On March 10th 2023, Silicon Valley Bank (‘SVB’) was taken over by the FDIC, following a wave of deposit outflows. Markets looked at the event as a potentially systemic risk for the US and global banking sector.

We disagree with this interpretation of events. SVB stress is due to an idiosyncratic deposit base facing significant outflows, which exposed the bank to sharp losses on its outsized securities portfolio. As we show below, SVB was a major outlier in terms of the degree to which they were facing deposit outflows (after a tremendous surge in deposit growth in the previous three years), the unusual deposit base dominated by high-balance (and uninsured) accounts, and the extent of the bond losses. The vast majority of large US banks, and certainly holdings across our portfolios, have a more diversified, stable deposit base and robust capital positions both on a spot and mark-to-market basis.

As a result, the read-across is miscalibrated and we view significant weakness across the banks’ capital structure an opportunity to buy, particularly in the high quality names in the sector.

What is and what happened to Silicon Valley Bank

SVB was not a typical US bank and stood out for several reasons. Its business model focused on the venture capital ecosystem. This allowed SVB to grow exponentially in the past four years, growing assets and deposits by >200% to $220bn and $198bn at their peaks, respectively. This compares to many of their peers that saw deposits grow at a much lower rate.

The rapid expansion came at the cost of diversification, laying the foundation for much of today’s issues. As of the end of 2022, the deposit base was highly concentrated in large accounts, with $152bn of its $173bn above the FDIC insured limit. As a comparison, the average US bank in our portfolio has nearly two-thirds of their deposit bases in insured accounts, versus just 12% at SVB. Many of SVB’s deposits were invested in long duration fixed-rate securities that became underwater as rates have risen, creating both earnings pressures from a negative carry trade as well as capital pressure due to a decline in the value of the bonds.

On Wednesday, SVB announced the sale of some of its securities reporting a $2bn loss and a concurrent equity offering. The catalyst appeared to be accelerating deposit outflows, which were 13% of peak deposits as of 4Q22, already >3x the average US bank even before the trends worsened at the beginning of this year. Widespread worries around the bank’s liquidity position in the aftermath of the deal announcement quickly led to a deposit run, failure of the capital raise, and ultimately the takeover by FDIC earlier today.

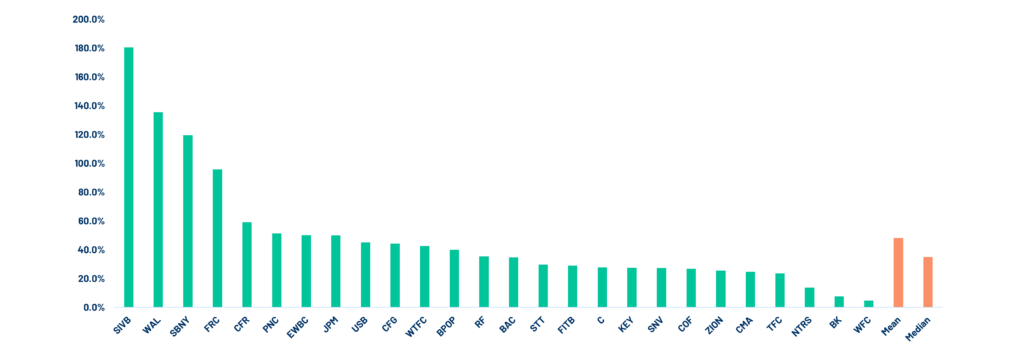

Source: S&P Global, Algebris Investments. Data as of 31.12.2022.

A (mostly) idiosyncratic issue

Developments around SVB caused indiscriminate selling across US banks on Thursday, which spread to Europe on Friday on fears of contagion. For sure, the fallout from SVB may continue for some time as the FDIC works to resolve the bank and there could well be implications for the economy to the extent part of its large startup customer base faces a liquidity squeeze. In this way, a liquidity mismanagement could ultimately lead to some credit issues for those banks exposed to venture capital-backed companies. However, assuming the economic impact is relatively contained, we do not see a clear read-across, particularly for the larger US and European banks, for several reasons.

Large banks are subject to more comprehensive and thorough regulation. For instance, in Europe, banks are limited in how much rate mismatching they can take on their held-to-maturity bond portfolios, due to Basel 4 regulations. This means that they will not face the same steep negative equity position that SVB found itself in with its deeply underwater securities book. Hence, the average European bank has losses of just ~5% of tangible equity, compared to the 124% that SIVB showed as of year-end; our US holdings are comparable to the average US bank on this basis. See chart on left in the chart above.

Further, European and large US banks must deduct unrealised losses on securities accounted at fair value (ie, marked to market on a quarterly basis, in contrast to held-to-maturity) from their regulatory capital. Looking at the banks we own, stressing the capital for a mark-to-market of the entire asset portfolio (i.e. securities held at fair value as well as those held to maturity) would still leave capital in significantly positive territory. See chart on the right in the chart.

Liquidity is also substantially better across the larger US banks and in Europe, partly due to rules around liquidity management and stress testing like the liquidity coverage ratio and net stable funding ratio – neither of which SVB was subject to, leading to a deeply mismatched balance sheet. Further, US and European banks typically have highly diversified and granular deposit base, in sharp contrast to SVB, making the probability of large withdrawals remote. Sectoral and geographical diversification strengthen deposit stability. And finally, in Europe, where deposits are still growing, banks are sitting on $3tn of excess liquidity representing about a quarter of the system’s deposit base, and have an additional $1tn government securities market at fair value, as additional liquidity buffer.

Source: S&P Global, Algebris Investments. Data as of 31.12.2022.

Our focus on quality

We were well attuned to the problems percolating at SVB, and in fact had a short in the stock where we had capability to do so. Our focus in investing in Financials is very much on quality, and idiosyncratic event such as SVB serve as a constant reminder as to why we prefer larger, systemic and well-regulated banks. These banks were also the most affected by regulations introduced post-2008 and are subject to the most arduous requirements and tightest supervision by regulators. In this period of wider market weakness, we have therefore maintained high conviction across our names and view the recent sell-off as buying opportunity at attractive valuations where quality names trade at 5-7x earnings for double-digit ROTE and high-single digit dividend yields.

This document is issued by Algebris (UK) Limited. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris (UK) Limited.

Algebris (UK) Limited is authorised and Regulated in the UK by the Financial Conduct Authority. The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Under no circumstances should any part of this document be construed as an offering or solicitation of any offer of any fund managed by Algebris (UK) Limited. Any investment in the products referred to in this document should only be made on the basis of the relevant prospectus. This information does not constitute Investment Research, nor a Research Recommendation. Algebris (UK) Limited is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris (UK) Limited , its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is for private circulation to professional investors only.

© 2023 Algebris (UK) Limited. All Rights Reserved. 4th Floor, 1 St James’s Market, SW1Y 4AH.