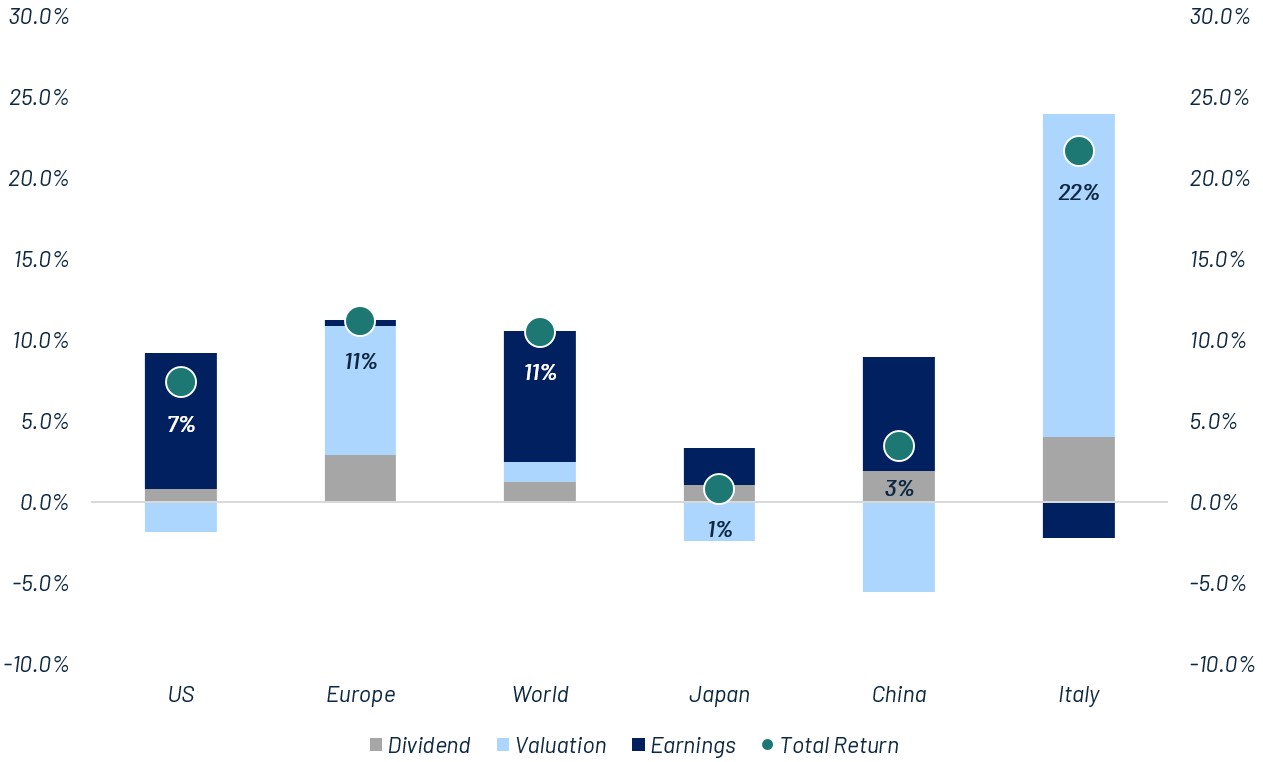

Currency Swings – The driver of Divergent S&P 500 returns

As of July 18, 2025, the S&P 500 recorded a year-to-date return of +7%, continuing its positive trend since Liberation Day. Strong earnings-per-share (EPS) growth largely offset valuation pressures, as multiples contracted due to heightened market uncertainty.

However, for European investors, the situation appeared markedly different. When measured in euros, the S&P 500 registered a negative year-to-date return of -4%. This divergence can be primarily attributed to the 11% depreciation of the U.S. dollar against the euro, underlining the significant influence that currency fluctuations exert on cross-border investment performance.

In contrast, Italy stood out with an impressive +22% total return during the same period. This outperformance was driven mainly by multiple expansion, reflecting a recovery from previously suppressed valuation levels, which had ranked among the lowest during the prior year.

Unlocking Italy – Quality, value, and global excellence in one market

Italy’s SMID champions stand out in the European landscape with a compelling mix of structural resilience and entrepreneurial drive. Italian SMEs contribute over half of the country’s exports—well above the European average—thanks to deep industrial specialisation and a strong high-tech manufacturing base. With more than 70% of these companies family-owned, long-term strategic vision translates into double the earnings growth expected versus the broader market (8% vs 4% CAGR 2024–26E). Despite trading at a discount (12x P/E vs 14x), they boast far healthier balance sheets, with net debt/EBITDA at just 0.8x. This unique combination of export-orientation, innovation, and financial discipline creates an underappreciated upside—making Italian SMIDs a high-conviction opportunity for equity investors seeking quality and value in one of Europe’s most dynamic segments.

Adding to this robust equity story is the strength of Italy’s banking sector—now among the most solid in Europe driven by well-capitalised financial institutions with healthy asset quality and profitability. This reinforces financial stability across the real economy and provides a supportive backdrop for corporate growth and equity performance.

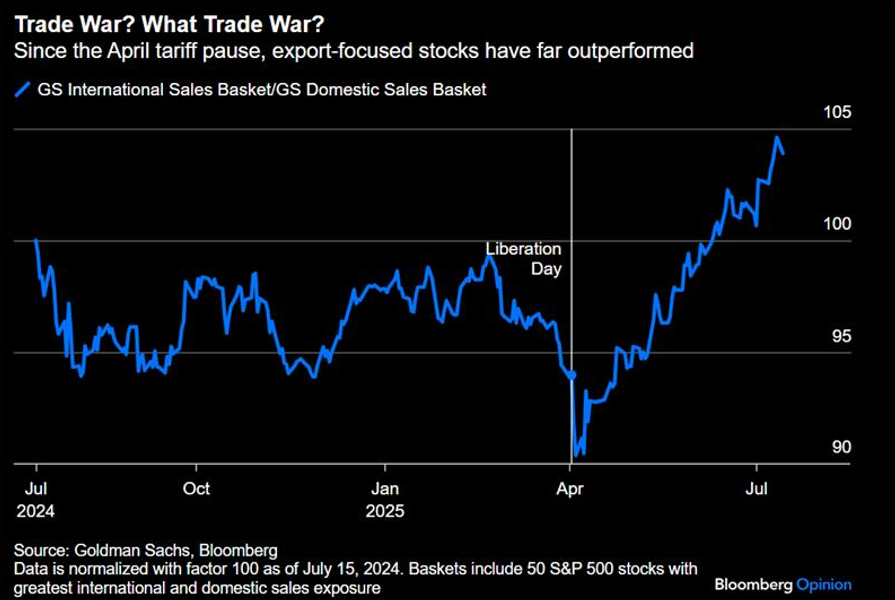

USA – Is Trump serious about tariffs?

Donald Trump came back to threaten the European Union with a 30% tariff on goods imported from the old continent. This should have been a negative surprise, as the general sentiment was for a more benign scenario. However, the reaction from equity markets so far has been quite muted.

Therefore, a question arises: is Trump serious about tariffs? After the Liberation Day shock, Trump revealed a more benign attitude, hinting that the real goal is negotiation. As shown in the chart, this idea has been widely accepted by the market so far, as US-listed stocks most exposed to exports have far outperformed domestic focused companies ever since Trump’s backtracking on tariffs in April.

Will the story repeat itself? It is very hard to predict, but the risk of a negative outcome out of this negotiation must not be underestimated. The sharp negative reaction of bond and equity markets after Liberation Day allows to believe that the US President might be induced to more “reasonable” terms. Moreover, the EU is offering counter-purchases, such as buying more US LNG or arms. But the Trump team wants market access. That involves altering European regulations, for example on food safety, and this will be much harder. Some sort of truce and a rate lower than 30% are achievable, but the issue won’t go away and will act as a lead weight on the European economy.

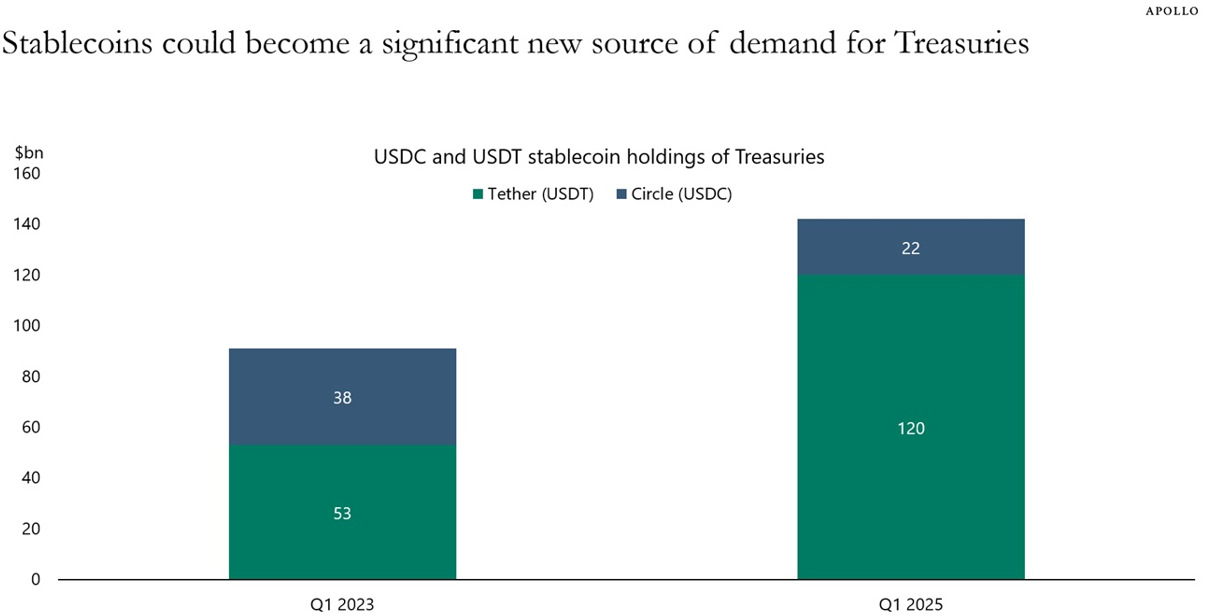

Dollar-Pegged, Debt-Fuelled – How stablecoins quietly shape US fiscal flexibility

Stablecoins are cryptocurrencies designed to maintain a stable value, typically pegged to the US dollar. To ensure this 1:1 peg, issuers such as Circle (USDC) and Tether (USDT) hold reserves largely made up of short-term U.S. Treasuries — low-risk, interest-bearing assets. These reserves are not only essential for stability, but also a key source of revenue: issuers earn interest on the assets backing their stablecoins. In 2024, for example, Circle generated $1.68 billion in revenue, 99% of which came from interest income. Circle, recently listed on public markets, is viewed as more transparent and U.S.-regulated, while Tether remains the dominant global player, with a more opaque structure but significantly larger market share. As of December 2024, Tether held approximately $113 billion in U.S. Treasuries, ranking it among the top global holders — reportedly the 7th largest, ahead of many countries. This dynamic makes stablecoin issuers a new and significant source of demand for U.S. debt. In a political context, it could help explain why a future Trump administration might tolerate higher interest rates or larger deficits — if crypto-based buyers continue absorbing Treasury supply.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.