Equities heat up over the summer

Global equity investors enjoyed a strong summer, with markets moving materially higher since our last update two months ago. The S&P 500 posted a +13% year-to-date gain in dollar terms, almost entirely driven by earnings growth. However, currency effects continued to weigh on foreign investors, leaving euro-based returns close to breakeven.

In Europe, markets also advanced, with a +13% return year-to-date. Gains came mainly from multiple expansion off very depressed levels, only partially offset by sluggish earnings growth. Italy was among the stand out performers with PE multiple expanding over 30% YTD and thus anticipating cyclical recovery in the industrial space which should bring EPS uplift starting from 2026. Asia also accelerated meaningfully over the summer. Since mid-July, Japan and China have added +14% and +3% respectively, supported by a clear rebound in earnings momentum.

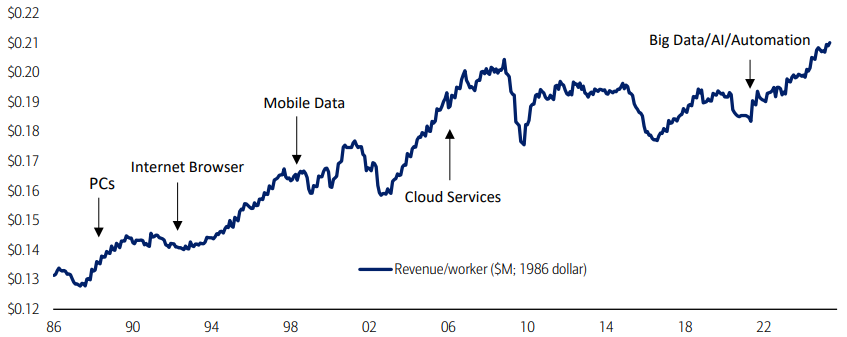

A productivity-led bull

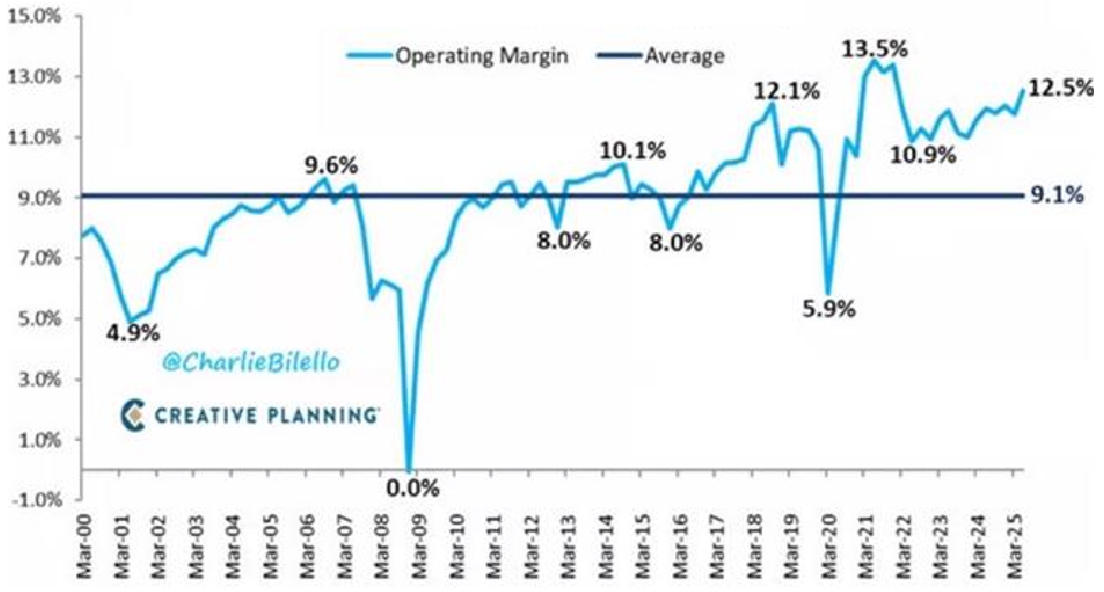

The U.S. market’s strength has been fundamentally about earnings, and earnings have been about margins. S&P 500 operating margins climbed to roughly 12.5% in Q2, the highest since 2021 and well above the ~9% long-run average, which mechanically lifts EPS for a given dollar of sales. While pricing power, cost discipline, and a shift toward asset-light, higher-return models helped, the bigger driver is a productivity upcycle—real revenue per worker for S&P 500 companies has pushed to record highs as years of investment in cloud, data, automation, and now AI let firms do more with the same (or fewer) heads. That combination creates powerful operating leverage: modest top-line growth converts into outsized profit gains, supporting equity prices even without a macro re-acceleration. As long as productivity growth runs at or above wage inflation, margins can hold or expand—key to the market’s advance.

Apple’s Anti-Inflation Playbook

Apple froze the sticker price on the base iPhone 17 ($799 with 256GB) and kept the Pro at $1,099 (also 256GB), so there’s no obvious tariff pass-through on iPhones themselves to end customers —helped by the fact that smartphones were explicitly spared in the latest tariff rounds. The macro backdrop, though, is inflationary at the margin: Boston Fed work suggests broad tariff packages could add as much as ~2.2pp to core inflation (first-round effects). Apple’s defence is classic: push mix and storage tiers up, lean on record-high Services, and keep shifting assembly out of China—now roughly one in five iPhones are made in India—so corporate gross margin stays lofty (46.5% last quarter) even as tariffs raise noise in the cost base.

From Waste to Wealth: Scaling Textile-to-Textile Recycling

Luxury sector has struggled over the past two years, with organic growth falling well below expectations. The slowdown in China, inflationary pressures, and arguably a lack of true innovation have weighed on the sector. In this context, luxury brands must find new ways to reinvent themselves — and textile-to-textile recycling could offer just such an angle. Fashion is on the verge of a transformation where old clothes can genuinely become new again. After years of relying mainly on recycled plastic bottles, textile-to-textile recycling is finally reaching industrial scale. Factories capable of processing tens of thousands of tons of garments are emerging, turning waste into a valuable resource and redefining the future of fashion. The opportunity is vast: millions of tons of clothing end up in landfill each year, yet less than 1% of global fibres come from recycled textiles. Breakthrough technologies — from AI-powered fibre scanning to hydrothermal and chemical processes — are enabling the separation and regeneration of cotton and polyester at scale. Regulation is also pushing the shift, with the EU and U.S. states requiring producers to fund and manage clothing recycling. Momentum is building: established brands are already sourcing fabrics from new recyclers, and dozens of plants are set to expand capacity globally. For investors, this signals the rise of a structurally growing industry, driven by policy, innovation, and consumer demand. Textile recycling is not just a sustainability story — it is shaping up to be the next growth frontier in fashion.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.