UK – Fiscal drives you higher

Last week, UK rates were one of the drivers of duration selloff, with 30-year yields climbing to their highest levels since 1998. The move was amplified by headlines suggesting Starmer’s reshuffle could sideline Rachel Reeves. At it’s core, the issue is fiscal. Refinancing costs are rising and with them the pressure for greater fiscal effort. The November Budget will be crucial—higher taxation now looks more politically feasible than deep spending cuts. On Wednesday, the cancellation of a 30-year gilt auction provided some relief at the long end. While yields may look stretched, they are justified by the UK’s deteriorating fiscal outlook, with a material risk of further deterioration.

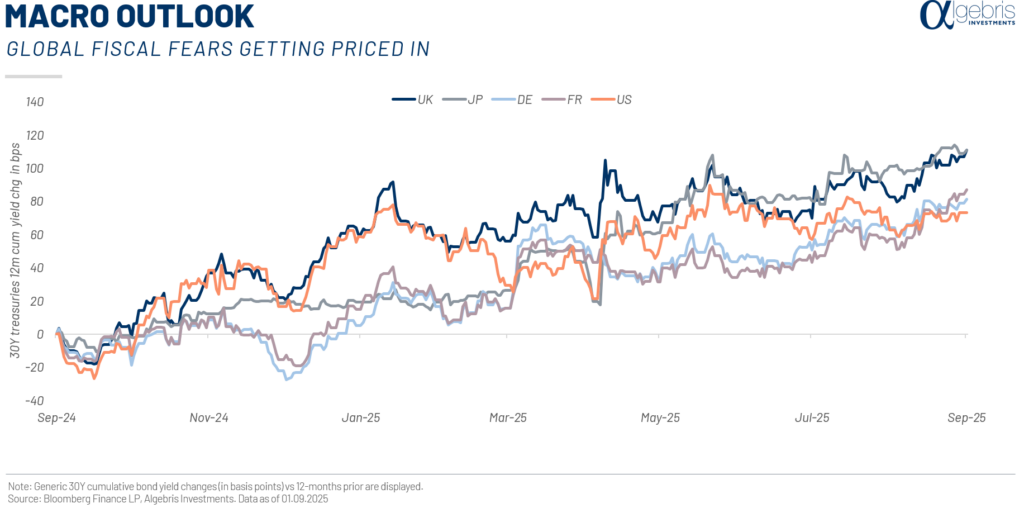

Global Rates – Fiscal fears getting priced in

As has been seen on several occasions in the UK recently, whenever fiscal fears come to the surface, the selloff in long-end rates becomes especially pronounced. The fiscal theme is now driving a repricing of long-term yields across major global economies, with similar dynamics playing out across currency markets. Large budget deficits are being maintained against a backdrop of solid growth but poor inflation dynamics. The UK is emblematic, but this repricing is a global phenomenon—and with US rates setting the tone, the upward drift in yields still appear to have further room to run.

ECB – Sticking to script

At its September meeting, the ECB is expected to leave policy unchanged, with recent commentary making clear that the bar for further cuts is very high. Incoming data offered few surprises, leaving forecasts largely unchanged. While markets may be priced for perfection in risk, the eurozone economy is far from showing strong momentum. We still see room for rate cuts over the next 2-3 quarters, even if the ECB remains reluctant to move quickly.

Algebris Investments’ Global Credit Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.