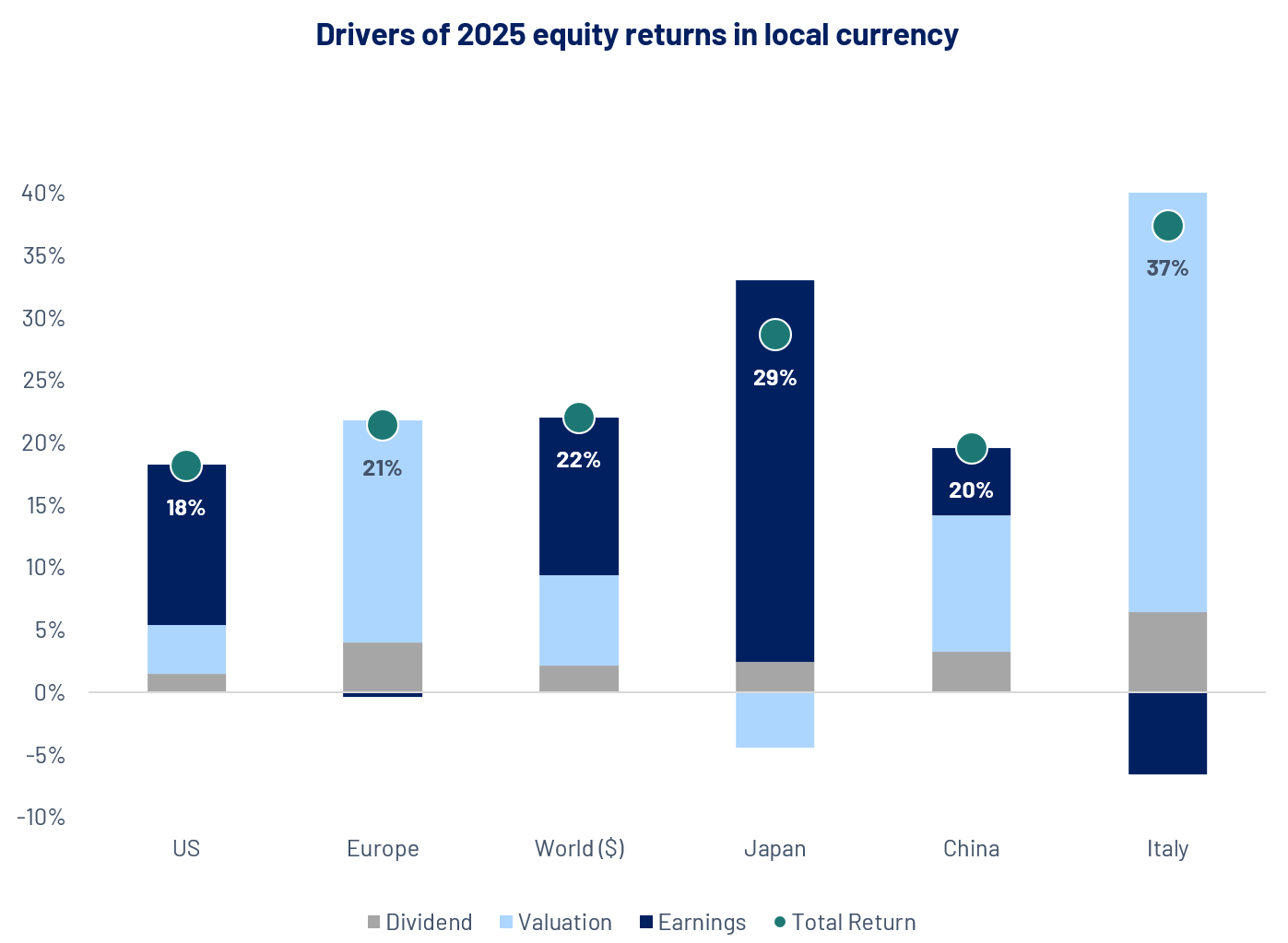

Annual review – A strong 2025 for global equities

Global equities navigated periodic volatility in 2025 but finished strongly, with the MSCI World up ~22% in USD, marking the third consecutive year of double-digit returns. For European investors, weakness in the US dollar versus the euro partially offset headline performance.

The United States, now representing more than 70% of the index, lagged ex-US markets while still delivering returns of around 18% over the year. Returns were primarily earnings-driven (S&P 500 EPS ~+13%) and led by technology, with improving expectations for Federal Reserve easing supporting broader participation later in the year.

In Europe, equities delivered solid gains and outperformed early, despite muted earnings growth. Performance was driven largely by multiple expansion from depressed starting levels, supported by better sentiment, renewed inflows, and defence/industrial exposure as markets began to discount a 2026 earnings recovery.

Source: Algebris Investments, Bloomberg Finance L.P, data as of 31/12/2025. Performances in local currencies.

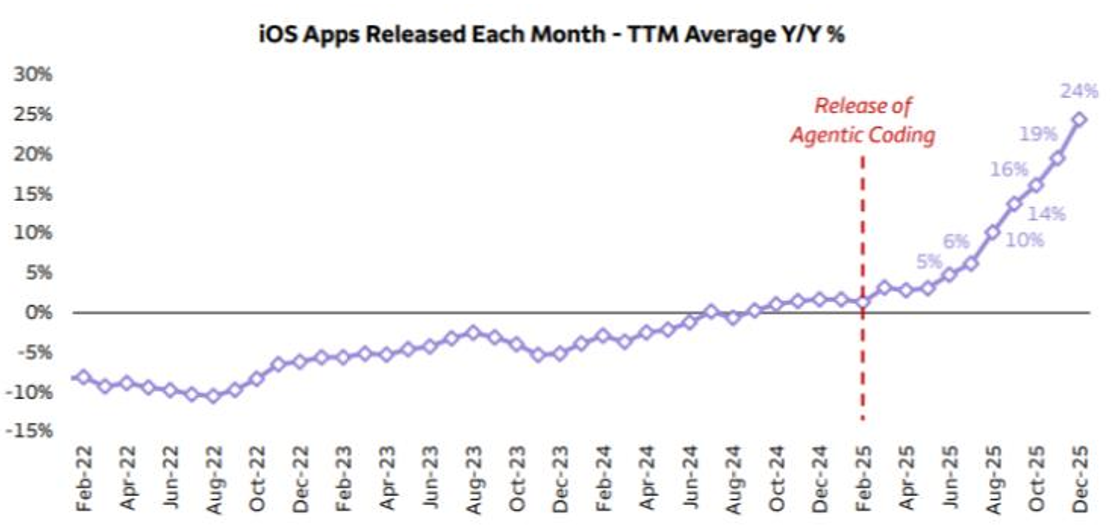

Death of software?

A “death of software” narrative has emerged, suggesting generative AI tools could automate coding and disrupt traditional Software-as-a-Service models, leading to obsolescence for many software firms.

Historically, software development was expensive and complex, which protected incumbents. AI has materially lowered these barriers, effectively commoditising coding and enabling small teams to build “good enough” versions of specialised tools that previously required dozens of engineers. For instance, AI model startup Anthropic has claimed they built their latest product, Claude Cowork, with the help of AI in just 10 days.

However, this trend might be exaggerated. AI won’t kill software but force vendors to adapt, integrating AI to enhance rather than replace their offerings. The winners are likely to be software platforms with durable distribution, proprietary data, deep integrations, and clear “AI-to-workflow” productization. Conversely, narrow point solutions are more vulnerable where AI-native substitutes are “good enough,” especially if pricing has outpaced perceived value.

Software is therefore unlikely to disappear, but the era of rent-seeking, in which companies could command high prices for basic functionality, is coming to an end.

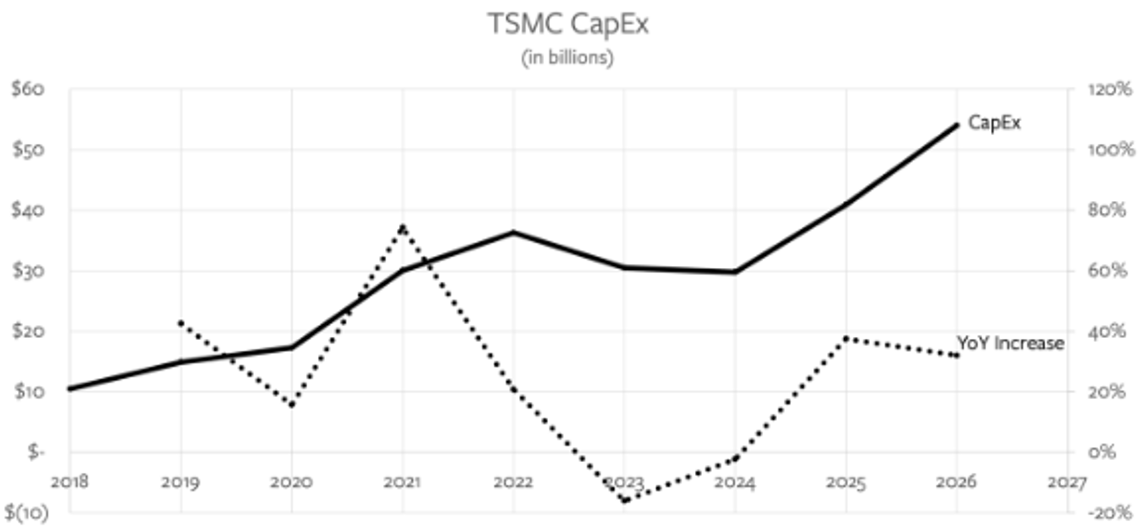

Booming hardware – Semi-capex tsunami in January

January 2026 kicked off with a bang in global equity markets, but one niche lead the move: semiconductor capital equipment, (“semi capex”) stocks. These companies supply high-tech tools used by chipmakers to build the world’s most advanced semiconductors. Names like ASML Holding, Applied Materials, ASM International, and Italy’s Technoprobe surged on relentless AI-driven demand. Picture a chain reaction: AI’s hunger for faster chips fuels massive factory expansions, funneling billions to equipment makers. Here’s why the rally ignited, backed by numbers, and what it means for investors.

The catalyst was TSMC’s record Q4 2025 earnings release on 15th January 2026. As the world’s largest contract chip foundry, producing cutting-edge silicon for Nvidia, Apple, and AMD, TSMC is the industry’s heartbeat. The Company reported record profits and forecast 30% USD revenue growth for 2026. The highlight? Capex surging to $52-56 billion in 2026, from ~$40 billion in 2025. This means factories scaling like high-tech kitchens for a restaurant boom. Exploding AI and high-performance computing demand requires more fabs, and TSMC’s spending signaled confidence in endless chip appetite, with ripple effects to suppliers.

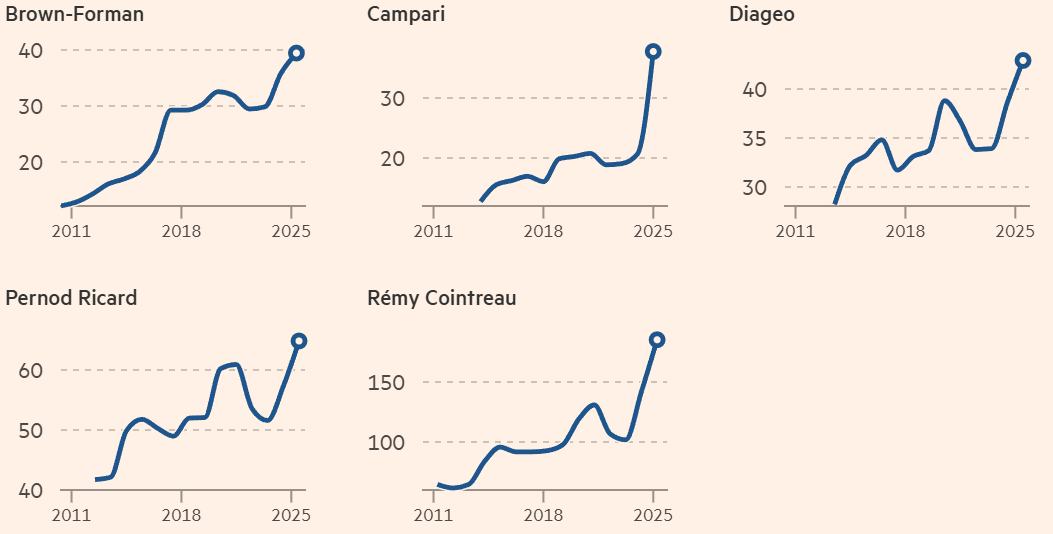

Spirits – Short-term cycle, long-term brand assets

The industry is digesting a post-Covid overbuild, with large producers holding a record ~$22bn of ageing inventory, prompting temporary production pauses and targeted pricing actions to clear warehouses while protecting brand equity.

While the near-term dynamics resemble a classic destocking cycle, medium term the outlook is more mixed. Some moderation appears structural, reflecting lower consumption among Gen Z and younger Millennials, though demand also remains sensitive to macro conditions. Historically, premium brands and consumption occasions have proven more resilient than overall volumes.

Demand could re-accelerate as macro conditions ease, with upside from premiumisation and sustained brand awareness, while disciplined production cuts and efforts to avoid deep discounting help protect future pricing power.

Source: Source: Financial Times, January 18th 2026

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.