The vaccine rollout is gathering pace in both the US and UK, with continental Europe running two to three months behind. With fiscal stimulus in overdrive in the US and the EU Recovery Fund about to be deployed, fiscal policy is providing a further impulse for a substantial economic growth recovery.

Market focus is now turning to an acceleration in inflation and a rise in interest rates, particularly at the long end of the yield curve where central banks exert less control. Naturally, investor interest in the financial sector has picked up given the uniquely positive gearing the sector has to higher inflation and interest rates.

In this white paper we aim to clarify some of the important effects these trends will have on the global financial sector:

- How the US will export inflation and push rates up globally

- Why higher rates are good for banks

- Why life insurers are underappreciated winners of a steepening yield curve

How the US will export inflation and push rates up globally

The recently passed $1.9trn stimulus plan in the US comes on the back of a $900bn package in December, and the $2.2trn CARES Act passed in the initial months of the pandemic, in total worth over 23% of 2019 GDP.

No other country globally is using fiscal policy as aggressively in response to the pandemic. However, many countries will feel the impact of the US’ actions via trade. As a result, the US will export the inflationary pressure its fiscal response is generating at home to the rest of the world.

For example, the OECD expects the most recent bill to add 3.8% to US GDP this year. Notably though, it also expects the stimulus to boost the combined GDP of the Euro area, UK, China and Japan by 0.5% as well, reflecting a spillover of US demand.

There is also a high likelihood of an additional $1.5-2trn infrastructure spending bill being passed by the Biden administration this year. That would bring the total fiscal response to over 30% of US GDP – further adding to the US’ export of demand and inflationary pressure globally.

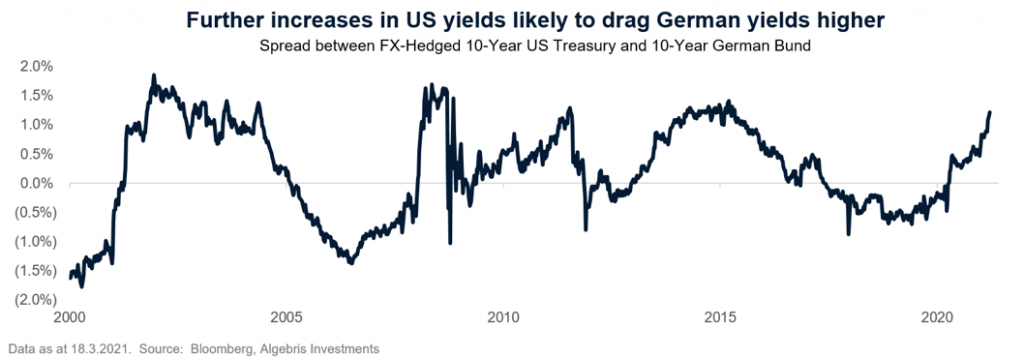

In addition, the size and depth of the US Treasury market makes it an anchor for global interest rates. The recent rise in US Treasury yields has made them particularly attractive for Euro-denominated investors for the first time in years. Since the formation of the Euro, US Treasuries have rarely delivered a higher spread over German Bunds on an FX-hedged basis. This suggests that a further rise in US Treasury yields is likely to pull rates higher in Europe, even if the European recovery does not take place at the same velocity as in the US.

Notably, the equity market appears to be taking its cue from the US bond market more so than the European bond market, which perhaps makes sense given the magnitude of central bank absorption of net supply in Europe relative to the US (i.e., prices are more distorted in Europe than US). We see this in European bank trading, where stocks traded with an R-squared of nearly 60% to the US 10-year Treasury in 2020, versus just 3% to the German 10-year Bund.[1]

Why higher rates are good for banks

Banks are fundamentally engaged in the business of maturity transformation – they take deposits with a short maturity (on-demand in the case of checking/current accounts) and make loans with a longer maturity (up to 30 years in the case of mortgages). The interest rates on deposits and loans are linked to the yield curve – deposits are priced on a spread relative to the short-end, and loans are priced on a spread relative to the long-end.

The spread between the short-end and the long-end – the term premium – is thus the base compensation that banks earn for engaging in maturity transformation. As a result, changes in the term premium impact bank net interest margins (NIM). When the yield curve is steepening and the term premium is expanding, as it has been recently, this results in higher NIMs for banks. However, because this influences pricing on new business only, the impact – while powerful – occurs gradually as old loans mature and new loans are extended.

In the short-term, the composition of a bank’s balance sheet, and specifically, the duration profile of assets and liabilities determine a bank’s earnings sensitivity to movements in interest rates, particularly on the short-end. Most banks benefit from rising short-rates due to several factors:

- Banks typically convert fixed-rate loans to floating to manage their interest rate risk (i.e., most mortgages and corporate loans are swapped to reprice off of short-term rates). In Europe, mortgages are often variable to begin with. As such, when short-rates rise the loan portfolio tends to re-price quicker than its liabilities

- A large portion of banks’ funding mix is comprised of core deposits that are non-interest bearing (checking/current accounts) or reprice less often than movements in market rates

- Banks maintain large cash positions (i.e., dry powder) in anticipation of rising rates and opportunistically deploy cash into higher-yielding securities as rates begin to rise

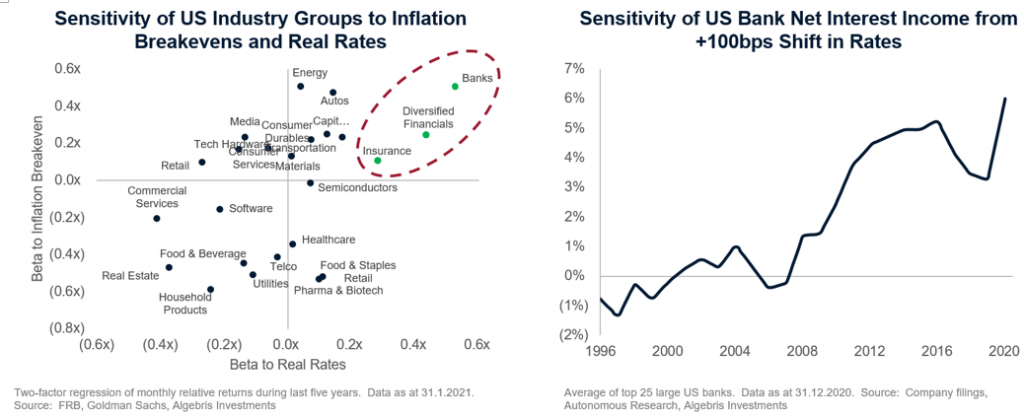

As shown in the chart above, a +100bps parallel shift would be a meaningful driver of US bank NII (+6% on average), but is more pronounced on an earnings basis at over 15%, on average. This dynamic is even stronger in Europe as a +100bps move in interest rates would similarly increase earnings by 20%[1].

Given these earnings sensitivities are averages, we highlight two banks where interest rates represent an even more profound driver of earnings growth:

- Commerzbank: CBK recently provided guidance on the earnings impact of both a parallel shift vs steepening yield curve. Management estimates a 100bps parallel shift would increase NII by 10% in the first year, largely due to short rate development. Meanwhile a 100bps steepening would also increase NII by 10%, but gradually over four years instead. Notably, given the operating leverage, a 10% increase in NII would increase 2022 profits by over 50%.[2]

- Wells Fargo: WFC’s most recent disclosure implies an 18% increase in NII from a 100bps parallel shift, while 100bps steepening at the long end increases NII by 7%. On an earnings basis, a parallel shift would boost consensus 2022 EPS by 38%. Furthermore, given the influx of deposits over the last 12 months from stimulus, WFC is holding excess cash they could opportunistically deploy as rates rise. Assuming they reinvest at a 1% incremental yield, NII would increase another 3%, or 7% on an EPS basis.[3]

Apart from other positive recent developments, the recent steepening in yield curves is starting to drive bank earnings upgrades. We anticipate earnings revisions will continue to be a key underlying driver of stock performance as inflation expectations and interest rates increase, and believe the market may not appreciate the extent of earnings upgrade potential, especially if growth accelerates in 2H21 and 2022.

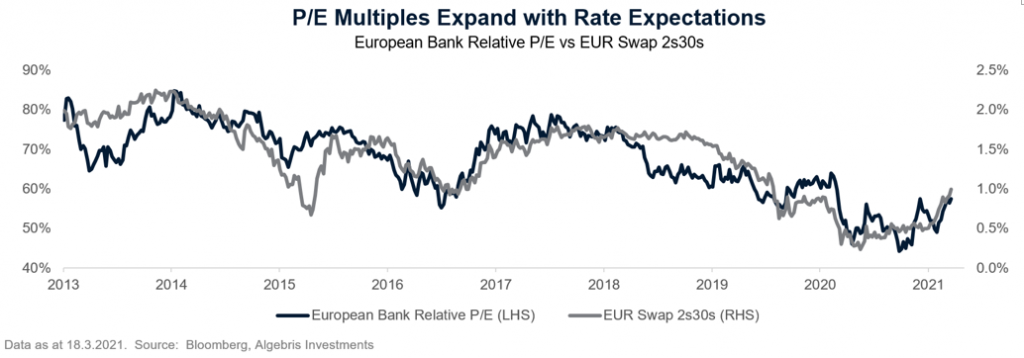

On top of earnings upgrades, there is a strong case for multiple expansion that would provide a “double play” boost to bank stocks. As shown below, there is a significant correlation between European bank relative P/E and yield curve steepening. As we saw in the US in the years leading up to the first post-GFC Fed hike, markets are willing to pay up for rate optionality – even if it is simply a case of rate hike probabilities going from zero (as it is today, in Europe) to something slightly more than zero.

Why life insurers are underappreciated winners of a steepening yield curve

Life insurers are significant beneficiaries of steeper yield curves. Rising yields at the long-end of the curve are good for life insurance companies’ earnings as they benefit from higher yields on new investments, while the cost of funding remains relatively sticky, similar to what we see with banks.

But unlike banks, which are typically more dependent on short rates, insurers are more sensitive to the long-end of the curve, largely because of a significant balance sheet effect. The bulk of life insurers’ liabilities are insurance reserves they take against the long-term obligations embedded in their life insurance contracts with customers, often 30 years or longer in duration. As long-end rates rise, the present-value of these obligations falls, increasing the embedded value of their entire in-force book of business at once. This also results in lower statutory capital requirements, further leveraging the effect as it boosts capital and reduces requirements.

So, if the Fed continues to let the economy run hot by suppressing the short-end, and we see higher inflation expectations and curve steepening as a result, US life insurers stand to benefit more substantially and immediately than banks.

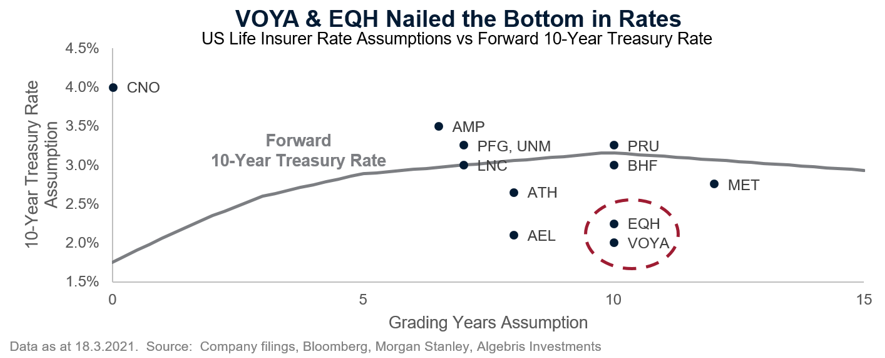

The opposite occurred over the past decade as rates dropped, leading to painful reserve charges which ultimately absorbed significant amounts of industry capital. While some companies still have outdated (and overly aggressive) assumptions, others have “taken their medicine” and rebased their assumptions to a very extended period of low rates, which could well turn out to be excessively conservative. Note, the bond market currently prices in the US 10-year rate to be ~2.7% in 10 years, already well above assumptions of Equitable (EQH) and Voya (VOYA), as shown below.

For an industry that is already sitting on meaningful amounts of excess capital, this could be a significant positive. Notably, the capital benefit of higher rates stands in contrast to large US banks, where unrealized losses on securities (AOCI) caused by higher rates feeds directly into lower capital ratios, meaning higher rates can actually reduce excess capital for banks, depending on the extent to which they hedge.

Conclusion

In a market where investors have crowded into long duration assets just at the time that interest rates appear to have bottomed and inflation expectations are accelerating higher, Financials offer a compelling alternative. While US banks have gone a long way to pricing in the benefit of higher rates and steeper curves, we find European banks and US life insurers still trading at deeply compelling valuations despite having more sensitivity to reflation than US banks. We find it surprising that both groups have significant embedded optionality on higher rates that the market is not yet paying for.

Our core investment philosophy is to find value opportunities with potential catalysts. In our view as we look across markets, there may be no better value than European banks and US life insurance, and no bigger catalyst than a shift towards reflation globally.

[1] Source: Autonomous Research, Bloomberg and Algebris Investments

[2] Source Company disclosures, Algebris Investments

[3] Source: Company disclosures, Algebris Investments

This document is issued by Algebris (UK) Limited. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris (UK) Limited.

Algebris (UK) Limited is authorised and Regulated in the UK by the Financial Conduct Authority. The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Under no circumstances should any part of this document be construed as an offering or solicitation of any offer of any fund managed by Algebris (UK) Limited. Any investment in the products referred to in this document should only be made on the basis of the relevant prospectus. This information does not constitute Investment Research, nor a Research Recommendation. Algebris (UK) Limited is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris (UK) Limited , its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is for private circulation to professional investors only.

© 2021 Algebris (UK) Limited. All Rights Reserved. 4th Floor, 1 St James’s Market, SW1Y 4AH.