Real Estate and the Trump Playbook: Why property could be the next political trade

While much of the political debate around the Trump return focused on energy, trade, and geopolitics, one sector that may quietly emerge as a key beneficiary is U.S. real estate. Often overlooked in macro discussions, real estate sits at the intersection of economic growth, household wealth, and financial stability, making it a natural target for policy support in a politically sensitive environment.

With housing affordability strained, the incentives for a more real estate-friendly policy stance are becoming increasingly clear.

Why is housing stuck?

A helpful way to frame the housing market is that U.S. housing is not simply weak or strong. It is “stuck.”

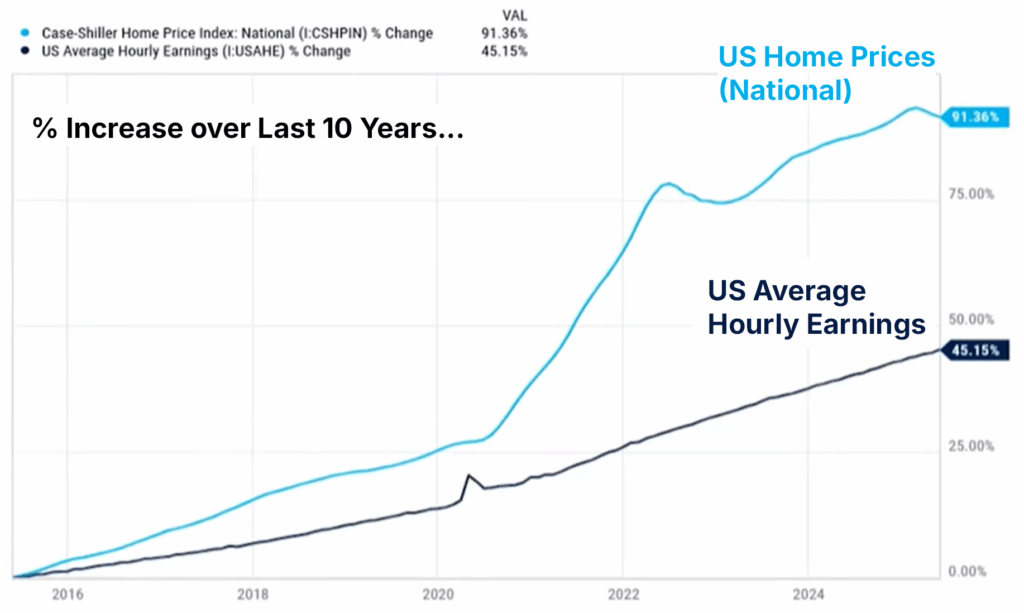

On the demand side, affordability has deteriorated sharply because mortgage rates rose much faster than incomes. Monthly payments became the binding constraint, not home prices alone. That’s why home sales and transaction activity can be depressed even when prices remain resilient.

On the supply side, inventories have stayed tight. Existing homeowners are effectively locked in: many refinanced at very low rates in prior years, and moving today would mean giving up that cheap mortgage and taking on a much higher payment. This “lock-in effect” reduces supply and prevents a traditional housing reset.

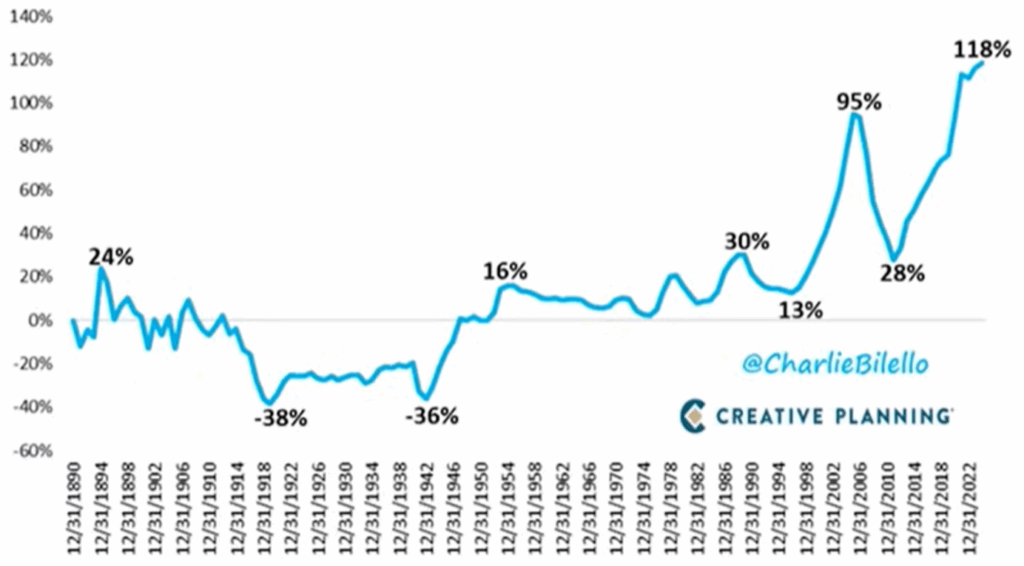

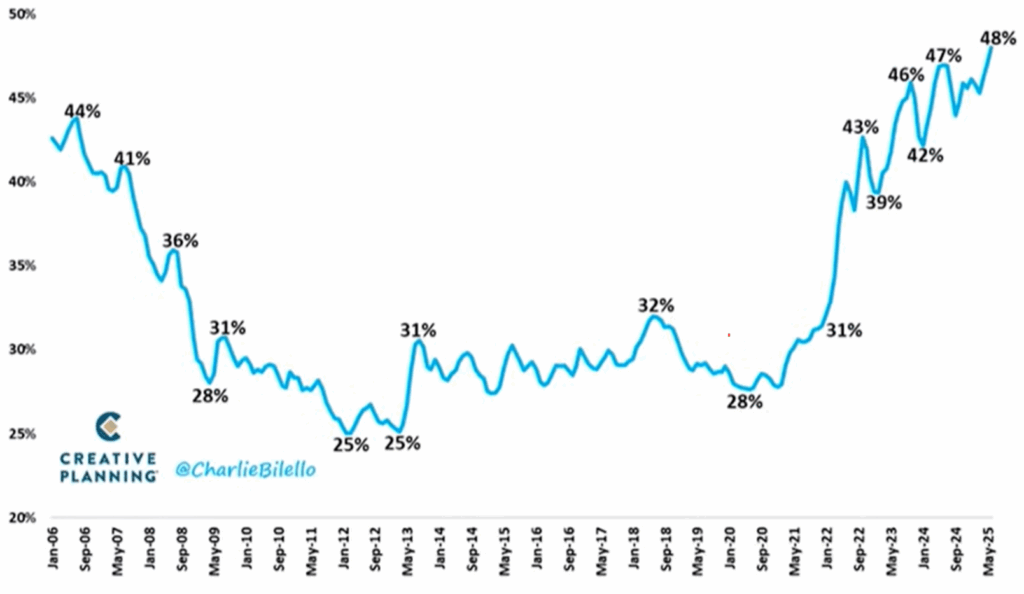

Fonte: Charlie Bilello su X, 6 gennaio 2026.

US Real Home Price Appreciation (Adjusted for inflation, Annual Data, 1891-2024). Fonte: Charlie Bilello su X, 6 gennaio 2026.

US Median Housing Payment as % of Median income (Note: Payment includes P&I, Taxes, Insurance, PMI) Data Source: Atlanta Fed (as of June 2025). Fonte: Charlie Bilello su X, 6 gennaio 2026.

Real estate in the U.S. economy: too big to ignore

Real estate plays an outsized role in the American economy. Directly and indirectly, real estate activities account for roughly 15% of U.S. GDP. Housing alone represents the single largest component of household wealth, while commercial real estate underpins large parts of the banking and credit system.

Such scale matters politically. A prolonged downturn in real estate would not remain confined to asset prices as it would spill into employment, consumer confidence, bank balance sheets, and local government finances. This explains why U.S. administrations historically have been reluctant to allow real estate stress to evolve into a systemic issue.

Today’s setup is particularly delicate. As higher interest rates have pushed mortgage affordability to multi-decade lows, transaction volumes have collapsed. For commercial real estate the problem is even worse: in addition to high interest rates, low demand due to office vacancies due to remote working have reset valuations sharply. This adjustment might be economically rational, but is politically uncomfortable.

Why Trump would care about real estate

Donald Trump’s relationship with real estate is personal, symbolic, and strategic.

First, Trump background is deeply rooted in real estate: his father built and owned large amounts of housing in New York. Even today, the Trump Organization is fundamentally a real-estate company.

Second, real estate aligns with Trump’s core political narrative: tangible assets, domestic investment, construction jobs, and visible economic activity. Supporting it fits naturally into a “pro-growth, pro-America” message, especially compared to more abstract policy areas.

Third, real estate weakness disproportionately affects politically sensitive constituencies like urban centres, regional banks, and middle-class households. Stabilizing property markets helps protect employment, local tax bases, and financial institutions without requiring explicit bailouts.

What form could “help” actually take?

Any support is unlikely to be framed as a direct bailout. Instead, it would likely come through indirect but powerful channels:

- Pressure for easier financial conditions, as recently seen with the whole Jerome Powell saga. Even modest declines in long-term yields have a material impact on real estate valuations.

- Regulatory flexibility for banks, easing capital treatment, or encouraging “extend and pretend” strategies should increase mortgage volumes, particularly for commercial real estate.

- Tax incentives, including accelerated depreciation, favorable treatment of capital gains, or incentives for redevelopment.

- Reduced regulatory friction, which can lower development costs and shorten project timelines.

In recent weeks some proposals have been circulated, as preventing institutional investors from buying single family homes, and increasing the purchase of Mortgage Backed Securities by government-sponsored enterprise.

Who would benefit in equity markets?

Clearly, a more supportive real estate backdrop would have equity implications, but a pro-real estate policy tilt would not lift every stock equally.

- Regional Banks remain one of the clearest beneficiaries of a stabilizing real estate narrative. Commercial real estate loans are a major overhang, and the market continues to worry about refinancing risk and collateral values, particularly in office. Banks can rally not because fundamentals suddenly improve, but because the probability of a disorderly outcome declines.

- Homebuilders are often treated as a pure beneficiary of any housing-friendly narrative, but the reality is more complicated: even if policy support improves confidence, affordability remains tight unless mortgage rates decline meaningfully. In this scenario, builders may need to support demand through lower prices. That means the sector can end up trading higher volumes for lower margins. This implies that risks for homebuilders are still in place

- Housing Related Consumption: if housing activity stabilizes and prices remain firm, consumer confidence and household spending tend to follow. That can benefit a broad range of consumer and housing-adjacent names: home improvement retailers, building products, and renovation-linked demand.

Conclusion: From structural headwind to political optionality

In today’s environment, where real estate stress coincides with election dynamics and a fragile banking system, the probability of supportive measures may be higher than markets currently reflect.

A Trump-friendly tilt toward real estate could support sentiment, ease refinancing pressure, and reduce tail risks, but the winners would be unevenly distributed. Banks and interest-rate-sensitive REITs may offer the cleanest exposure, while homebuilders could benefit from improved activity but still face margin pressure in an affordability-constrained world.

In other words: this is not a simple “Trump = housing boom” story. It is a “Trump = policy backstop and risk premium compression” story. Will that be enough?

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2025 Algebris Investments. Algebris Investments is the trading name for the Algebris Group

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.