The rapid growth of computing demand, driven especially by AI workloads, is making data centers one of the fastest-growing sources of electricity consumption globally. AI training, new software solutions, and large-scale data storage require significantly more power than traditional enterprise IT, pushing infrastructure to its limits. As capacity scales, so does resource use.

By 2035, data centers are expected to require more than 360 gigawatts of additional power generation globally. At the same time, U.S. hyperscalers (being the large companies operating in the cloud computing and software space) are expected to commit over $1.8 trillion in capital expenditure by 2030 to secure power supply, expand capacity, and upgrade operational systems. Asian hyperscalers are working on a similar trajectory.

Two critical constraints are emerging across this buildout: power availability and water-intensive cooling. Energy infrastructure projects frequently face long lead times, with their interconnection to the main grids often taking years. Meanwhile, large datacenters can consume large amounts of water per day, raising environmental and regulatory concerns, particularly in water-scarce regions.

In response, operators are treating efficiency as the new capacity. Solutions such as renewable energy, liquid cooling, waste heat recovery, and digital industrial management are gaining ground, not just to reduce footprint but to unlock additional workload capacity. These shifts are redefining business models, and this is where value accrues. Beneficiaries may be companies related to the power and grid sector, together with technology and industrial solution providers that are well positioned for the next phase of digital growth.

More Compute, More Consumption

In 2024, datacenters had an estimated power capacity of 81 gigawatts and consumed around 371 terawatt-hours of electricity, roughly 1.4% of global final demand. It has been steadily growing since 2010, as more individuals become connected to the internet or have access to technology (IEA, 2024).

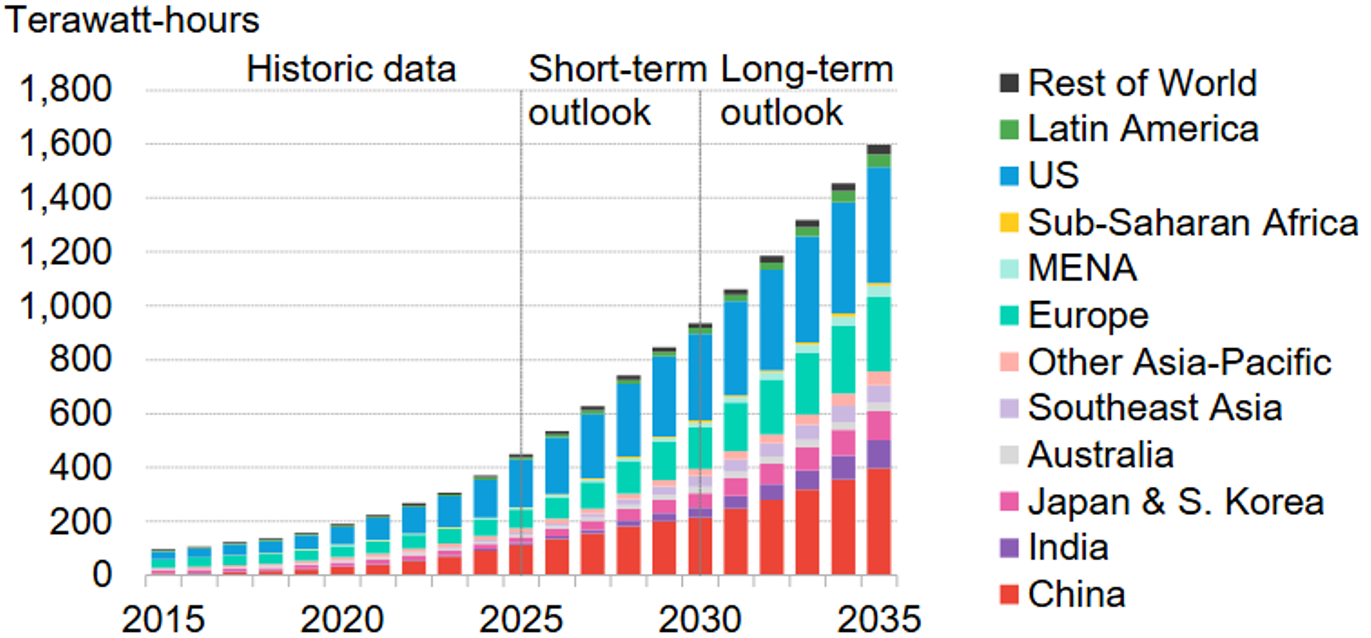

Source: BNEF. Data as at 15/04/2025

Yet, the proliferation of computational workloads in both businesses and daily life is spurring unprecedented data center expansion – and with it, soaring energy consumption.

Bloomberg NEF (BNEF) expects their capacity to more than triple over the coming decade, reaching 179GW by 2030 and 277GW by 2035. As a result, electricity consumption will scale dramatically, increasing 2.5x to 935TWh by the end of the decade (2030) and potentially hitting 1,600TWh by 2035 (see figure 1, BNEF, 2025).

This surge means datacenters alone could account for 3% of total global electricity demand by 2030 and 4.5% by 2035. Looking further ahead, if current trends continue, datacenters could be responsible for as much as 8.7% of global power use by mid-century, highlighting the urgent need to align digital infrastructure growth with sustainable energy strategies (BNEF, 2025).

To support this surge, industry capital spending is set to grow significantly. BCG estimates U.S. hyperscalers alone will invest $1.8 trillion in data-center CapEX from 2024–2030 in everything from compute to supporting corollaries such as power generation and grid.

Outside the U.S., Asia is rapidly emerging as a second major engine of data center growth. In China, the 6 largest internet and cloud providers are expected to boost annual CapEX by nearly 60% over the next three years, exceeding RMB 373 billion (about US$50 billion). This investment is projected to drive 3-4 GW of new data center capacity per year, equating to a 20% CAGR. Elsewhere in the region, Malaysia is leading Southeast Asia’s buildout, with utility Tenaga managing a 6 GW data center pipeline, roughly two-thirds of total planned regional capacity.

A major reason energy use is scaling so steeply is that today’s computing activities are far more power-hungry than traditional IT. AI workloads, such as training large models and running inference on GPUs, roughly account for 20% of energy demand, and that share can grow (The Guardian, 2025). For example, processing a single ChatGPT query consumes nearly 10 times as much electricity as a typical Google search. Yet, the other 80% derives from the drastic rise of online users, driving massive growth in cloud computing and data storage, further amplifying the overall energy burden.

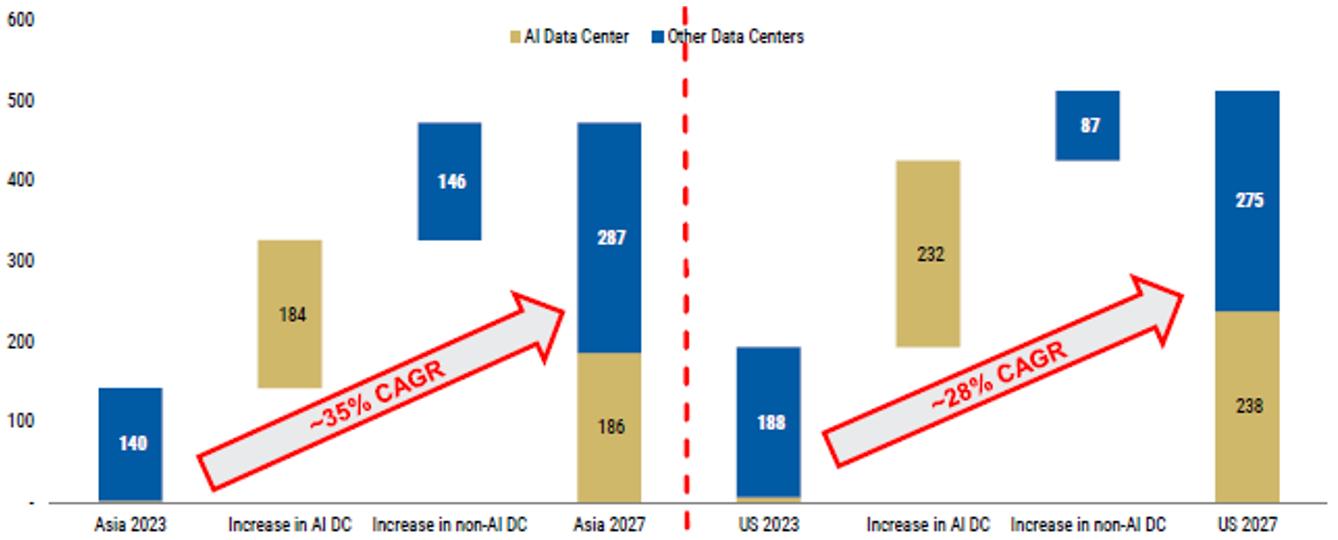

Source: Morgan Stanley, Algebris Investments. Data as at 26/05/2025

With the higher processing workloads likely to increase, density of power supplied by datacenters is also likely to grow out of necessity. Morgan Stanley estimates this increase to be from 188 TWh to 513 TWh in US and similar in Asia, though Asia’s growth rate is likely higher than the U.S.’ (35% CAGR versus 28% CAGR respectively for Asia and U.S., see figure 2).

With such a steep scale up curve, large tech companies are now running up against physical resource limits: securing enough power, grid capacity, land, and cooling (water). We will be tackling the following two in this publication.

- Power availability is frequently the hardest constraint. New energy projects are challenging and can take years to per approved. Where capacity is available, permitting new high-voltage lines or substations for transmission and distribution can take years.

- Water and cooling resources are another concern. Many large facilities rely on evaporative cooling, often consuming significant amounts of water (the average data center can use about 1.8 liters of water for every kWh of energy it consumes), raising sustainability concerns, among others.

Gigawatts for Gigabytes

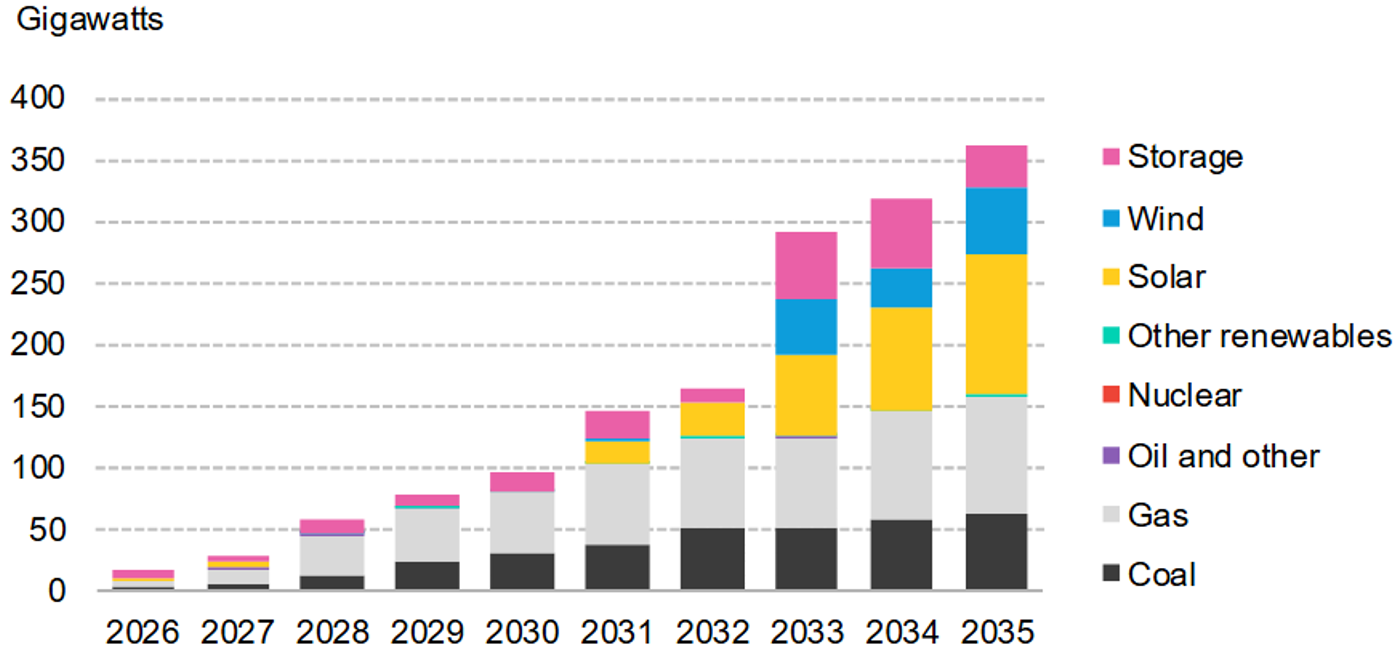

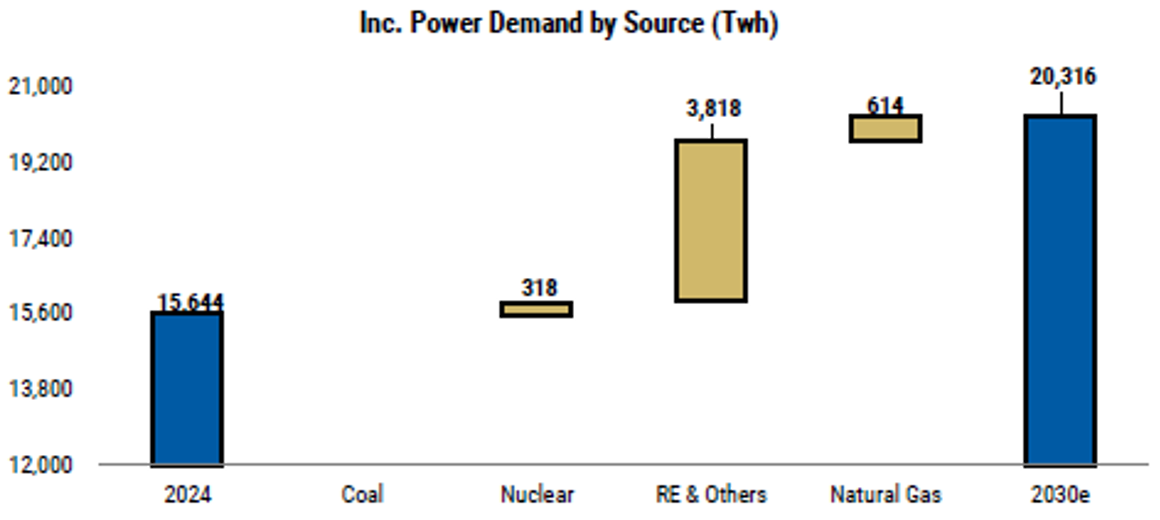

NEF estimates that if data centers were treated as a single country, they would rank as the fourth-largest electricity consumer globally – behind only the US, China, and India. To meet this escalating demand, an additional 362 GW of global power generation will be needed by 2035, the equivalent of constructing 350 large-scale power plants, according to BNEF estimates (see figure 3).

Source: BNEF. Data as at 15/04/2025

To meet this demand, significant energy infrastructure development is crucial from both power availability and transmission and distribution perspectives.

Leading U.S. hyperscalers (i.e. Amazon, Microsoft, Google, Meta) are the major drivers of this energy infrastructure growth, as they enter both short-term and long-term contracts with utilities that have both renewable and fossil fuel capacity, as well as renewable energy developers and grid operators. Though gas has been the energy source of choice in the short term for 24/7 power availability – bridging cost, emissions, and immediate deployment – a clean energy mix will likely be the outcome, bringing costs even further down while facilitating their decarbonization and meeting their net zero commitments.

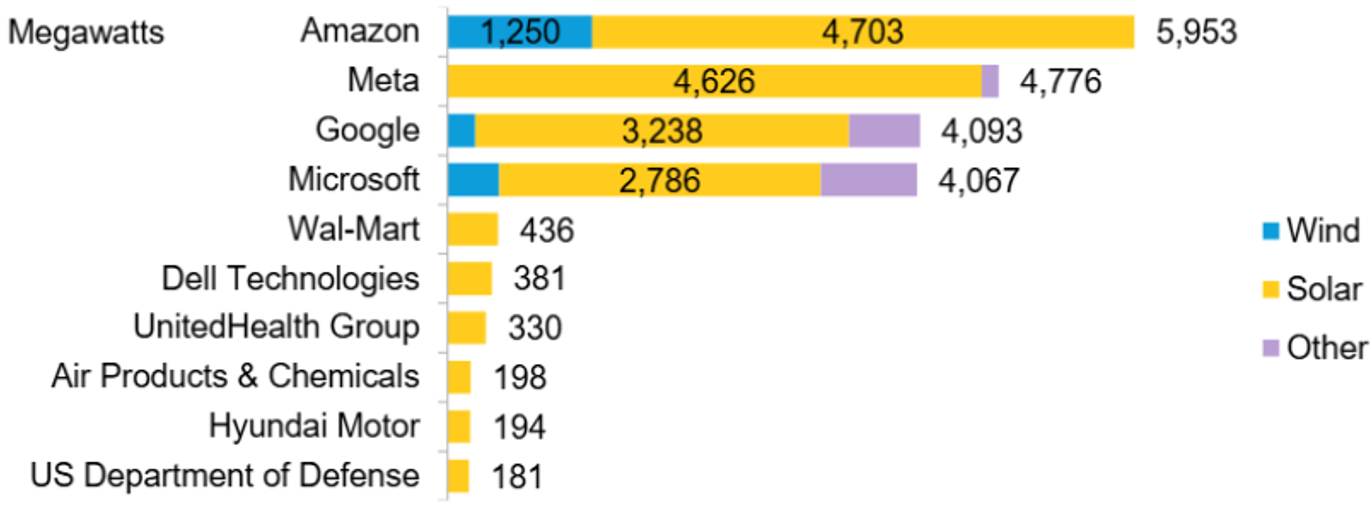

Today, an S&P analysis finds that U.S. hyperscalers together have c84 GW of clean energy in their procurement pipeline. They contracted over 50 GW of renewable capacity to supply their facilities, with solar and wind dominating these contracts (about 29 GW and 13 GW respectively in the U.S.) (see figure 4).

Source: BNEF. Data as at 15/04/2025

In Asia-Pacific, large cloud and technology companies are also working to meet growing power demand, expected around c4.7% CAGR through 2030 (led by China and India, with Southeast Asia following closely, c4.3% annually ex-China). This expanding demand is reshaping the regional energy mix thanks to investments from hyperscalers: renewables and natural gas are gaining share, while coal use remains largely flat (though it is expected to decrease).

There is upside in renewables, supported by aggressive capacity buildout and steady efficiency gains, creating a clear runway for investment across generation, grid, and enabling technologies.

These long-term contracts from big tech firms provide a reliable offtake, allowing wind, solar, and gas projects to secure financing, which is not a certainty in the renewables space. In markets like the EU and US, datacenters and tech firms have led a rise in corporate PPAs, complementing government auctions for renewable energy. In Asia, similar efforts are creating a parallel investment cycle across the region, positioning regional utilities, renewable developers, and grid enablers as key beneficiaries of hyperscale growth.

As this trend grows, datacenters will increasingly procure clean energy supporting a positive feedback loop. This loop not only creates significant upside potential for utilities and renewable developers, but also for the companies facilitating the deployment of this clean energy.

Enablers of interconnected grids such as Prysmian or Nexans will help fill gaps in renewable power and will likely benefit from hyperscaler investment. With high grid exposure through the Power Grids and Transmission businesses, those segments have a projected compounded average revenue growth of c8% and c9% respectively to 2030.

Source: Morgan Stanley. Data as at 26/05/2025

Efficiency is the New Capacity

With power and cooling emerging as gating factors, data center operators are treating energy efficiency as effectively the new capacity. Every watt of savings in overhead or cooling is a watt free for additional computing workload. Beyond immediate capacity gains, improved efficiency enables companies to reduce their long-term environmental impact and supports them in meeting their climate commitments.

As traditional air-cooling struggles with rising chip densities, leading to inefficient hotspots or maldistributed cooling, the industry is increasingly turning to liquid cooling. Surveys show only ~17% of data centers have adopted liquid cooling so far, but an additional 32% plan to deploy it in the next 1–2 years, indicating a potential wave of adoption ahead (AFCOM, 2024).

On the one hand, companies such as Vertiv, Asetek, and Schneider Electric arerolling out liquid-cooled rack designs in partnership with chipmakers to support up to 100+kW per rack efficiently. On the other, companies such as ABB and Trane Technologies are incorporating real efficiency gains in datacenter operations through highly efficient power architectures and autonomous control systems.

These solutions not only cut cooling power use (one liquid cooling module showed 15% total power savings in AI clusters during tests) but may also enable water heat recovery and reuse in other parts of the facility or the community therearound.

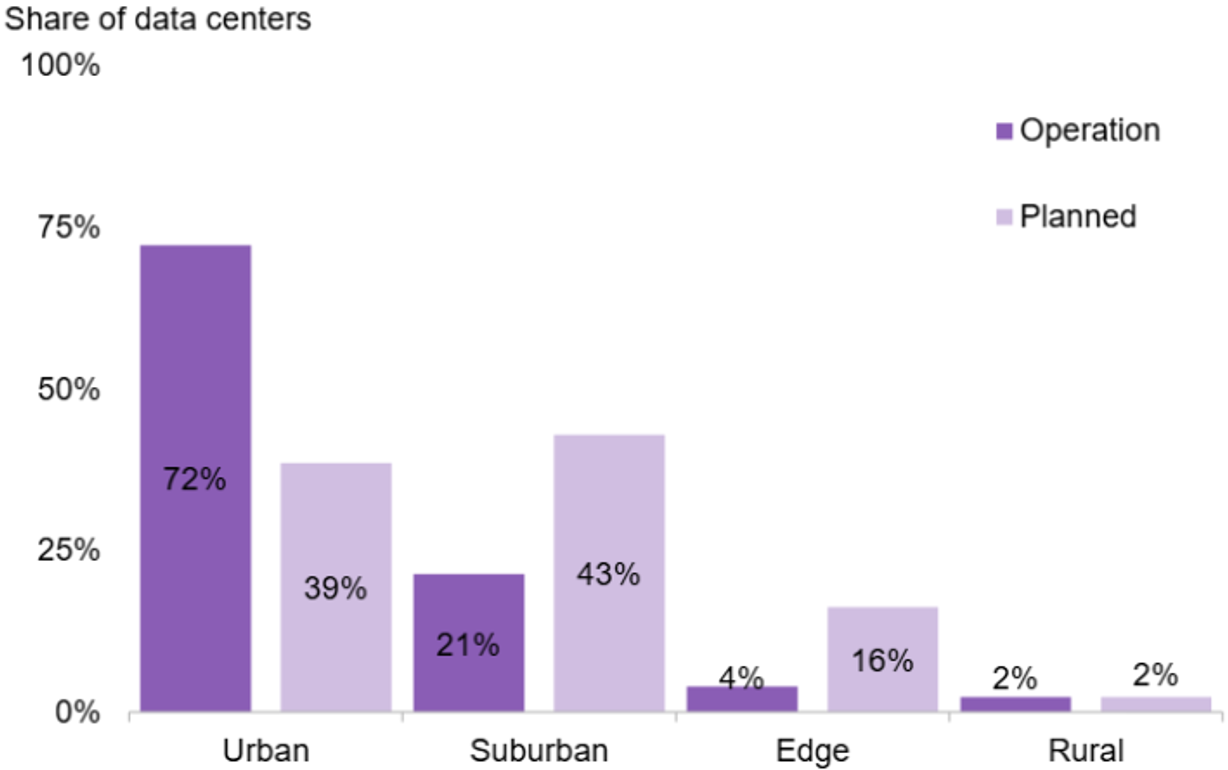

Indeed, as nearly 100% of the electricity entering a data center turns into heat there is a huge opportunity to reuse that energy (Vertiv, 2025). This is already in place in Denmark, where Meta’s Odense data center recovers waste heat to supply thousands of households via the city’s district heating system. With most datacenters planned near urban areas, this is a viable possibility for the efficient reuse of power and energy; see figure 6 (BNEF, 2025).

Source: BNEF. Data as at 15/04/2025

Beyond hardware, smarter operations can turn efficiency into capacity. Many operators are now layering digital twins to simulate and optimize power usage, predicting hot spots or underutilized equipment and calibrating accordingly: adjusting cooling, airflow, server workloads. Chip manufacturers such as Nvidia are also working with these industrial solutions providers to expand efficiency capabilities. Examples of these twins are Schneider Electric’s EcoStruxure, ABB’s Ability or Siemens’ AVEVA, among others.

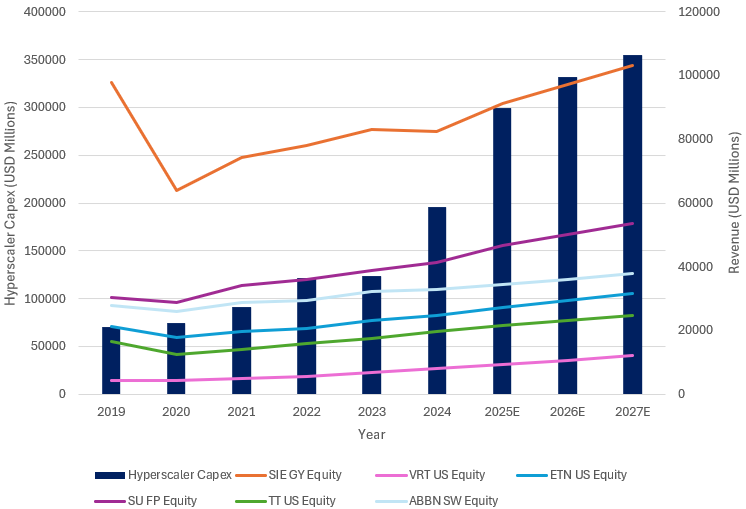

Over a large fleet of datacenters, these savings add up. Since efficiency initiatives often have strong financial paybacks – energy being one of the largest operating costs for data centers – long-term savings will likely incentivize large tech companies to invest in these upgrades sooner rather than later. In turn, this may benefit the revenue growth of the entire datacenter value chain (see figure 7, figure 8).

Source: Algebris Investments. Data: Bloomberg Finance L.P. Data as at 11/06/2025. Note: Hyperscalers Capex consider the capex of Meta Platforms Inc, Microsoft Corp, Oracle Corp, International Business Machines Corp, Alphabet Inc, Salesforce Inc, Amazon Web Services

Where digital growth meets real assets

In conclusion, increasing demand for compute from AI to data storage is not just a story of datacenters and microchips; it is equally a story of energy and infrastructure. In the 2025–2035 horizon, data centers face a new reality: energy usage and resource management are the primary limiting factors for scaling our computational abilities.

To address these constraints, capital could flow toward decarbonized compute, and value will increasingly accrue to those positioned to solve physical constraints: power, cooling, and connectivity. Clean energy pipelines paired with hardware manufacturers – from cables to cooling systems – are now central to unlock the next wave of hyperscale investment. Backing technologies that make scaling possible may offer not just returns, but resilience in an increasingly compute-dependent world.

Source: Quartr, 2025

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2025 Algebris Investments. Algebris Investments is the trading name for the Algebris Group

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.