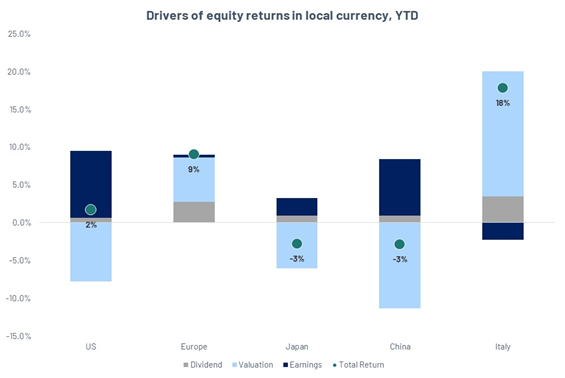

FX Impact and Regional Divergences Shape YTD Equity Performance

As of June 20, 2025, the S&P 500 posted a +2% year-to-date return. Despite robust EPS growth, the index faced valuation headwinds, with multiples contracting amid heightened uncertainty, in our view.

For European investors, however, the S&P 500 showed a -8% YTD return in euro terms, driven by significant USD depreciation against the euro in the first half of 2025. This underscores the material impact of FX movements on cross-border investment returns.

In contrast, European equities delivered strong performance, with the region up +9% YTD. Within Europe, Italy stood out, achieving an impressive +18% YTD total return in the same timeframe.

Strait of Hormuz: The Geopolitical Trigger No One Can Ignore

Amid rising tensions in the Middle East, the risk of Iran closing the Strait of Hormuz—a key chokepoint through which 30% of global seaborne oil flows—has re-entered market conversations. A blockade would instantly disrupt global supply chains, ignite a spike in crude oil prices, and amplify geopolitical risk premiums across all asset classes. But this isn’t just about oil. It’s about what happens next to equities.

Following the recent escalation, oil prices have already surged—from below $60 to around $75 per barrel in just a few days—underscoring how sensitive markets are to this risk.

Historically, when oil prices skyrocket suddenly, the immediate reaction on equity markets tends to be negative, especially for indices in oil-importing economies (e.g., Eurozone, Japan, India). Higher energy costs feed into inflation, erode corporate margins, and tighten consumer spending—all of which put downward pressure on valuations. Central banks may be forced to maintain or resume hawkish stances, further stressing equity multiples.

However, not all sectors react the same. Energy stocks (especially upstream oil producers and integrated majors) often outperform, acting as a rare hedge. Defence, shipping, and inflation-sensitive value names may also find support. Conversely, industrials, discretionary, and transport-heavy sectors tend to underperform.

In short, an oil price shock is rarely just a commodity story—it’s a macro regime shift with ripple effects across global equity positioning.

While Ferrari Waits, China Overtakes

Last week, Ferrari announced another delay in the launch of its first fully electric vehicle, underscoring the complexities that even the most prestigious automakers face in adapting to the electric transition—particularly within the luxury performance segment.

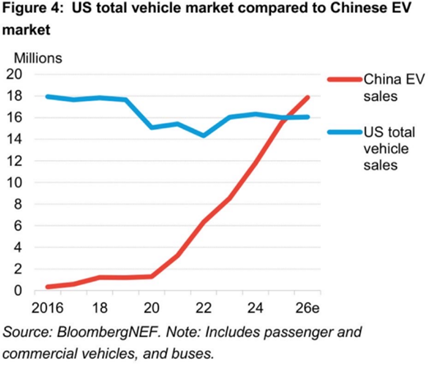

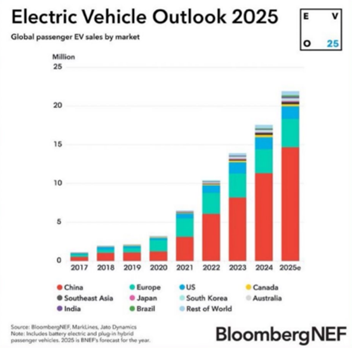

In China, EV sales are expected to reach approximately 14 million units in 2025, making up more than 40% of all new car sales. By 2026, EV sales in China alone are projected to exceed the total volume of all vehicle sales—of every type—across the United States.

This contrast highlights a growing strategic divide. In the U.S. and EU, the EV market faces headwinds from lagging infrastructure and supply chain, higher price tags (while in China EVs are cheaper vs ICE across all categories, in the EU and USA EVs come at hefty premiums vs ICE), regulatory uncertainty, and wavering consumer demand, particularly as subsidies are phased out or challenged politically. Meanwhile, Chinese manufacturers such as BYD, Nio, and XPeng are scaling rapidly, supported by strong domestic demand, cost-efficient supply chains, and aggressive innovation cycles. These firms are no longer just dominating their home market—they are increasingly targeting global expansion, often with EVs priced well below Western counterparts.

As European and American automakers contend with sluggish uptake, rising costs, and increasing pressure from investors to meet sustainability targets, the specter of Chinese EV competition looms large. The upcoming years may not just define the trajectory of EV adoption, but also reshape global automotive leadership.

Don’t Bet Against Progress

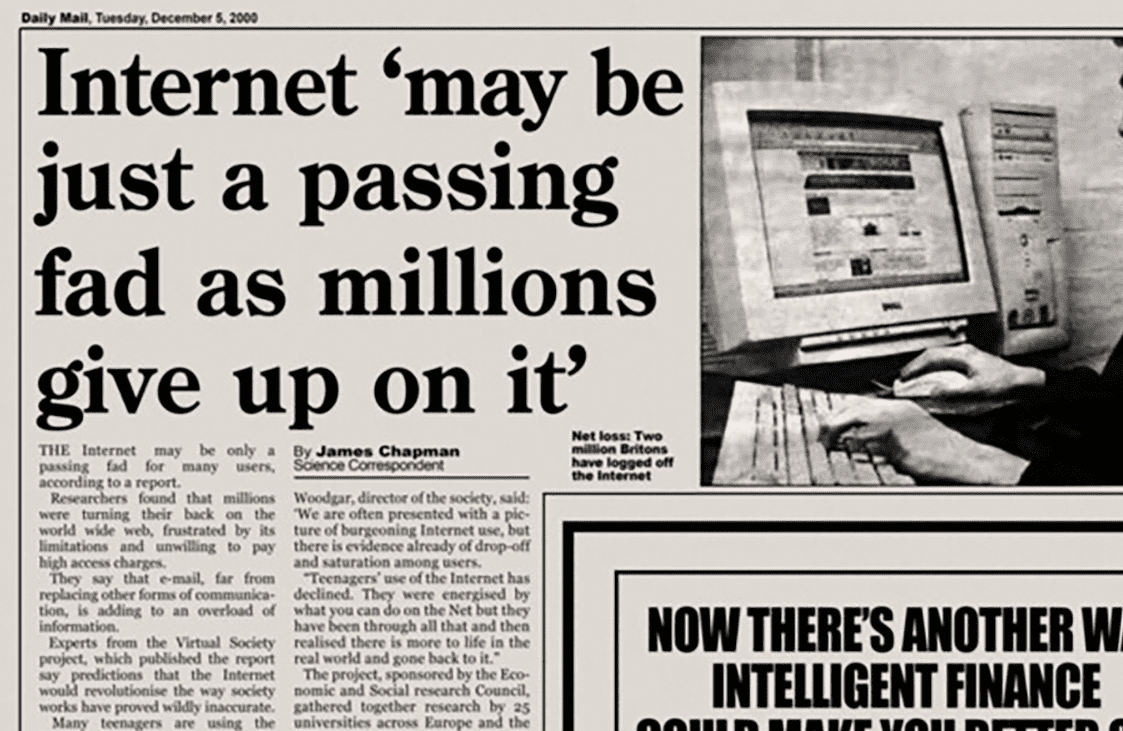

Back in December 2000, the Daily Mail famously declared: “Internet may be just a passing fad as millions give up on it.” We all know how that ended—digital innovation reshaped the world and equity markets. Today, similar doubts hover around artificial intelligence. Yet AI adoption is already driving massive investment: global spending on AI datacentres is expected to exceed $200 billion by 2027, with power demand from AI workloads projected to grow by 160%+ by 2030. Just like the internet, this isn’t a fad—it’s the infrastructure of the future. Historical patterns suggest that innovation should not be underestimated.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.