Equities Pause despite solid earnings

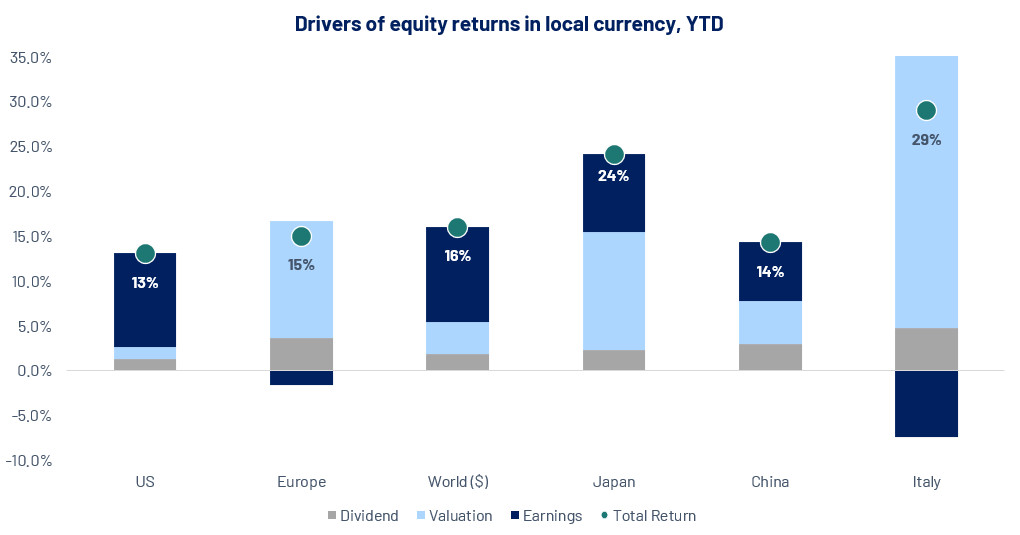

Global equities were overall muted over the past month, with a year-to-date backdrop remaining strong. Q3 results broadly confirmed resilient profit trends, and policy expectations stayed supportive, helping to limit downside risk. In the United States, markets were broadly steady. Earnings season was constructive, though expectations were elevated, while the late-October Federal Reserve cut and the conclusion of quantitative tightening provided a helpful policy tailwind. Equities also proved resilient through the federal shutdown, with investors largely looking past political noise amid solid, broad-based results. Sentiment improved further after a bipartisan funding deal was signed in mid-November, ending the shutdown and removing a key tail risk into the year-end. European equities also finished slightly lower, with a more uneven tone than the U.S. Investors worked through a heavy late-October reporting calendar against still-soft growth. Q3 earnings were mixed but started from low expectations, so modest beats were enough to cushion markets, especially in financials and defensives. The region continues to draw interest on relatively attractive valuations and less crowded positioning, with investors looking ahead to a cyclical recovery in 2026.

Source: Algebris Investments, Bloomberg Finance L.P, data as of 21/11/2025. Performances in local currencies.

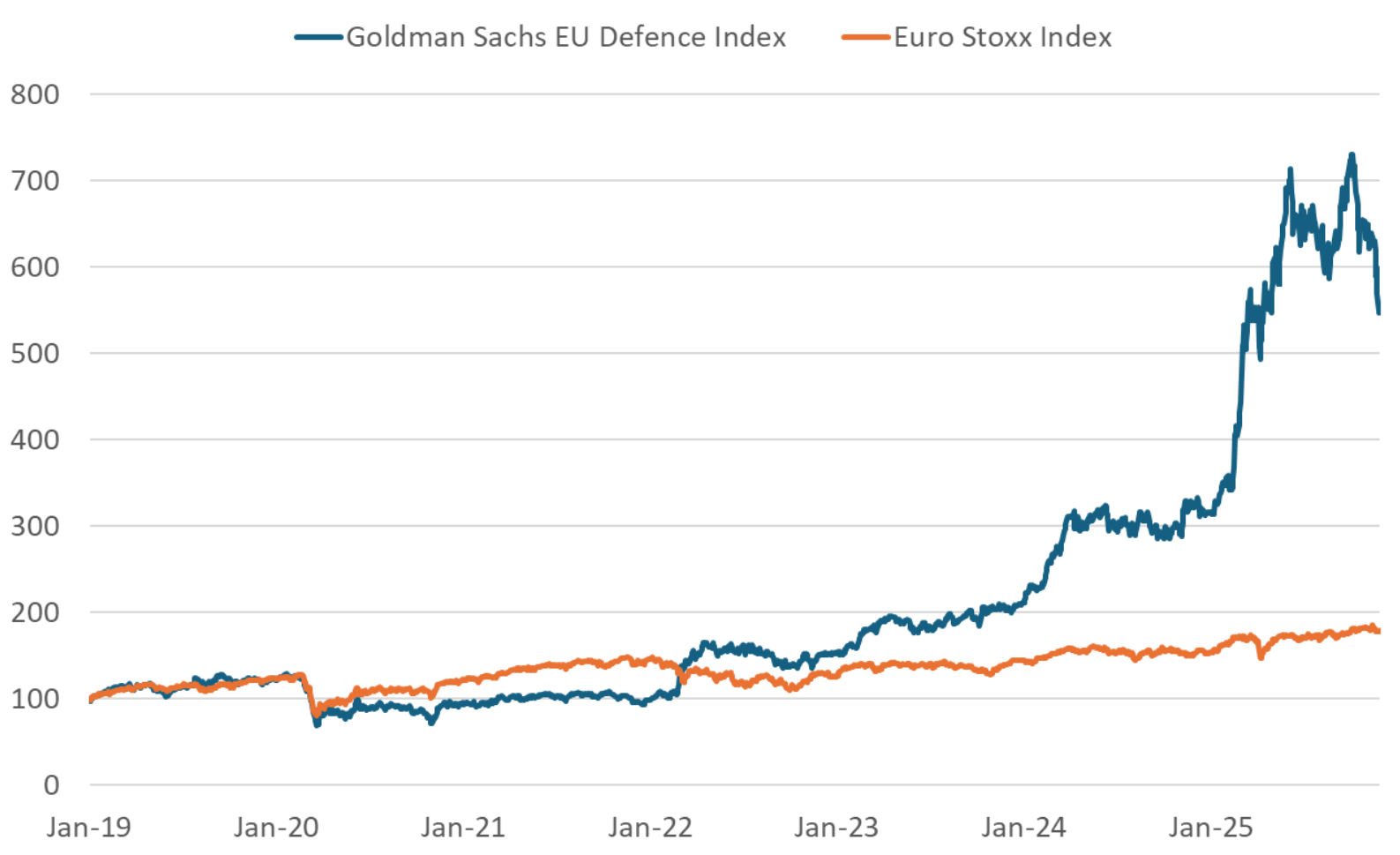

Defence cycle strengthens as wars cool

Even as hopes grow that the major wars could be approaching a turning point, the global defence sector remains firmly in investors’ sights. Defence stocks have posted strong gains as elevated order books and rising government budgets underpin a structural shift in military spending. While the headline risk of war may recede, the investment case is shifting toward a longer-term “super-cycle” of defence capitalisation. Rheinmetall’s recent Capital Markets Day underscored this point. The company outlined some of the most ambitious targets in the industry: revenue of €50 billion by 2030, more than double today’s levels, and an operating margin set to rise above 20%. Management highlighted three fast-growing pillars, Naval systems, Air Defence, and Digital Solutions, all supported by multi-year procurement programmes and a pipeline extending well beyond current conflicts. On the macro side, defence spending as a percentage of GDP is gaining traction. The North Atlantic Treaty Organization (NATO) benchmark has long been 2% of GDP, but many now discuss 3%-3.5% and even 5% as a future yardstick. Meanwhile in Germany, despite strong rhetoric from Friedrich Merz and his government, there is ongoing scepticism about whether the lofty 3.5% of GDP target will be met. Merz himself recently remarked that “the discussion about percentages of GDP is a makeshift construct” and that the real focus must be on actual capabilities rather than arbitrary benchmarks. For global equity investors, this signals a more nuanced tilt: defence is not just a reaction to active wars, but part of a longer-term structural cycle in spending. Selective exposure remains compelling, yet the geopolitics, public finances and regulatory backdrop warrant vigilant monitoring.

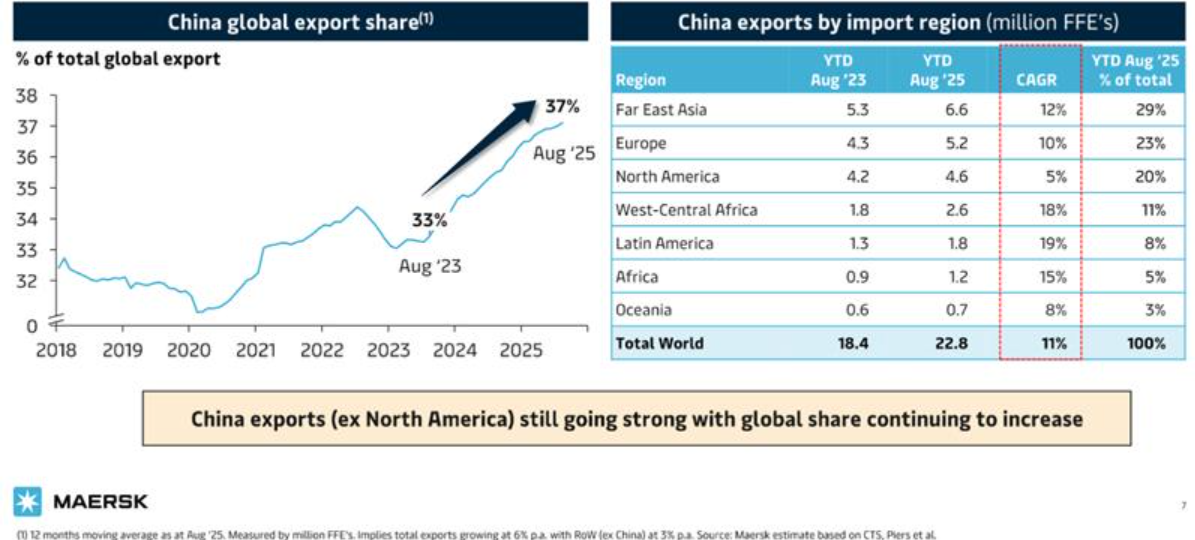

Trade Rebalancing: China shifts beyond the United States

During the presentation of its 3Q25 results, Maersk underlined that exports from China to the US have been slowing significantly during 2025. At the same time, exports from China to other regions remain healthy and are the main driver of global container growth this year. Maersk data indicate that while exports to North America grew only 5% CAGR from August ’23 to August ’25, Chinese exporters redirected capacity toward other markets: shipments to Europe and Far East Asia rose 10% and 12% CAGR, respectively, while Latin America and West-Central Africa surged 19% and 18%. This mix shift lifted China’s global export share from 33% to 37%, underscoring Chinese exporters’ efforts to find alternative destinations for their goods. The weakness in imports into the US is mainly attributable to tariffs imposed by the Trump administration on China-made products. Recent signals from Washington and Beijing point to tentative progress toward a limited trade framework, however, the outlook remains uncertain, as the two sides have not yet reached an official agreement.

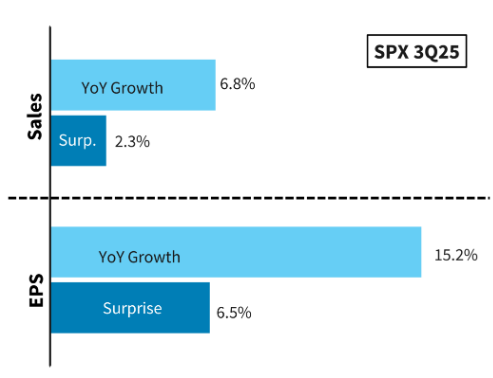

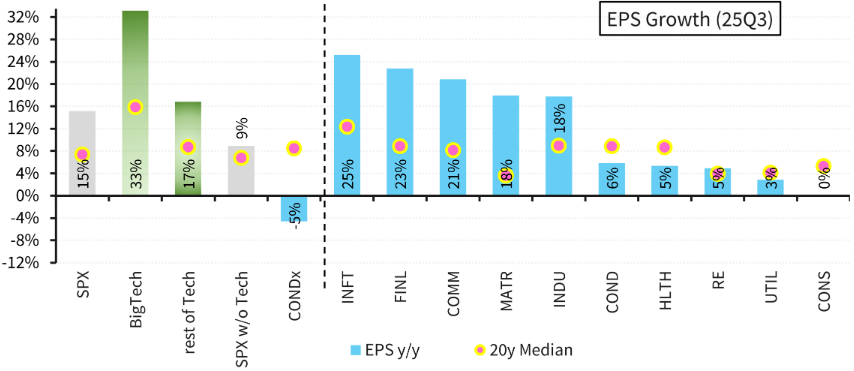

Q3 Earnings breadth improves outside big tech

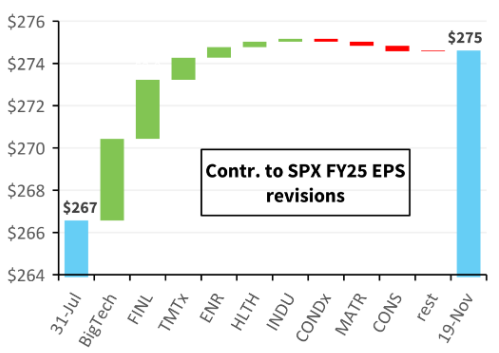

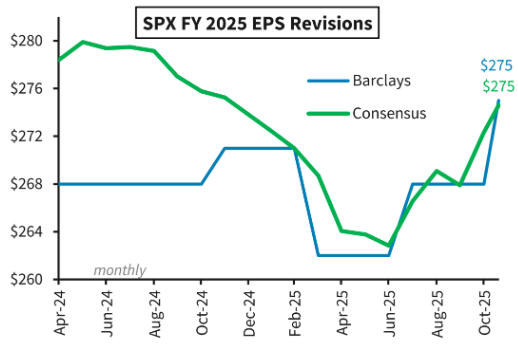

The latest earnings season beat expectations by a wide margin, with S&P 500 EPS up 15.2% YoY and a 6.5% positive surprise. Revenues also surprised to the upside, though more modestly, with sales up 6.8% YoY and a 2.3% beat. For the first time in many quarters, Technology lagged the broader market on EPS surprises. Big Tech delivered only a ~2.1% surprise versus ~11% for the rest of Big Tech excluding Meta. This miss was mainly due to a Meta tax one-off that pulled down the whole sector’s surprise factor. Despite that, Big Tech earnings growth re-accelerated to about 32% in 3Q, up from 28% in Q2. Looking ahead, consensus still expects roughly 20% EPS growth for Megacaps over the next three quarters. Given the strong exit rate from 3Q, these forecasts are likely biased to the upside. Full-year index earnings have been revised up to around $275 from $267 expected in July. Megacaps (TMT) and Financials have driven most of this upward revision.

Source: LSEG Data & Analytics, Bloomberg, Barclays Research. Data as at 20/11/2025.

Source: LSEG Data & Analytics, Bloomberg, Barclays Research. Data as at 20/11/2025.

Earnings contribution is an “estimate” calculated using index shares and Qtr EPS. It assumes Index Divisor to be a constant, and so is not affected by individual stocks. Data as of 20/11/2025.

Source: Bloomberg, LSEG Data & Analytics, Barclays Research.

Source: Bloomberg, LSEG Data & Analytics, Barclays Research. Data as of 20/11/2025.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.