At the beginning of 2018, we positioned more cautiously for markets caught between headwinds from the end of QE and tailwinds from positive growth. This is what happened so far and what we expect from the second half of the year:

1. Financial markets have underperformed the economy. Growth continues to be positive, with upward momentum in the US and fading momentum in Europe and EM. However, without central banks as marginal buyers, financial assets have moved lower. One by one, QE-supported carry trades in rates, credit, FX, volatility have re-priced. Markets continue to appear fragile, as we highlighted in our last Silver Bullet │ The Age of Fragility.

2. The US continues to outperform the rest of the world. The Trump Administration’s tax cuts have helped to isolate US financial markets. US high yield bonds are the only credit asset class close to flat year-to-date. In our view, this will continue to allow the Federal Reserve to carry on normalising policy relatively smoothly, while other central banks struggle.

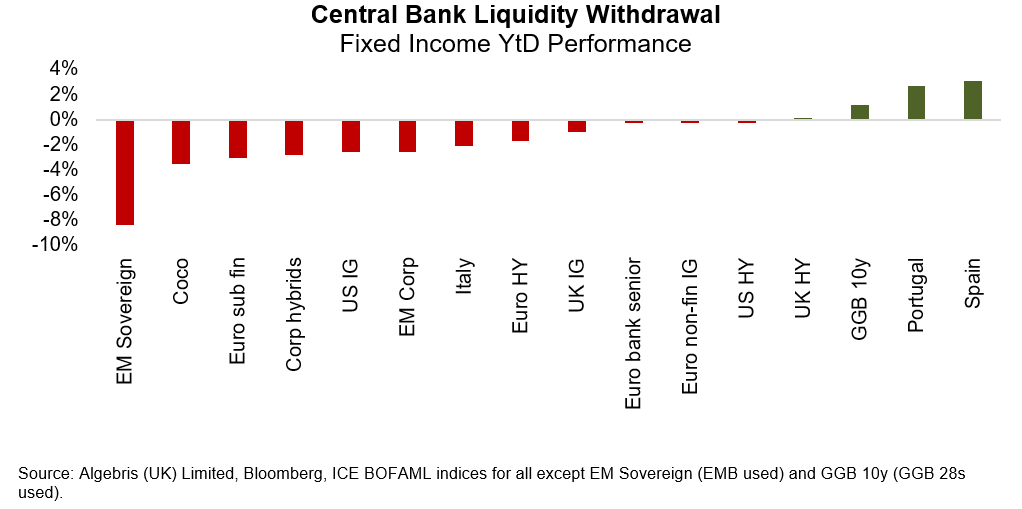

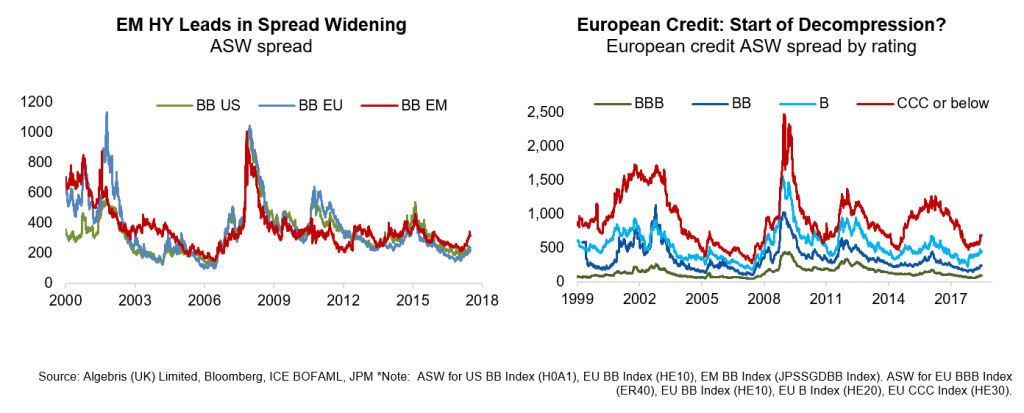

3. Risk premia have re-priced sharply across Europe and EM. Credit spreads in cash bonds have widened and returned to long-term averages in Europe, moving above average in the periphery and Emerging Markets. Cash bonds have underperformed CDS hedges.

4. There is no systemic risk but sudden spikes in volatility. The February unwind in short volatility equity strategies has been followed by turmoil in EM (Turkey, Argentina, Brazil), Europe’s periphery (Italy), high yield credit and other cash-park assets like crypto. But while the direction is downwards, the speed of the re-pricing is so far slow – perhaps given that most central banks other than the Fed remain dovish. This slow motion re-pricing means it is harder to hedge using volatility products and derivatives in general.

5. Can the re-pricing accelerate? A combination of rising trade wars, geopolitical risks, negative fund flows across risky assets and lower trading liquidity could push markets to overshoot. That said, growth remains positive and our models see a relatively low chance of a turning point in default rates – especially in Europe, where corporate and bank balance sheets have not taken advantage of low interest rates to leverage. US credit markets and US assets generally appear more vulnerable instead, with little re-pricing happened since the beginning of the year and triple-C low quality debt compressing to record tight spreads.

What Are the Risks Ahead?

1. Trade Wars

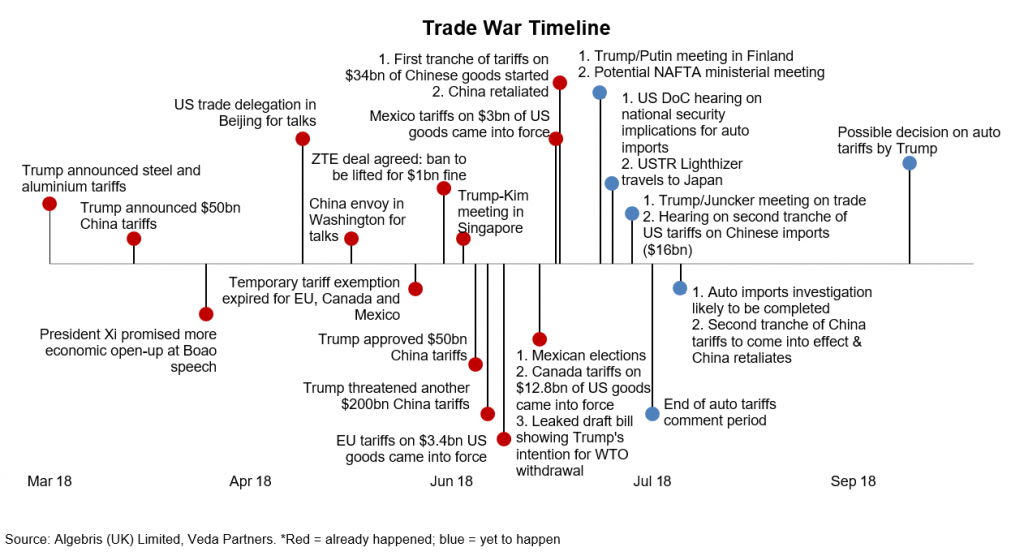

We wrote earlier this year that the exchange of tariff threats between the US and its trading partners could evolve into a wider trade war, hurting global growth and confidence. Since then we have seen an escalation of tensions and tariffs coming into action (see timeline below). It has also become clear that the US demands not only a deficit reduction but a more structural change to its trade relations with the rest of the world. In our view, the US is likely to stick to its hard stance for two reasons. First, trade tensions so far have not hurt growth in the US: data remains strong and the Fed’s GDP Nowcasts continue to point to robust expansion (NY Fed, Atlanta Fed, St. Louis Fed). This gives the Trump administration more flexibility and likely has led them to believe that the US has more leverage in trade negotiations. Second, the Democrats’ poll lead over the Republicans for the midterm elections has been narrowing this year, while President Trump’s approval ratings has strengthened. The administration likely has gained more confidence that the majority of voters agree with their trade policies.

In the coming months we will see developments in the following areas:

US-China tariffs and investment restrictions: The US’s main aim is likely to contain China’s technological advancements, as outlined in the “Made in China 2025” plan. It has announced $50bn of tariffs, focusing on sectors linked to the 2025 plan. Trump has also ordered his administration to identify another $200bn of Chinese imports for tariffs if China retaliates, and threatened on a further $200bn. The House and the Senate also passed a bill to enhance power of the Committee on Foreign Investment in the US (CFIUS), which means more checks on China’s investments in US companies. We think while China wants to avoid a trade war, it will have to retaliate given the strategic importance of developing its high-tech industries for long-term growth.

NAFTA: The three sides failed to reach a deal before the Mexican election, in which leftist candidate Andrés Manuel López Obrador scored a land-slide victory. His appointed finance minister Carlos Urzua suggested renegotiations would continue. However, the process could become lengthier as the time pressure to strike a deal before the Mexican vote becomes irrelevant.

Auto tariffs: President Trump has ordered a “Section 232” national security probe into auto imports – the same procedure that led to the imposition of steel and aluminum tariffs. The EU has already warned of retaliation if auto tariffs are imposed. Tit-for-tat tariffs on autos could mean a significant escalation of trade war given the increase in scale: the EU warned that global retaliation on auto tariffs could be $300bn.

Are trade war risks adequately reflected by risk premia? According to JPM estimates, markets have priced a -0.5% slowdown in global growth – equivalent to the impact of a 10% tariffs by the US on all imports and with full retaliation. However, the risks of further escalations into a global trade war, disruptions to supply chains and loss of confidence are not yet fully priced.

2. Centrifugal Politics in Europe

In Germany, Chancellor Merkel’s open-border policy decision in September 2015 overwhelmed domestic political consensus, aiding in the emergence of the AfD as a force on the political right. That decision triggered in the past few months the worst political crisis in the CDU/CSU alliance in decades. Germany’s interior minister (and CSU leader) Seehofer’s ultimatum to close the German border to asylum seekers however, has to be taken in the electioneering context of the upcoming October Bavarian federal state election, in which the CSU risks losing its absolute majority via a voter leakage to far right AfD.

We think CSU leadership will value their long term influence in national politics above a short term symbolic victory – including up-and-coming CSU hard liner and chief Seehofer rival Markus Söder. Conservative CSU voters are likely to value the stability of the Federal Government and conciliatory tactics rather than Seehofer’s frontal clash approach going forward – particularly now that some concessions appeared to have been extracted from Merkel. We expect, however, German political stability risks to add uncertainty and another overhang over the Euro and European markets over the illiquid summer months, up to the October elections and beyond, as the immigration issue remains far from resolved.

While the statement from the late June Eurogroup meeting has proven enough to placate the CSU temporarily, the muddled outcome included a promise to help periphery nations deal with the immigration cost that is unlikely to be quickly acted upon. In the likely event of slow progress, we see the next episode of European disagreement to emerge from Italy’s anti-immigration government, where unlike in Germany, conflict with the EU and chancellor Merkel is well rewarded at the polls.

3. Oil Shock Risk

We have argued in previous Silver Bullets that geopolitical risk represents an underpriced downside risk to supply, and upside risk to oil prices. Whilst there remains plenty of room for further escalation, especially in the middle-east, some of these risks have started to be reflected in current prices. The 90-day wind down period for foreign businesses to disassociate with Iran following the US withdrawal from the nuclear agreement ends on 9th August. Iran’s oil exports are likely to be severely affected. The recent OPEC agreement to increase supply failed short of worries around loss of supply from Iran and Venezuela. Further increases at the September meeting are likely. We previously expressed concern that a supply-shock driven increase in oil prices can negatively affect global growth, with negative feedback loop for commodity prices. These concerns are further increased from tensions arising from trade wars. Global economic confidence has already been affected, and monetary authorities around the world are sounding the alarm on the consequences for global growth. This tempers our long-standing bullishness on oil prices. Whilst global demand has not softened materially yet, downside risks have certainly increased. Some commodities, such as copper, have already begun to reflect these risks. Oil prices continue to enjoy solid tailwinds from supply, but demand headwinds are gaining strength.

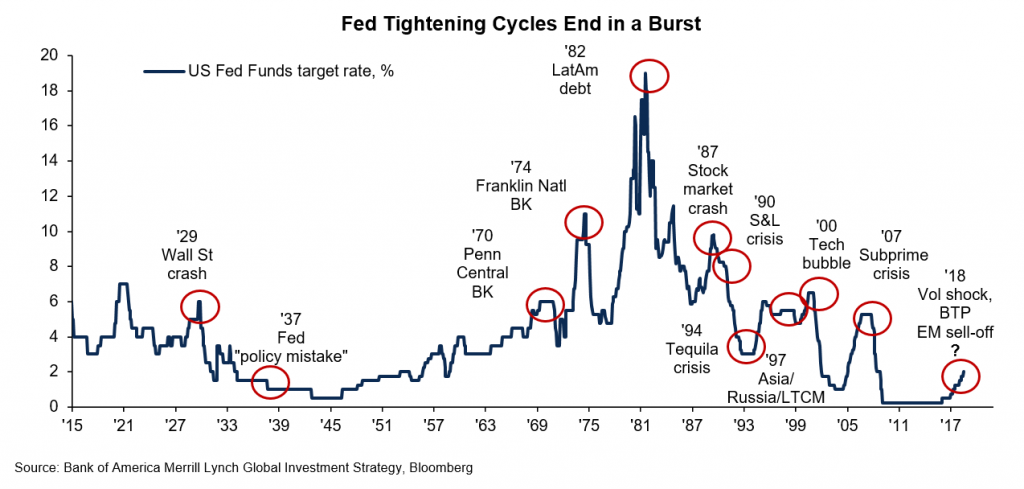

Will the Federal Reserve blink?

In our view, it would take a significant risk event for the Fed to either pause rate hikes or indicate rate cuts. In fact, we think the Fed’s tolerance threshold is higher than that of other major central banks.

This higher tolerance can firstly be explained by the resilient US economy: growth is still booming, wages are rising albeit slowly, and there’s a risk of late-cycle inflation. Secondly, the Fed may be keen to build an adequate monetary policy buffer heading into the next recession, especially as the government has limited room for further fiscal stimulus.

However, there are risks looming which could turn the Fed dovish. Amongst those risks, the most significant is the risk of a trade war. Thus far, the trade war has been limited to just tariffs on steel and aluminum imports, and articles such as washing machines and solar panels. The overall net negative impact on US GDP from this is potentially small (GS research) and most recent hard data indicates that the economy has been left largely unscathed. However, there have been casualties and cracks are beginning to appear. In June, the US’s largest nail manufacturer laid off 10% of its staff to avoid insolvency as steel costs soared. Furthermore, at the Fed’s June Q&A session Chair Powell highlighted that businesses are for the first time indicating caution in capital spending and hiring. If the trade war further escalates and rhetoric turns into reality, the impact on the US economy could range from -0.1pp to -1pp of GDP (-0.1pp impact from tariffs on $50bn Chinese imports and 25bp in tightening financial conditions, to -1pp impact from 20% tariff on all Chinese imports in to the US; MS research). Thus the negative impact of a trade war could eventually more than offset the economic boost caused by President Trump’s fiscal stimulus plan, and this may serve as a catalyst for the Fed to blink.

Conclusions

1. We are still cautious. At the beginning of the year, we flagged our more cautious view on 2018, on the combination of a potential return of volatility vis a vis still positive global growth. As discussed last month, our view remains cautious, as the retreating wave of central bank liquidity has pushed assets to re-price in an environment of lower trading liquidity. This means we have improved substantially portfolio liquidity, either substituting cash instruments with derivatives or using barbell strategies.

2. But opportunities are starting to arise. That said, there are parts of credit markets where risk premia imply a return of the Eurozone crisis or an Emerging Markets crisis. This means that a mid to low-duration high yield portfolio today can yield 5-7%. On the other hand, other QE-driven trades appear still crowded and vulnerable to us. These include long-dated triple-B bonds, or short volatility.

3. Our Macro Credit strategy was hurt by spread widening its credit book through the year, despite having scaled down risk in January. We maintain hedges in QE-sensitive markets, particularly in EM as well as in tight investment grade credit, while holding a net positive carry in medium to low-duration high yield bonds, which now offer high single digits yields. The overall net exposure gains from a decline in stock prices and a widening in spreads.

4. Our Tail Risk strategy continues to be net short, with a focus on IG credit, EM and firms and sectors which we estimate most vulnerable to trade wars and heightened Eurozone risk.

Per ulteriori informazioni su Algebris e i suoi prodotti o per farsi inserire nella lista di distribuzuione, si prega di contattare il dipartimento Investor Relations all’indirizzo algebrisIR@algebris.com. Gli articoli passati sono disponibilii sul sito Algebris Insights

Questo documento è emesso da Algebris (UK) Limited. Le informazioni contenute nel presente documento non possono essere riprodotte, distribuite o pubblicate da alcun destinatario per qualsiasi scopo senza il preventivo consenso scritto di Algebris (UK) Limited.

Algebris (UK) Limited è autorizzata e regolamentata nel Regno Unito dalla Financial Conduct Authority. Le informazioni e le opinioni contenute nel presente documento hanno solo scopo informativo, non hanno la pretesa di essere complete o complete e non costituiscono una consulenza in materia di investimenti. In nessun caso qualsiasi parte del presente documento deve essere interpretata come un’offerta o una sollecitazione di qualsiasi offerta di qualsiasi fondo gestito da Algebris (UK) Limited. Qualsiasi investimento nei prodotti cui si fa riferimento nel presente documento deve essere effettuato esclusivamente sulla base del relativo Prospetto informativo. Queste informazioni non costituiscono una Ricerca di Investimento, né una Raccomandazione di Ricerca. Con il presente documento Algebris (UK) Limited non organizza o accetta di organizzare alcuna transazione in qualsiasi tipo di investimento, né intraprende alcuna attività che richieda l’autorizzazione ai sensi del Financial Services and Markets Act 2000.

Non si può fare affidamento, per nessun motivo, sulle informazioni e sulle opinioni contenute nel presente documento, né sulla loro accuratezza o completezza. Nessuna dichiarazione, garanzia o impegno, esplicito o implicito, viene data in merito all’accuratezza o alla completezza delle informazioni o delle opinioni contenute in questo documento da parte di Algebris (UK) Limited , dei suoi direttori, dipendenti o affiliati e nessuna responsabilità viene accettata da tali persone per l’accuratezza o la completezza di tali informazioni o opinioni.

La distribuzione di questo documento può essere limitata in alcune giurisdizioni. Le informazioni di cui sopra sono solo a titolo di guida generale ed è responsabilità di ogni persona o persone in possesso di questo documento informarsi e osservare tutte le leggi e i regolamenti applicabili di qualsiasi giurisdizione pertinente. Il presente documento è destinato esclusivamente alla circolazione privata per gli investitori professionali.

© Algebris (UK) Limited. Tutti i diritti riservati. 4° Piano, 1 St James’s Market, SW1Y 4AH.