offering or solicitation of any offer of any fund managed by Algebris (UK) Limited. Any investment in the products referred to in this document should only be made on the basis of the relevant prospectus. This information does not constitute Investment Research, nor a Research Recommendation. Algebris (UK) Limited is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris (UK) Limited , its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is for private circulation to professional investors only.

© 2022 Algebris (UK) Limited. All Rights Reserved. 4th Floor, 1 St James’s Market, SW1Y 4AH.