Middle East tensions trigger global market sell-off

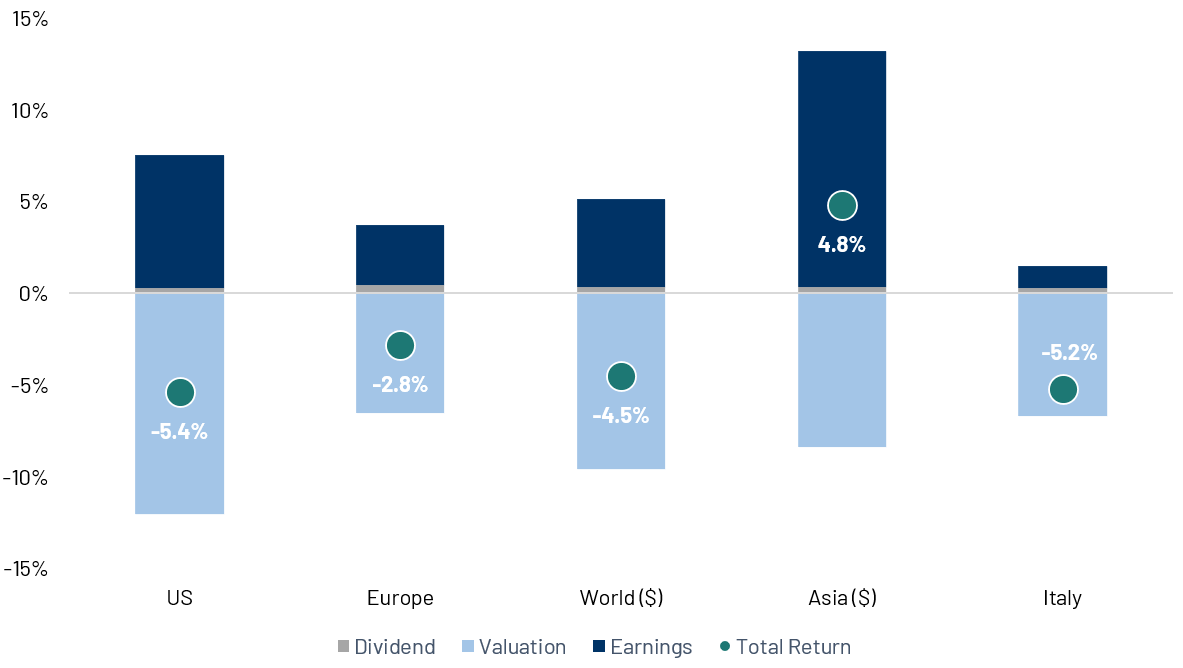

After a relatively strong start to the year, during which Asian markets and Europe outperformed a broadly flat US market, global equities came under pressure following the coordinated military action launched by the US and Israel against Iran on 28th February. Iran’s retaliation, which targeted Israel and several Gulf countries, included attacks on energy production facilities and effectively disrupted tanker traffic through the Strait of Hormuz, temporarily cutting off roughly 20% of global oil and gas supply. As a result, oil prices surged above $100 per barrel and markets sold off sharply. The US, benefiting from its relative energy independence, proved more resilient despite posting negative returns. By contrast, Asia and Europe were hit harder: Asian economies remain heavily exposed to trade flows through Hormuz, while Europe continues to rely on gas supplies from the region. Consequently, Asia surrendered much of its year-to-date outperformance, although it remained in positive territory, while both the US and Europe moved into negative territory for the year, down by mid-single digits.

Source: Algebris Investments, Bloomberg Finance L.P, data as of 20/03/2026. Performances in local currencies.

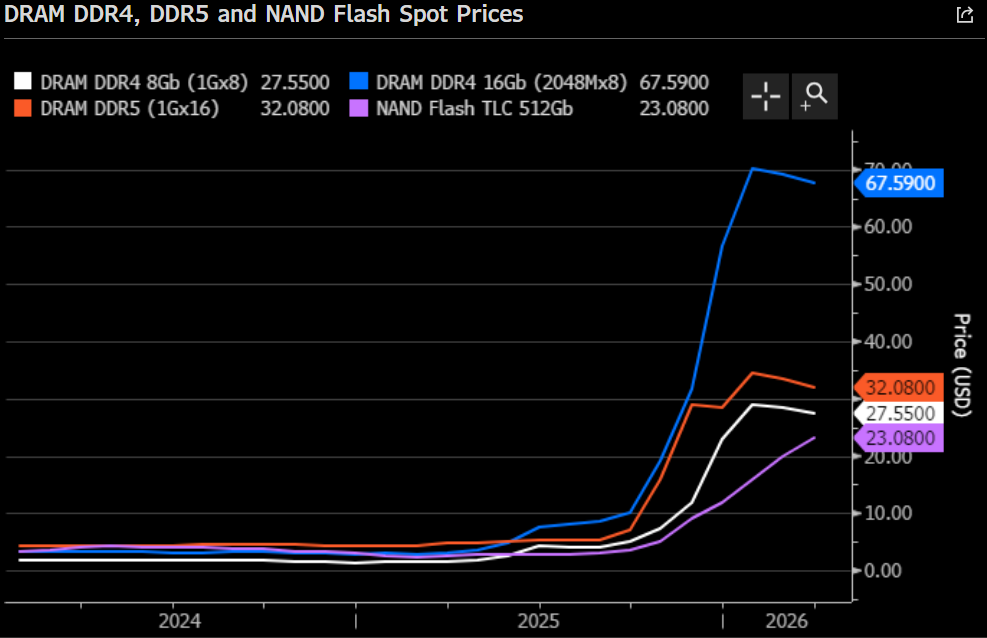

RAMmageddon shakes the smartphones industry

The smartphone industry is currently navigating a significant challenge as memory chip prices continue to surge. Driven by AI demand, leading memory chip producers, such as SanDisk and Samsung, have diverted much of their manufacturing capacity toward AI memory chips, leaving the traditional consumer electronics sector with reduced availability. Consequently, procurement costs for mobile memory have risen sharply, with leading DRAM and NAND prices increasing significantly since mid-2025. This is expected to have severe impacts on the smartphone and consumer electronics industries. According to IDC Research, the smartphone market could shrink by almost 13% in 2026. Manufacturers are adapting by abandoning unprofitable budget models and encouraging consumers toward premium devices. Major brands are already planning their largest collective price hikes in nearly five years, signalling that the era of the cheap smartphone has likely come to an end.

Source: Bloomberg Finance L.P, data as of 23/03/2026.

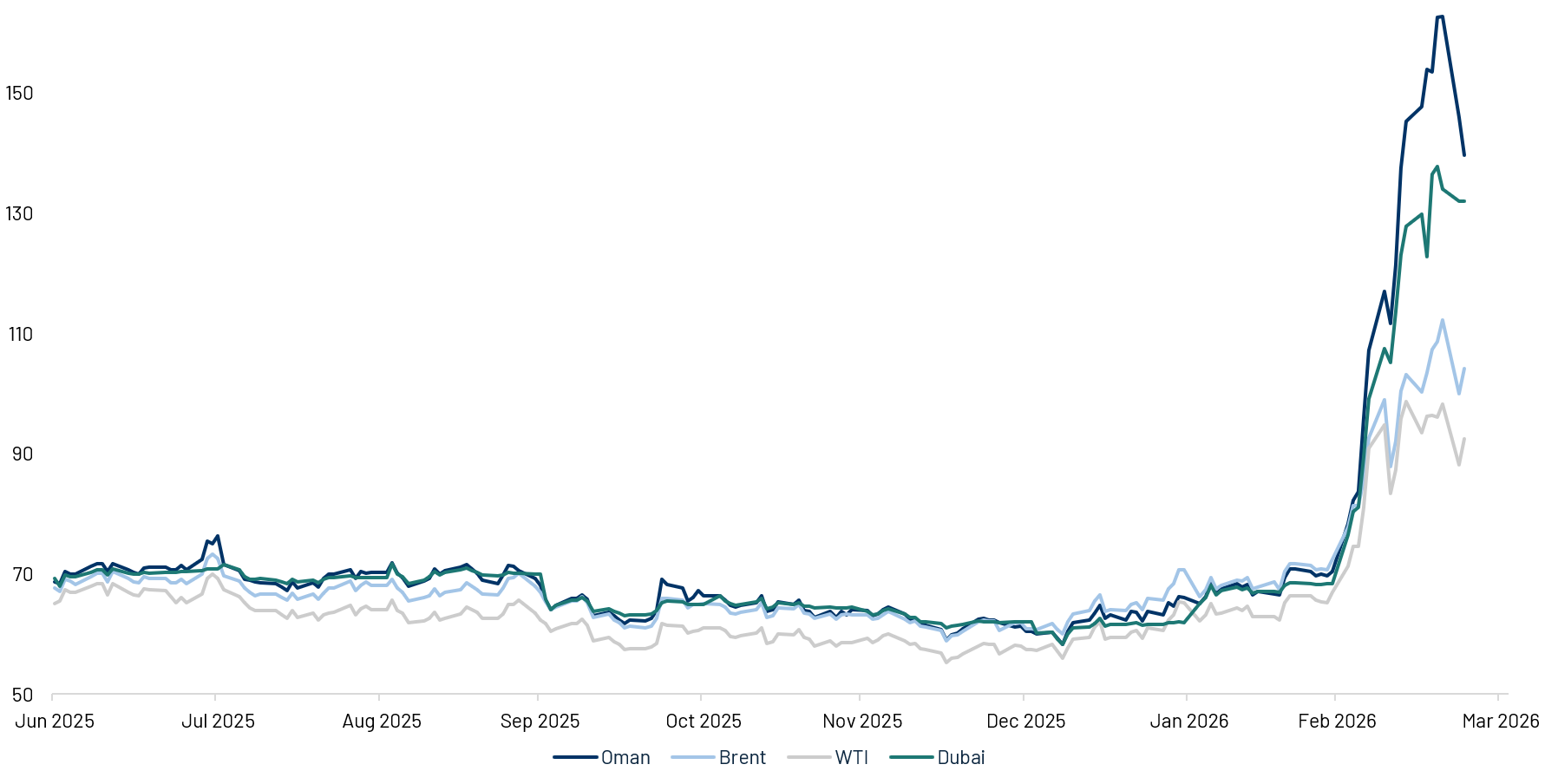

Oil’s wake-up call for consumers

In a market that had increasingly treated oil as a forgotten commodity over the past couple of years, helped by softer price expectations and reinforced by President Trump’s pro-supply “drill, baby, drill” stance, the war has been a sharp reminder that oil remains the world’s most strategic commodity. U.S. gasoline prices have jumped to about $3.96 per gallon, up roughly $1 from late-February levels and now at their highest point since late 2023. The move reflects the surge in crude oil after the Iran conflict disrupted energy flows through the Gulf. Because crude oil accounts for just over half of the retail price of gasoline, higher oil prices feed quickly to the pump. For consumers, this acts like a tax: it squeezes disposable income, hits lower-income households disproportionately, and risks shifting spending away from discretionary categories such as restaurants, apparel, and leisure.

Source: Bloomberg Finance L.P, data as of 23/03/2026.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.