“I’d like to share a revelation that I’ve had during my time here. It came to me when I tried to classify your species and I realized that you’re not actually mammals. Every mammal on this planet instinctively develops a natural equilibrium with the surrounding environment but you humans do not. You move to an area and you multiply and multiply until every natural resource is consumed and the only way you can survive is to spread to another area. There is another organism on this planet that follows the same pattern. Do you know what it is? A virus.”

Agent Smith, The Matrix, 1999

We have entered a process of creative destruction. The old economy – oil, retail, commercial real estate, cars – is clashing with the new. Governments and central banks around the world are deploying monetary and fiscal ammunition to keep economic supply alive. But will demand return to pre-shock levels?

We believe the virus is accelerating history, as we pointed out in The Pandemic Revolution. Today, we have more data points to try to understand where the world is going.

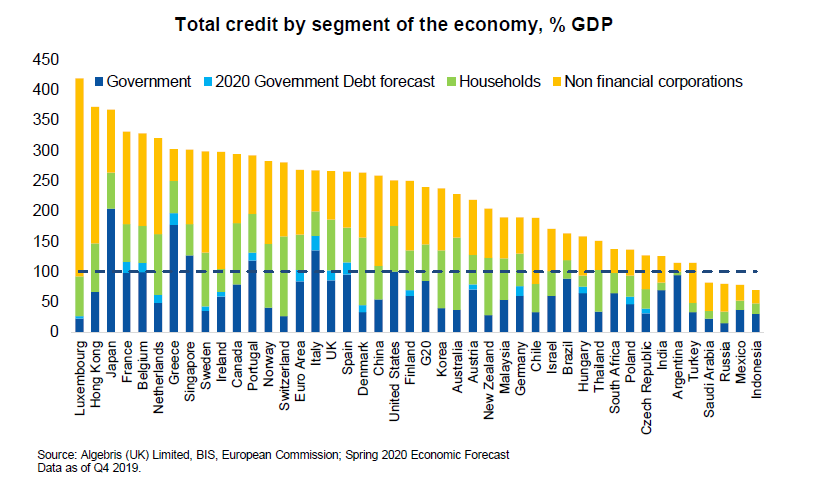

New vs old economy. Technology, telecoms will likely emerge as clear winners, while retail, oil-energy and airlines have been in structural overcapacity and will have to consolidate. Public balance sheets have taken the burden of private debt, but eventually taxpayers won’t be able to keep entire sectors alive, if demand trends shift away from the previous normal. We have classified sectors as winners, survivors and losers based on financial strength, overcapacity and government support.

The strong will get stronger. Public support will be a key determinant of survival. Weak companies in a strong country may get the help they need to survive, while stronger firms in weaker countries may not. The US benefits from its reserve currency status, which has allowed a very rapid monetary and fiscal expansion, without a rise in funding costs or currency depreciation. European policymakers have been traditionally slower-acting. We think the EU’s €750bn recovery fund is a game-changer, including €500bn of grants to weaker countries. Emerging economies may not be able to deploy the same firepower – we see many EM countries facing increasing challenges amid rising debt and stretched monetary policy.

Deflation vs inflation. As excess capacity and excess debt get resized through restructuring, consolidation and defaults, price dynamics are likely to remain deflationary in the near term. However, the unprecedented expansion in central bank balance sheets and fiscal spending begs the question whether inflation is dead, or if it will return in a different form. This is an extremely difficult question: the answer depends on a combination of four unknowns: monetary and fiscal stimulus on the one hand, the virus shock and the oil supply glut on the other. History provides an interesting perspective: where governments face the burden of unsustainable debt, eventually they resort to ways of creating inflation themselves (see also Monetary Regimes and Inflation, P. Bernholz, 2016). We see the potential for supply constraints and bottom-up economic policies bringing inflation higher over the coming years.

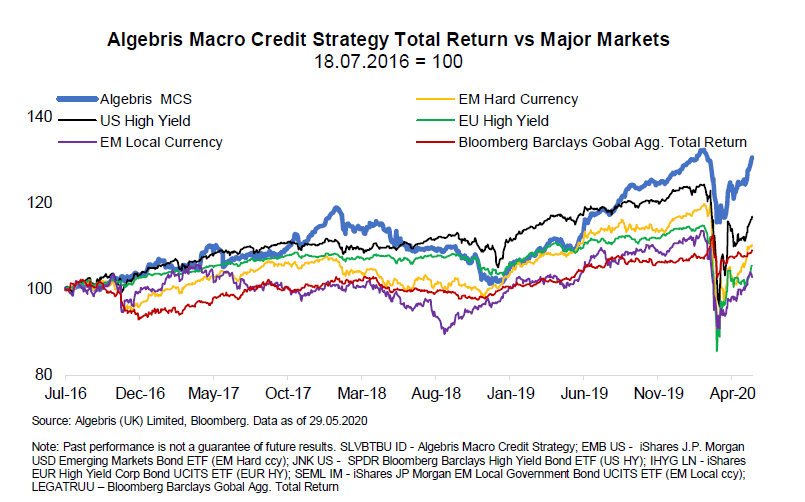

In our Silver Bullet newsletter from March, Nothing Left to Sell, we highlighted that the disorderly selloff created substantial opportunities in fixed income and credit. Today, we still believe this is the right time to invest, and that strategies with an active and selective approach across sectors and special situations should outperform passive beta.

The Strong vs the Weak: Comparing the Speed of Recovery across Countries

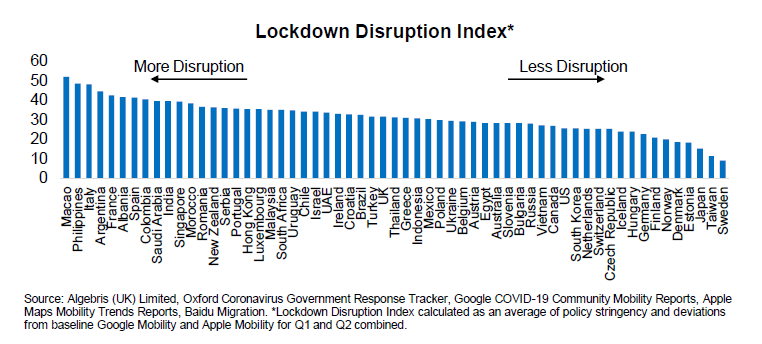

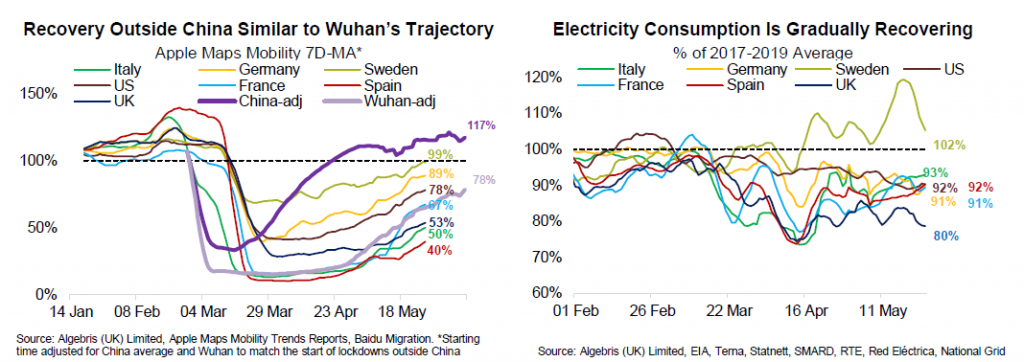

As countries start to exit lockdowns, real-time data suggests that the speed of activity recovery globally is much more gradual than the speed of decline when going into lockdowns. The recovery varies by sector: ground mobility is back to 65-70% of pre-virus levels; average electricity consumption is back to 90% of last year’s level, while air travel is still at around 30%. This is consistent with a faster recovery in industrial and ground transport sectors vs international travel.

Across countries, the more stringent lockdown measures have been, the bigger the dip in economic activity – that said, countries which implemented a faster and more organised response to the virus, are also the ones who may recover earlier. Italy, France and Spain were among the most disrupted economies. In contrast, the Nordics and Germany were among the least disrupted. Sweden and Germany are also leading in the race to normal, while Italy, Spain and the UK are still behind. France seems to be bouncing back more quickly than peers over the past two weeks after the government lifted restrictions.

Most importantly, countries with stronger healthcare systems from the start have been able to combat the virus more effectively, and countries with a larger fiscal capacity have been able to support businesses with a stronger and faster stimulus. As our analysis shows, countries’ effective reproduction numbers (R0) after 6-8 weeks of lockdowns seem to be negatively correlated with their GHS scores in Health Sector Robustness and Overall Country Resilience, regardless of lockdown strictness. In other words, stronger countries are likely to be more efficient in mass testing, contact tracing and quickly isolating infected cases, which are what matters in controlling the virus. This helps explain why countries like Germany, South Korea and the Nordics were able to manage their respective outbreaks with less activity disruptions.

The Winners, the Survivors and the Losers: Opportunities in Credit

While indices and in particular investment-grade assets have repriced aggressively thanks to central bank action, high yield and off-benchmark assets remain dislocated and are underpricing the potential for a recovery.

Survivors: we see alpha opportunities in stressed credits with upside potential from policy support or from a resumption in activity.Our framework to selecting non-financial credits is based on (a) our estimate of their revenue-recovery and ability to manage costs post COVID, (b) liquidity and (c) positive idiosyncratic catalysts such as a capital-raise or creditor-friendly restructuring.

To understand the speed of the recovery in each sector, we are closely monitored consumer spending patterns in countries emerging from a lock-down. The strongest recovery has been in autos and some consumer sectors (e.g. cosmetics, gaming). Autos have the additional benefit of strategic-sector support, as in Europe, as well as being the new preferred travel option given health concerns. Names within these sectors where we see upside include Adient, a car-seat manufacturer, Adler, a manufacturer of auto-acoustic parts and Codere, a gaming company active in Europe and South America.

Amongst financial credits, we see value in peripheral additional tier-1 (AT1) or bank lower-tier debt (LT2) which have lagged the rally and are likely to receive support, given banks remain the primary means of accommodative policy transmission to peripheral citizens and businesses. We are long major core and periphery banks, and in particular we see upside in Deutsche Bank and Monte Paschi LT2, on potential sovereign support, and UniCredit Cashes on a substantial mispricing vs AT1.

Winners: we continue to like credits which have rallied but offer a good coupon with strong fundamentals.At the height of the sell-off, we added in issuers which fit the profile of a strong company in a strong country. This two-pronged approach gave us the added comfort that while the companies were likely to withstand a severe COVID crisis, they would receive sovereign support before others in their country if the virus was a lot worse than feared. These credits include, those in autos (VW, Ford), manufacturing and construction (GE, Vinci), telecommunications (Vodafone, Telecom Italia), utilities (EDP, ENEL), banks (Barclays, Intesa, BNP) and energy (Total). While we have lightened up our exposure in these names, we have kept about half of our original exposure. These bonds still pay an average yield of 5%, which remains attractive.

We have also switched risk from credit to convertibles in investment grade, which offer higher spreads, being outside the ECB’s eligible universe, and additional upside convexity through equity optionality (Total, Veolia, Deutsche Post, Siemens, Alibaba, BP, Dufry, Sacyr).

Losers: we remain cautious on zombie-firms in sectors with capacity overhangs.Even before the COVID crisis hit, we were cautious on sectors that were in a secular downturn (retail, energy) or had high operating leverage (commercial airlines). Airlines in particular have received almost €30bn of state support in Europe and c$20bn in the US. These sums, while significant, are sufficient if travel recovers up to 75% of pre-crisis levels by 2021, but are not if it takes longer.

Therefore, we remain cautious on airlines and have added forward-starting protection in some over-levered airlines: we have bought short-dated credit and sold longer-dated credit, which traded at near similar prices despite the significant difference in risks. Even with state-aid which has helped kick-the-can, long-term solvency concerns persist, in our view.

Inflation: Fuel Waiting for Fire

Inflation risks have risen dramatically over the past two months, but are unlikely to materialize before 6-9 months. Longer-term, inflation remains one of the main risks for the market.

The massive balance sheet expansions of global central banks provide fertile ground for inflationary pressures over the next few years. True, QE has been there for the past ten years, and inflation didn’t pick up. The main reason why QE Infinity failed to lift inflation, in our view, is a collapse in the velocity of money. While inflation is ultimately a monetary phenomenon, monetary theory assumes that money is used for economic transactions – instead, a large part of central bank balance sheet expansion has ended up in financial assets and particularly in cash-park assets like short term government bonds, housing, art, collectibles and gold. Put differently, the transmission mechanism of monetary policy from money supply to credit and the real economy remains broken. That said, things could change radically going forward, with governments and central banks deploying new, more aggressive tools.

From QE 2 to QE 3: debt monetisation is closer. The Fed has stepped-up purchases by more than 10% of US GDP in just two months, including several corporate bond categories that were previously untouched. The increase in Japan has been similar, and a higher PEPP size may put the ECB in the same league. The monetary policy discussion has also reached new boundaries quickly. The Bank of England is openly discussing negative rates. Several Fed speakers have recently revived post-war “yield-curve-control” policies, where central banks target longer-term rates, in absence of room of manoeuvre on short-term rates. New Zealand has already gone down this route. With monetary taboos completely gone, both in terms of size as well as type of instruments, the ground for inflation is as fertile as ever.

New money is now reaching Main Street. One big difference between the current round of QE and the previous one is that monetary expansions are now directly financing fiscal deficits, and such deficits are clearly aimed at boosting spending among low earners. As cash reaches out to households with higher marginal propensity to consume, spending will increase more.

The US administration, for example, has introduced an unprecedentedly large unemployment benefits package. Under the new subsidy, 70% of recipients eligible will receive income exceeding pre-Covid earnings. Workers with particularly low pre-Covid earnings may end up with income more than twice as before the crisis. Considering that unemployed workers in the US reached 24mn at the end of April, the potential for the policy to generate spending once the virus uncertainty dissipates is large.

In many European countries, discussion of various forms of Universal Basic Income are at advanced stages. In Spain, for example, the government has recently announced the introduction of UBI for 850,000 families. Assuming an average composition of 4, this could amount to 10% of the population.

Finally, job retention has been highly incentivized in most countries via expensive Furlough schemes. The UK, for example, has introduced government subsidy for all workers temporarily furloughed between March and October, up to £2,500 per month. The policy has already reached more than 5mn workers and will provide a stimulus in excess of £50bn, by definition focused on low-earning individuals.

As opposed to earlier crises, monetary stimulus is reaching low income’s pocket quickly. The impact of spending and inflation during the recovery is thus likely to be much higher.

Supply disruption and de-globalisation may create bottlenecks. Some supply-side pressures may lead to a transformation of the inflation basket in a few countries, with implications for the price level. In fact, the cost of selected items may increase due to reduced supply or limitations – like air travel or tourism. Moreover, the broad de-globalisation pressure may reduce the price gains from trade for a variety of goods, agriculture being a prime example.

Supply side limitations are unlikely to generate long-lasting inflationary pressures. Food prices displayed an uptick in March and April, but headline numbers have been broadly down due to oil and core components. Moreover, upward pressures on food prices are unlikely to be long-lasting. In China, for example, food prices spiked into the lockdown and eased during reopening. So, in the next few months the recession is more likely to generate deflation rather than inflation. As recovery gets more robust, though, the inflation pre-conditions created by recent stimulus may bite.

We do not believe inflationary pressures will gain steam in the near term. However, given these material risks, we find long-end rates and government debt in developed economies generally unattractive. QE has depressed long-end rates too much, exposing them to long-term inflation risk. Credit and selected emerging markets sovereigns are more attractive, as high spreads and real rates provide a better cushion against this risk. US CPI-linked Treasuries look attractive vs nominals.

Emerging markets: The Good, the Bad and the Ugly

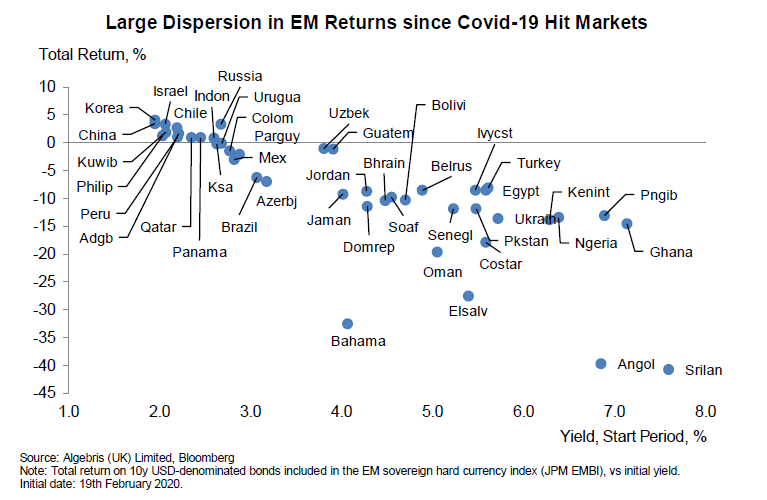

EM as an asset class has lagged the broad credit rally started in April. The hard currency index yields 6% vs 4.5% at the end of January. According to EPFR data, $43bn have left the asset class in 2020. We think it makes sense to increase some exposure as the recovery picks up. Still, picking the right quality layer is key as public debt levels remain high, and not all countries will benefit equally from ample dollar liquidity.

Since February 19th, dispersion in EM bonds returns has been substantial. All countries went down together in March, but only some made it back by May. Performance dispersion is largely a reflection of fundamentals. With solid global growth and low funding costs, market prices did not differentiate much across countries, until this year.

Differences in fundamentals and in policy responses will now matter. A deep global recession will limit the flow of dollars to EMs via a contraction in trade and commodity exports. On the one hand, countries who did not plan ahead for bad times by accumulating reserves or keeping debt levels in check risk debt restructurings or large devaluations. Spread levels and FX volatility will thus remain high in these countries. On the other hand, the large liquidity injection performed by global central banks will quickly find its way through higher quality assets. The market bifurcation that characterized the past three months will thus persist, in our view.

The good: Indonesia, Egypt and selective energy firms. Indonesia is one of the few local markets where the central bank maintained a dovish but cautious attitude and a steady eye on FX. 8% yield after a 20% devaluation make the bonds attractive. Egypt is a laggard despite solid reserves and renewed IMF engagement. With reform momentum ongoing in the past two years and market access preserved during the Covid crisis, the bonds remain undervalued. The oil slump made valuations in government-owned energy names like Petrobras (Brazil) or Pemex (Mexico) very attractive.

The bad: Turkey. We believe Turkey is approaching a balance-of-payments crisis as a result of the Covid crisis. The global financial stress has exposed Turkey’s Achille’s heel, a consequence of several years of short-term policy decisions. As the Covid crisis hit markets, global investors scrambled for dollars and the Central Bank of Turkey cut rates aggressively. As a result, pressure on the lira intensified.

The central bank has tried to defend the currency aggressively. Gross reserves fell by a third in March, as shown on the left. The net figure is even worse, as the central bank is effectively borrowing dollars from private banks to defend the lira, yet creating additional contingent liabilities in the process. Borderline levels of reserves and high FX leverage in the banking sector means a currency crisis over the next few months is possible, potentially triggered by political events. The consequences on banks and the economy may be severe. We maintain a very cautious stance, especially on the Lira.

The ugly: Brazil. With President Bolsonaro’s response being a mix of populism and bravado, Brazil’s lockdown has been late and ineffective; contagion numbers remain an outlier vs other countries. In fact, Brazil is one of the few countries where the contagion curve is still exponential, as shown on the left.

A longer crisis means deeper recession and a higher fiscal cost. Brazil will end 2020 with a 6% recession and 95% debt/GDP, up from 65% in 2019. The central bank has already cut rates to the historical low. Without space for fiscal nor monetary policy, part of the output loss will be permanent, as opposed to countries with higher policy leverage. The economic crisis has also brought about political stress, and uncertainty over the remaining tenure of the government is mounting. We remain very cautious on the country, in particular the currency, which is likely to shoulder the burden of the economic adjustment over the next few months.

Conclusions: Identifying the Survivors with Macro and Micro Analysis

The covid crisis has exposed capacity and debt overhangs in several sectors of the old economy. Governments and central banks are expanding their balance sheets to support demand and these sectors. However, not all countries will be able to give support, and not all sectors will be able to consolidate or overcome the crisis.

In this context, we believe credit offers a better risk-return than equities, which especially in the US are pricing record-high multiples. Credit spreads remain above record highs and compensate for a 20-25% 5-year default rate in high yield. In addition, public bailouts are likely to benefit solvency, with restrictions on dividends and shareholder-friendly activity.

That said, credit markets have re-priced too. Safe, investment grade sectors or the obvious winners from the crisis – like tech or telecom firms – are now expensive. The opportunity is in more cyclical sectors and firms which will be able to survive, thanks to management decisions, their competitive position, and public support.

These opportunities can yield substantial returns: for example, Monte Paschi’s LT2 10.5% bonds moved from 70s to par over the past few days, after the EU approved Italy’s plan to support its disposal of non-performing loans.

Our job as investors is to understand which countries, sectors and firms can survive. We believe combining macro policy analysis with micro fundamentals, our unique approach in the Macro Credit Strategy, will be key to generate alpha in the future.

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2020 Algebris Investments. Algebris Investments is the trading name for the Algebris Group.