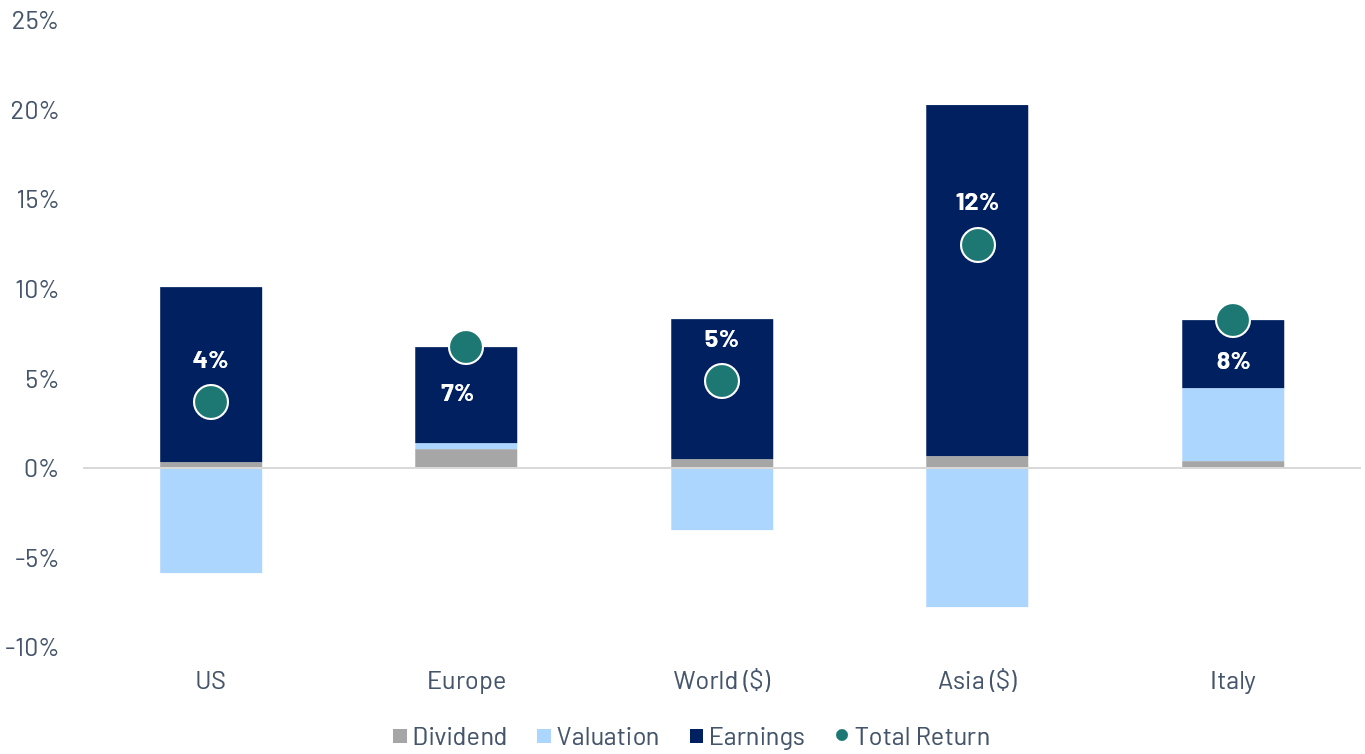

V-Shaped recovery as ceasefire hopes unlock risk appetite

After a sharp sell-off triggered in late February by the US-Israel strikes on Iran and the ensuing disruption to tanker traffic through the Strait of Hormuz, markets spent most of March on the defensive, with the Euro Stoxx 600 posting its worst month since mid-2022 at nearly -10% from peak to bottom. Sentiment turned decisively in early April, when US-Iran ceasefire talks gained traction and Tehran agreed to the conditional reopening of the Strait. Oil prices, which had been trading above $100 per barrel during the peak of the conflict, fell sharply by double digits within days, with Brent falling back below $95. The ensuing risk-on rally was broad-based but particularly pronounced in Asia, which had been hit hardest by the energy shock and trade disruption. Europe staged its strongest one-day advance since March 2022, while the S&P 500 closed at a fresh all-time high on 17th April as the Strait appeared to reopened. As a result, all major indices have now more than recouped their February-March drawdowns and sit comfortably in positive territory year-to-date: Asia leads, up double digits, closely followed by Europe and the US.

Source: Algebris Investments, Bloomberg Finance L.P, data as of 20/04/2026. Performances in local currencies

When sentiment falls, fundamentals matter

Markets are behaving exactly as the old saying goes: they take the stairs up and the elevator down. War and geopolitics have understandably dominated investor attention year-to-date, and the recent move in the S&P 500 captures that mood well: the index came close to a 10% correction and then rebounded almost 13% from its intraday low. Yet beyond the headlines, the macro picture remains challenging. Headline CPI has now spent 60 consecutive months above 2%, even if the Fed’s formal target is framed in PCE terms, and persistent inflation continues to weigh on households. Consumer sentiment, as measured by the University of Michigan survey, has fallen to a record low, highlighting how deeply inflation and uncertainty are affecting confidence. Nevertheless, corporate America is delivering. The Q1 earnings season has only just begun, but all six major US banks have already beaten EPS expectations, while S&P 500 earnings are currently tracking year-on-year growth of 13.2%.

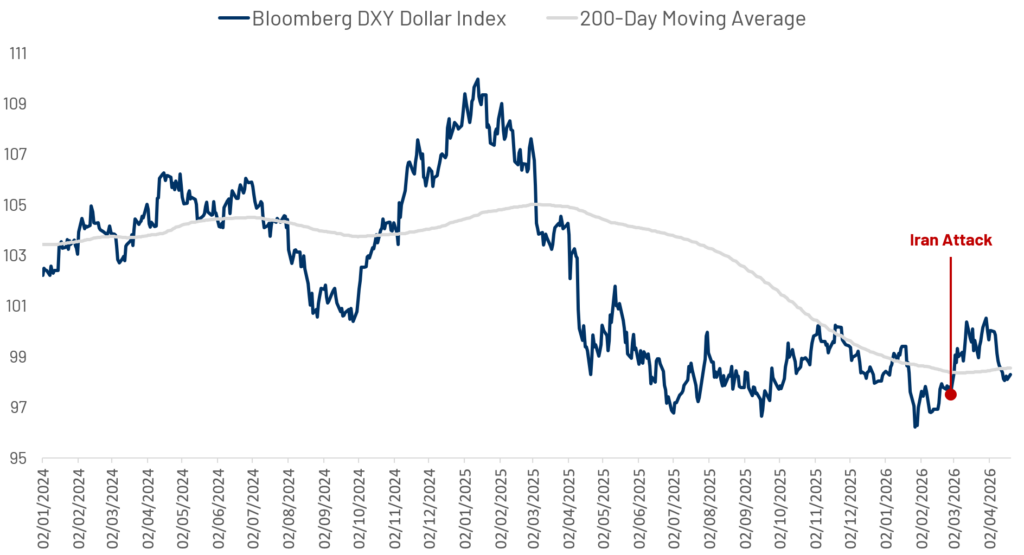

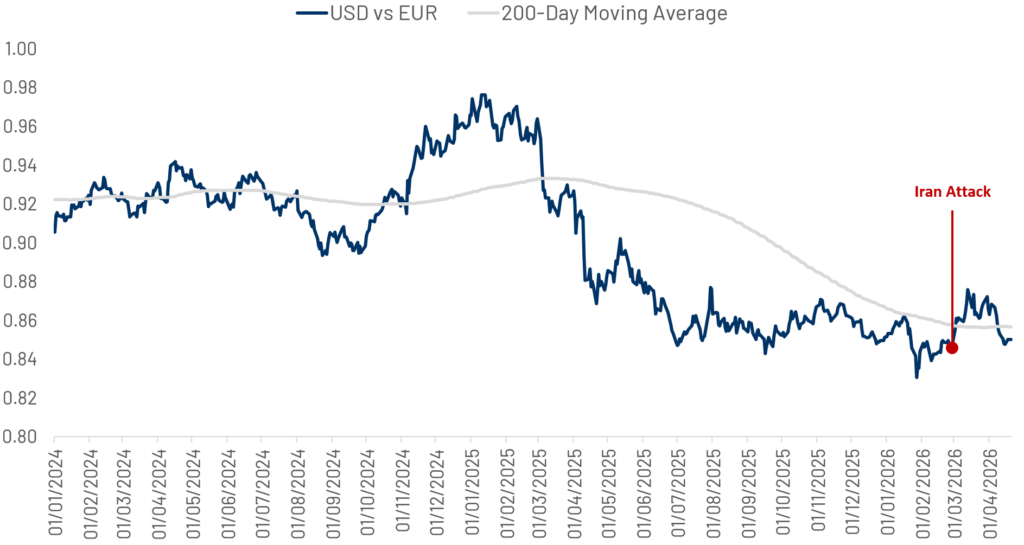

The dollar effect on European earnings

The US dollar has been highly volatile since the start of 2026. After a weak beginning to the year, the coordinated US-Israeli strikes on Iran triggered a sharp rebound, with the dollar rising roughly 4% from trough to peak before giving back those gains and returning to around its starting level for the year. Following the dollar’s marked weakness in 2025, this move has revived the debate over its safe-haven role and the prospect of a more durable recovery. For European equities, however, the broader FX backdrop has not materially changed. Despite the recent rebound, the dollar remains significantly weaker against the euro than it was a year ago. The current USD/EUR rate is around 10% below the average level of Q1 2025, creating a meaningful translation headwind for European companies with sizeable US revenue exposure and limited hedging. Consensus estimates suggest that Euro Stoxx 600 companies generate around 26% of their revenues in the US, while a 10% move in exchange rate can translate into roughly a 2% impact on EPS. Overall, despite recent volatility, last year’s US dollar depreciation is still likely to weigh on European corporate earnings in the next quarter.

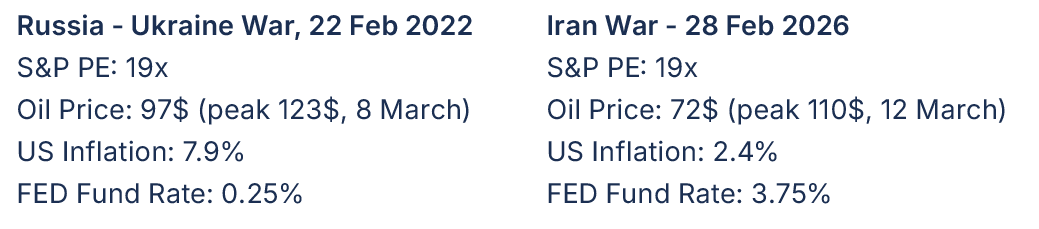

Same headlines, different macro backdrop

The past month was dominated by one macro story: the escalation of the US/Israel–Iran conflict in the Middle East. It pushed oil prices sharply higher, triggered sector rotation, and injected fresh volatility into markets. Major indices had a choppy March but stabilized in early April, supported by strong corporate fundamentals and hopes for a swift de-escalation. The market has naturally drawn comparisons with 2022 and the outbreak of the Russia–Ukraine war. Yet today’s macro backdrop is very different. In 2022, the world was emerging from Covid, inflation was already elevated at 7.9%, economic data were weak, oil was starting from a much higher level and moved even higher, and the Fed had only just begun tightening from 0.25%. Today, valuations may look similar, but inflation is much lower at 2.4%, oil started from a lower base, and rates are already restrictive, with the Fed at 3.75%. In other words, unlike in 2022, this geopolitical shock is not hitting markets that are already dealing with an inflation spiral and the start of an aggressive tightening cycle. Of course, market performance will depend heavily on how long the Iran conflict lasts and whether the current oil shock intensifies further.

Source: Algebris Investments, Bloomberg Finance L.P., data as of 20/04/2026.

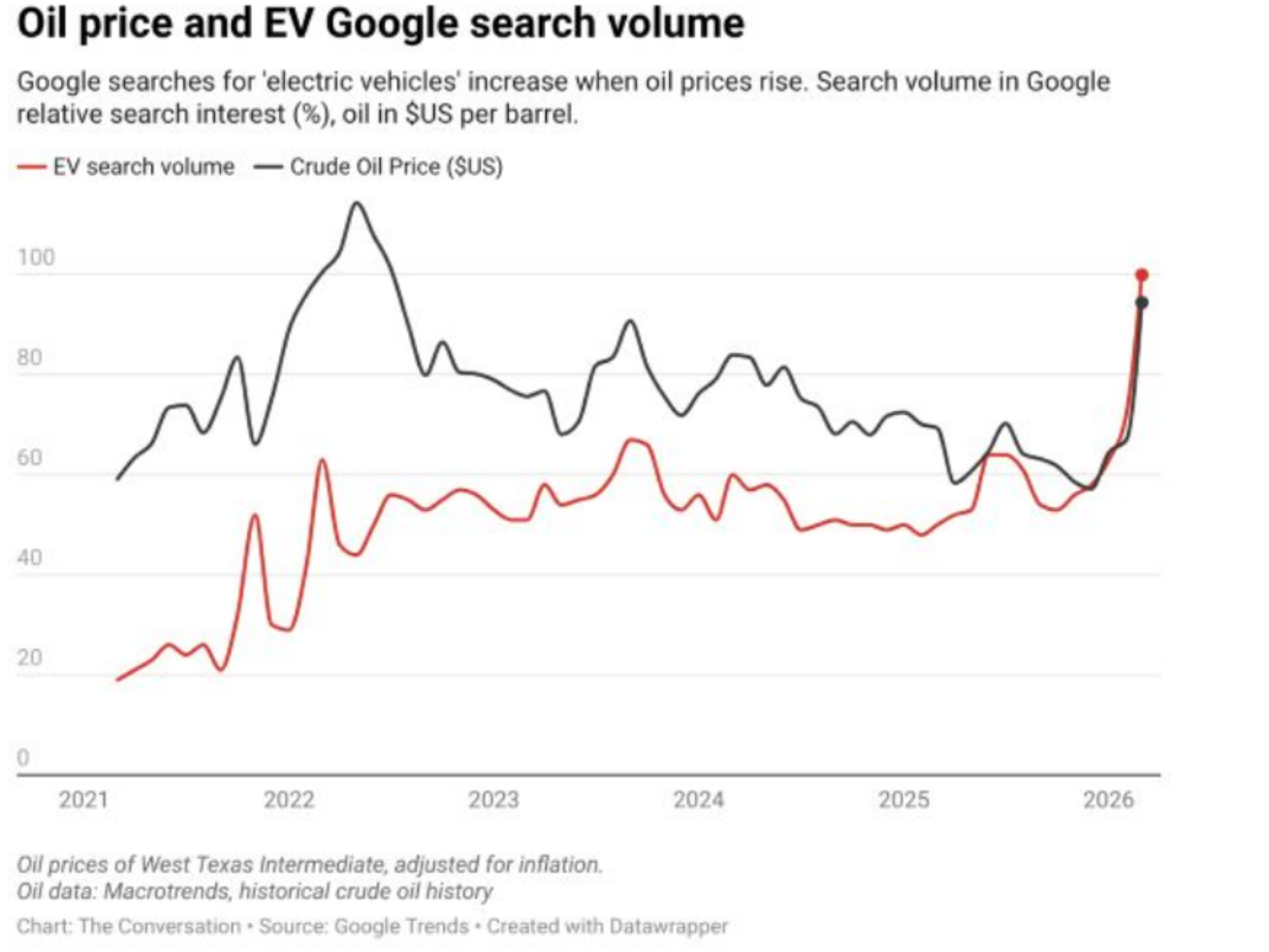

Oil crisis could recharge EV demand

Energy crises often reshape industries and consumer behaviour. The 1973 oil crisis, for example, pushed the automotive industry toward more fuel-efficient cars and engines. Now, with oil prices rising following the US-Israeli strikes on Iran, both consumers and policymakers may once again reassess the appeal of electric vehicles (EVs). Historically, the link between petrol prices and interest in EVs has been clear: when fuel costs rise, consumers become more willing to consider buying an electric car. This was evident in 2022, after the oil price spike triggered by the Russia-Ukraine war, and it appears to be happening again today. Whether this renewed interest will translate into stronger EV sales will become clear over the coming months, although there are already some early signs of this trend in parts of Asia and in Australia. This could represent another challenge for European and US OEMs, given their weaker competitive position relative to Chinese carmakers in EV powertrains.

Source: Google Trends, Murdoch University., data as of 20/04/2026.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.