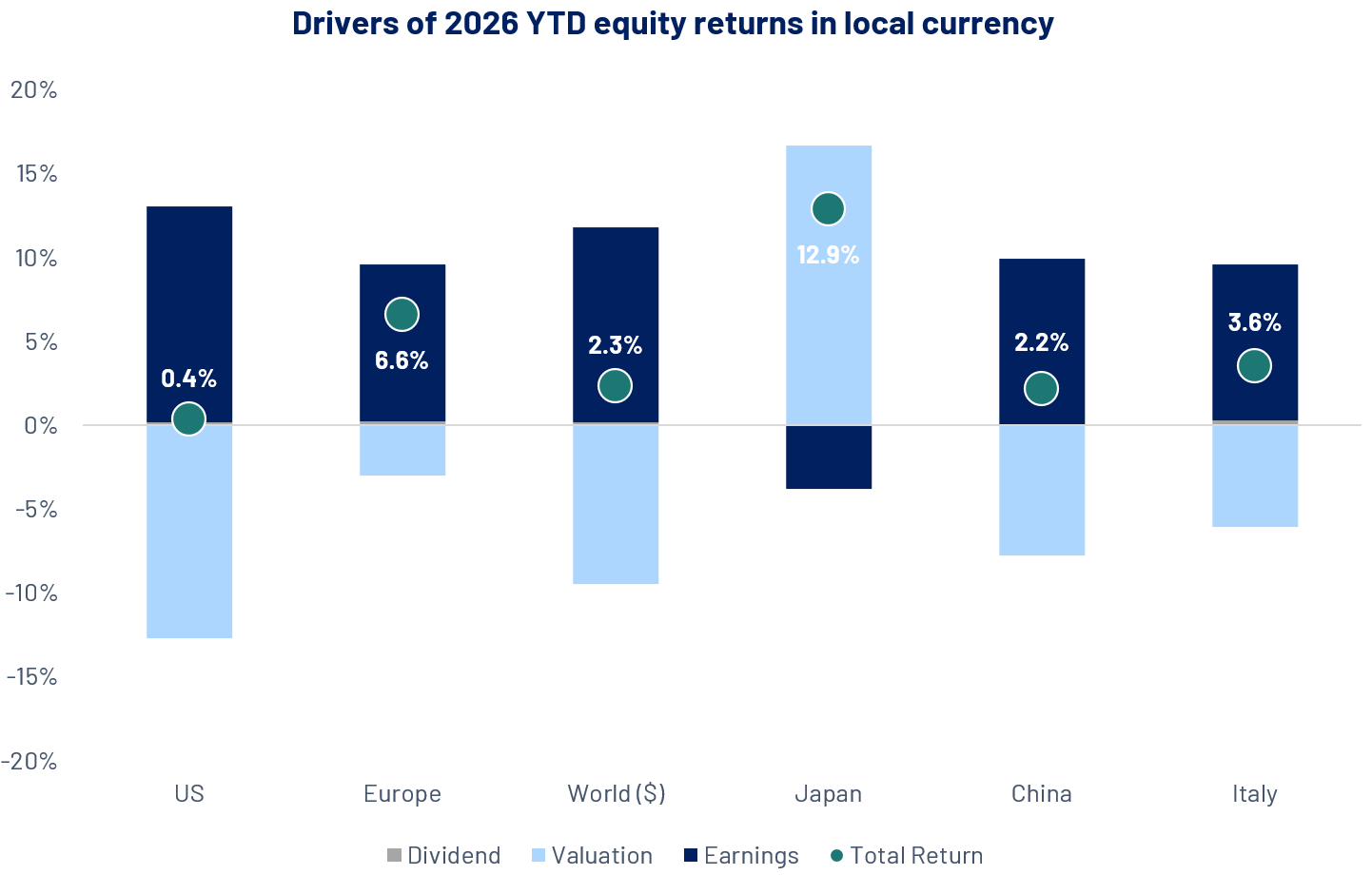

A positive start to 2026

Global equities began 2026 on an upbeat note, with the MSCI World Index rising 2.3% YTD in USD terms. This performance was primarily driven by a global recovery in earnings, which was only partially offset by a contraction in valuations. Mirroring the trend seen in 2025, the US remained a laggard as global capital reallocation continued. We are seeing some outflows from US markets in favour of strong inflows into Europe, Latin America, and select Asian countries, even as underlying US earnings growth remains robust during the current reporting season. European equities, which surged over 20% in 2025 as valuations rebounded from historical lows, are now seeing a fundamental recovery in earnings, a trend that is also reflected in the Italian market. In Asia, Japan and Korea have emerged as standout performers. The Japanese index was bolstered by the recent re-election of Prime Minister Sanae Takaichi and her administration’s commitment to an aggressive fiscal expansion plan. Meanwhile, Korea’s tech-heavy index continues to benefit from the ongoing buildout of US data centres and the global demand for AI infrastructure.

Source: Algebris Investments, Bloomberg Finance L.P, data as of 31/12/2025. Performances in local currencies.

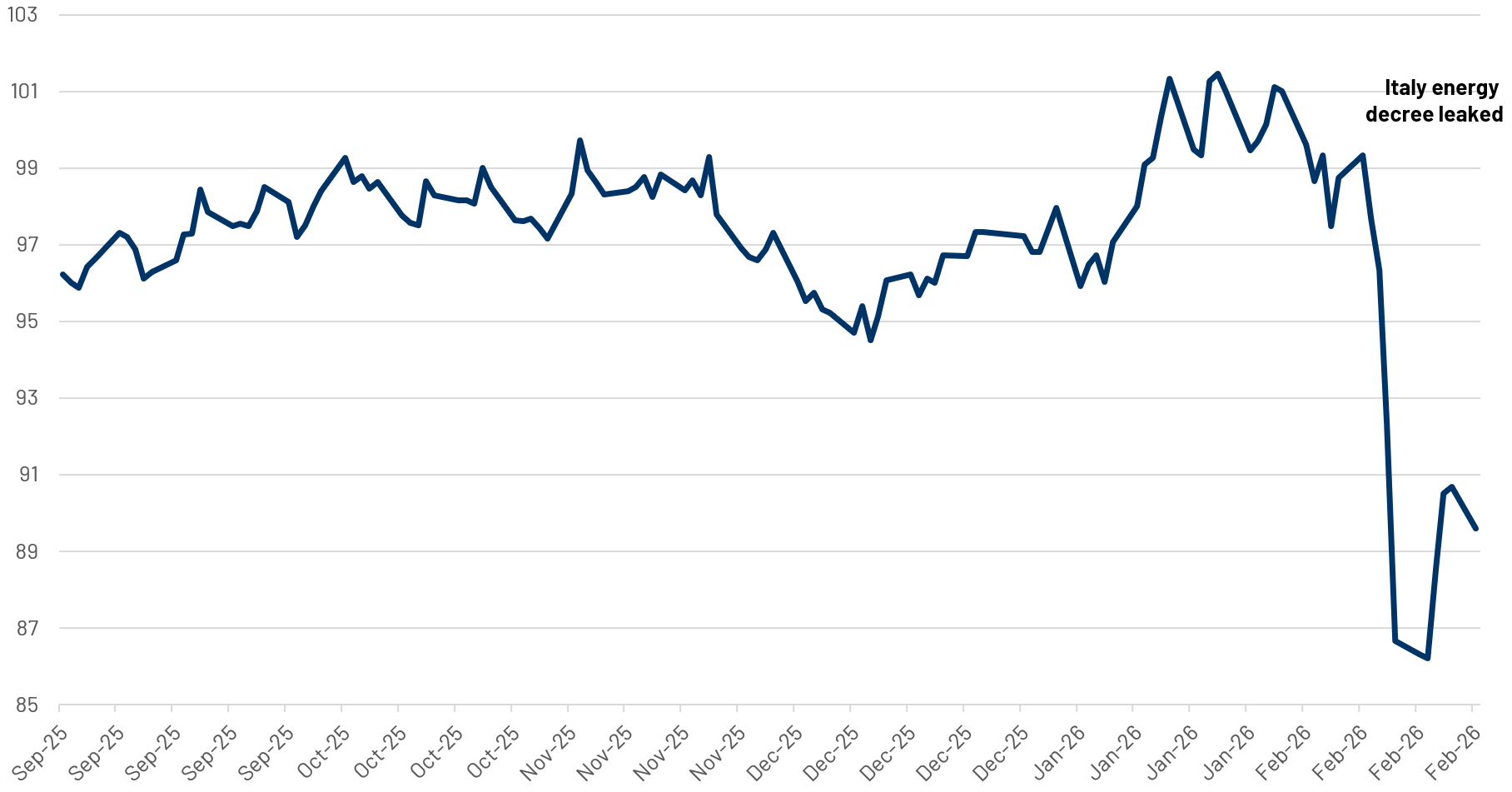

A structural shift in italian energy prices?

The newly approved Energy Decree introduces a temporary 2% tax surcharge on energy companies (2026–27) and signals a potential structural reform of the wholesale power market, including the possible removal of carbon (ETS) costs from electricity bills and compensation mechanisms for gas-fired plants (subject to EU approval). Italian year-ahead power prices have declined sharply in recent sessions as markets reprice regulatory risk and the prospect of a partial decoupling of carbon costs from marginal pricing. While the measures aim to deliver meaningful consumer cost relief, they could structurally lower clearing prices and compress margins for utilities and renewable generators, including regulated players (e.g., Terna, Snam), integrated utilities (e.g., Enel, A2A, Edison) and renewable operators (e.g., ERG), thereby increasing earnings sensitivity to policy outcomes and adding regulatory complexity across the Italian power sector.

Source: EEE, European Energy Exchange, Bloomberg. Data as of 23/02/2026

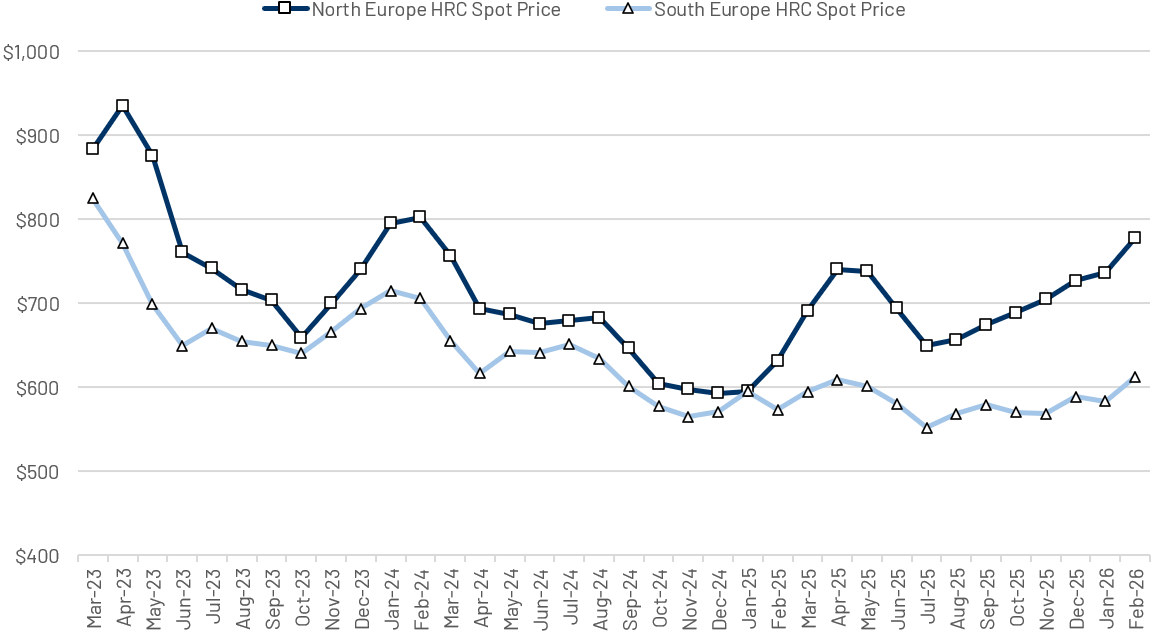

Make EU steel great again!

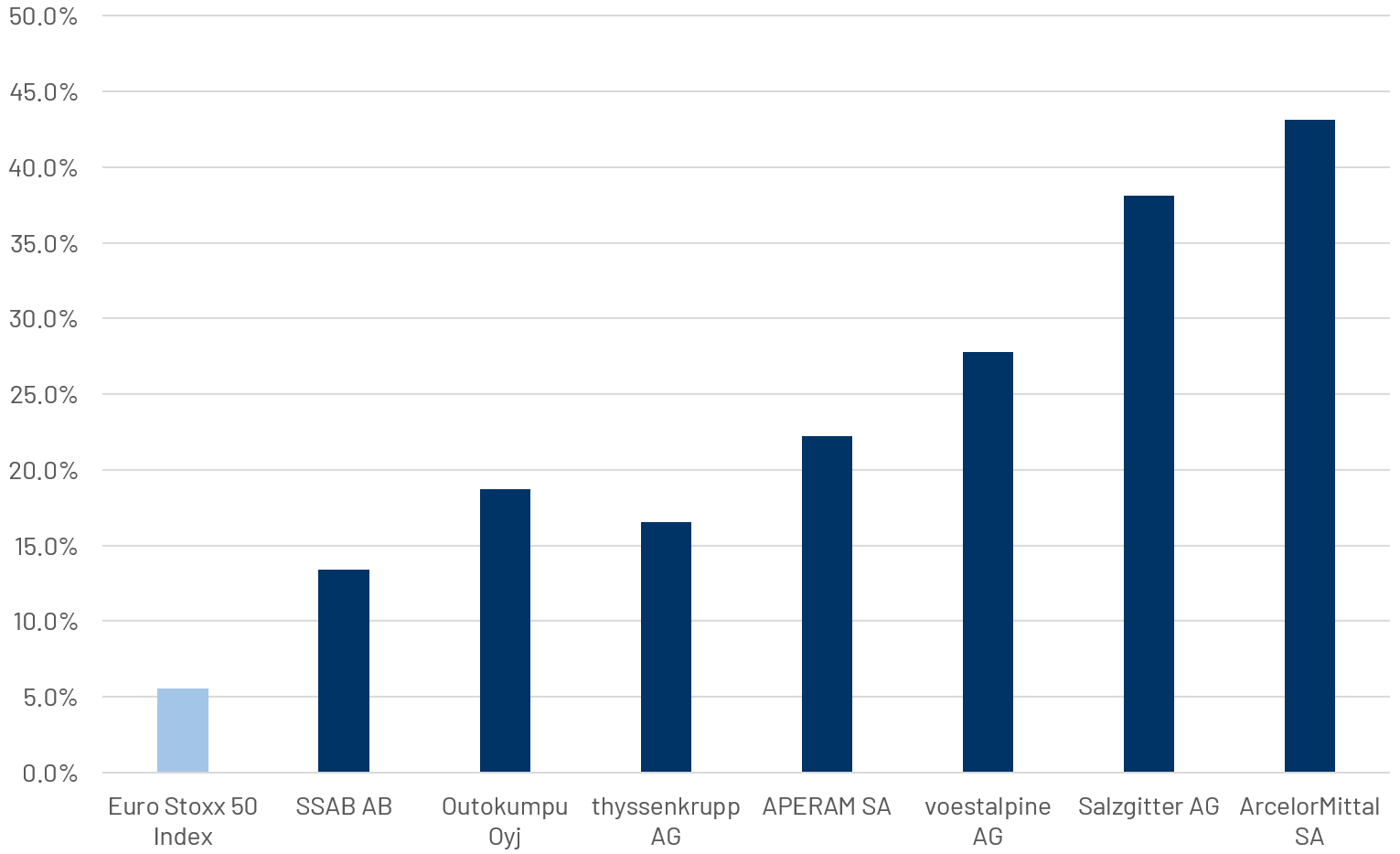

Europe’s steel industry has struggled in recent years due to weak demand, high energy costs, and rising import penetration. However, a recent shift in EU policy could improve the sector’s outlook. In October 2025, the European Commission proposed a much tougher trade regime, halving import quotas and doubling out-of-quota tariffs to 50%. At the same time, the roll-out of the Carbon Border Adjustment Mechanism (CBAM) is expected to increase the effective cost of non-EU steel, encouraging local sourcing and supporting higher European benchmark prices. This comes as the US, under President Donald Trump’s second term, has also strengthened protectionist measures to support its domestic steel industry, with tariffs on steel import up to 50%. The new European framework is expected to come into force in mid-2026 and could significantly reduce steel import penetration in Europe (which was close to 30% in 2025) while lifting prices. Markets have already begun to reflect this scenario: European hot-rolled coil prices are up around 11% year-to-date, and major European steelmakers stock prices are all up double-digit since the beginning of 2026, outperforming the Euro Stoxx 50 index.

Source: Bloomberg Finance L.P, data as of 24/02/2026. Performances in local currencies.

Source: Bloomberg Finance L.P, data as of 24/02/2026. Performances in local currencies.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.