Bearish Lows, Bullish Highs: A week of extremes

The first week of April was characterised by markets on a rollercoaster. On Monday 7th, the S&P 500 dipped 0.2%, nearing bear market territory. Treasury yields rebounded after an early drop, while the VIX hit 60 intraday—reflecting intense volatility. Traders were pricing in four rate cuts from the Fed. Meanwhile, the dollar rose, and gold slipped.

Tuesday 8th saw the S&P 500 fall 1.6%, coming close to officially entering a bear market. Trading volume surged to 23 billion shares as long-term yields climbed. The dollar, oil, and Bitcoin all declined, signalling broad market weakness.

A dramatic reversal came on Wednesday 9th, when the S&P 500 soared 9.5%—its biggest single-day gain since the financial crisis—while the Nasdaq 100 jumped 12%. A record 30 billion shares were traded. Two-year yields briefly topped 4%, and bets on Fed cuts were reduced. Goldman Sachs dropped its call for a U.S. recession.

However, optimism quickly faded. On Thursday 10th, the S&P 500 fell 3.5%. The dollar had its worst day since 2022, and a strong 30-year Treasury auction failed to lift market sentiment. Oil prices dropped again, while gold rebounded.

Friday 11th ended the week on a positive note. The S&P 500 rose nearly 2%, capping its best weekly gain since 2023. While 30-year yields declined, they remained elevated. The dollar weakened, and both the euro and Bitcoin advanced..

Made in Asia, Paid in America: How tariffs could kick U.S. jobs to the curb

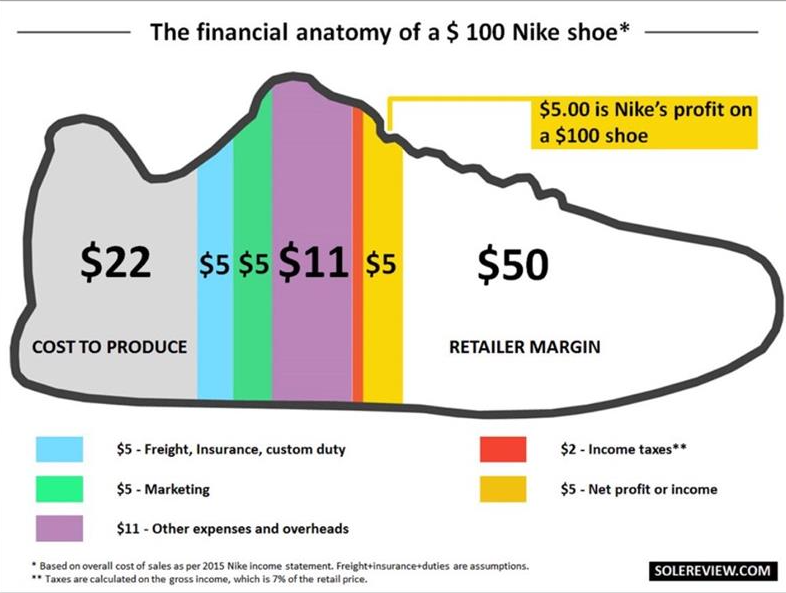

Back in 2016, Sole Review analysed Nike’s income statement using a hypothetical $100 shoe. Of that $100, manufacturing costs—including freight—totalled $22, plus taxes and marketing. Nike would then sell the shoe to retailers for $50.

Adding a $26 tariff at the port doesn’t necessarily mean the final price would increase by $26. However, the real concern is that it could spark a broader rise in costs, potentially making the shoe significantly more expensive for consumers.

Despite being manufactured in Asia, these shoes still support U.S. jobs. Why? Because Americans can still purchase them at local stores, employing salespeople, store managers, and many others. Moreover, Nike’s U.S.-based teams—designers, marketers, and brand strategists—are an integral part of the value chain.

If Nike pays $25 to produce each pair, the factory might keep about half—roughly $12.50. From that, only a fraction goes directly to the workers. Assuming ethical labour standards, these wages—although modest—remain part of the broader economic equation.

This highlights the transition to a post-industrial economy. The U.S. and other developed nations have increasingly focused on higher-value roles like design, branding, and marketing, while outsourcing manufacturing to lower-cost countries. This model allows companies to offer affordable products to consumers.

Ironically, overseas manufacturing can lead to more jobs at home. If political or economic decisions push prices too high—say, to $220 per pair—consumer demand could fall, potentially resulting in job losses across retail and design sectors in the U.S.

Guns before butter: Europe’s strategic pivot

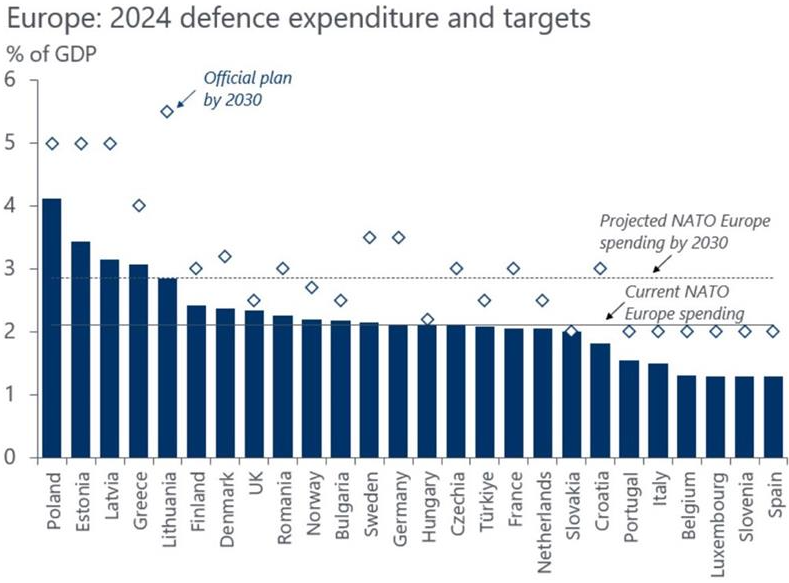

European rearmament is accelerating, marking a structural shift in defence priorities across the continent. NATO’s European members are projected to raise military spending to 3% of GDP by 2030, up from 2.1% in 2024. This is a sharp contrast to the average of just 1.2% during the 2010s, underscoring the pace of change.

The increase is being driven by heightened geopolitical tensions and a renewed emphasis on strategic autonomy. As defence budgets expand, the implications for industrial policy, fiscal balances, and Europe’s broader security architecture are profound.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.