The AI wave lifts all boats

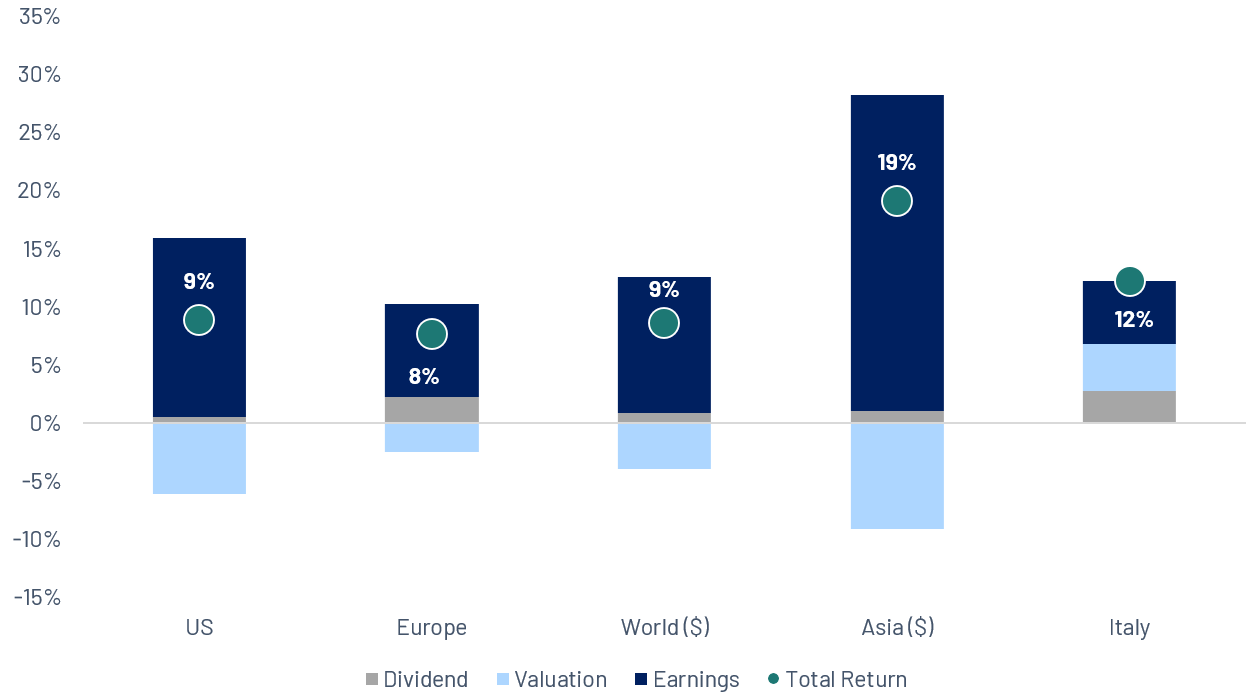

Building on the sharp April recovery, equity markets extended their gains through May, with ceasefire talks between Washington and Tehran continuing to set the tone, oscillating between optimism and setback before Trump declared negotiations were in their “final stages” late in the month, pulling oil back from its highs. The dominant theme across the period, however, was artificial intelligence. Nvidia’s blowout earnings on May 21st acted as a catalyst across the board. The Korean Stock Exchange Index (KOSPI) surged over 8% in a single session, Samsung and SK Hynix both hit record highs, and the Nikkei broke through 65,000 for the first time. In the US, the S&P 500 closed at a fresh all-time high above 7,230 on May 1st, supported by a strong Q1 earnings season and still resilient labour market data, though a hotter-than-expected CPI print mid-month injected some caution around the Fed’s trajectory under incoming Chair Kevin Warsh. Europe lagged relative to Asia and the US, remaining more exposed to residual energy price volatility and the prospect of ECB tightening. Year-to-date, Asia continues to lead, with the technology-heavy indices in Korea and Japan posting exceptional returns; the US and Europe remain firmly in positive territory.

Source: Algebris Investments, Bloomberg Finance L.P, data as of 22/05/2026. Performances in local currencies

Q1 Earnings: Momentum in the US, Resilience in Europe

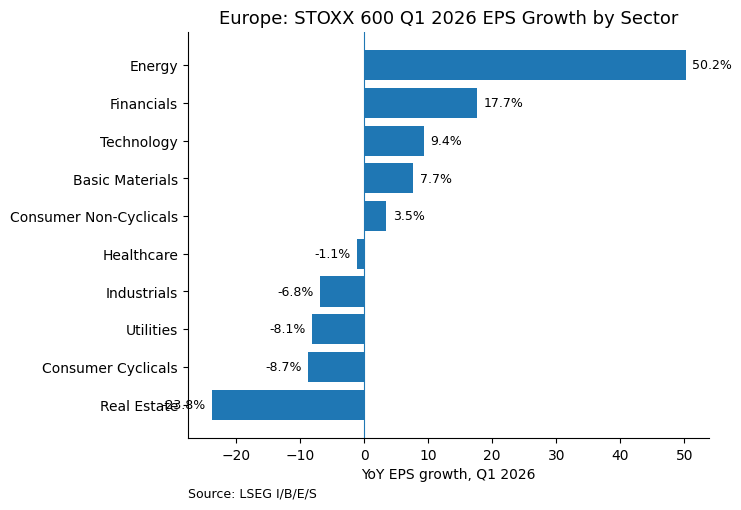

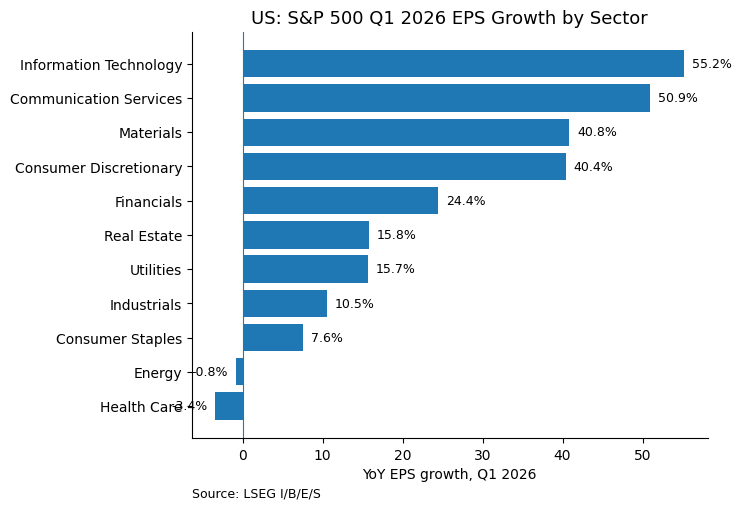

In the US, earnings remain the clearest fundamental support for the market: in 1Q26 the S&P 500 delivered a very strong EPS beat rate, with 84% of companies beating expectations, and Q1 earnings growth estimates were being revised sharply higher through the season. The season confirmed that corporate fundamentals continue to support market performance, with Technology, Communication Services and AI-related capex beneficiaries remaining important sources of earnings strength. In Europe, the season was also better than expected: the STOXX 600 delivered a solid 58% EPS beat rate, above its historical average, while earnings revisions turned positive, helped by Energy, Financials and selected defensives. Europe’s story is less about broad demand acceleration and more about resilience: revenues remained soft, while earnings upside came mainly from margins, cost discipline and sector mix. Overall, in the US, earnings are still providing a powerful engine for the market, supported by structural growth themes; in Europe, the earnings floor looks firmer than investors feared, and the next phase will depend on whether margin resilience can be complemented by a clearer recovery in revenues.

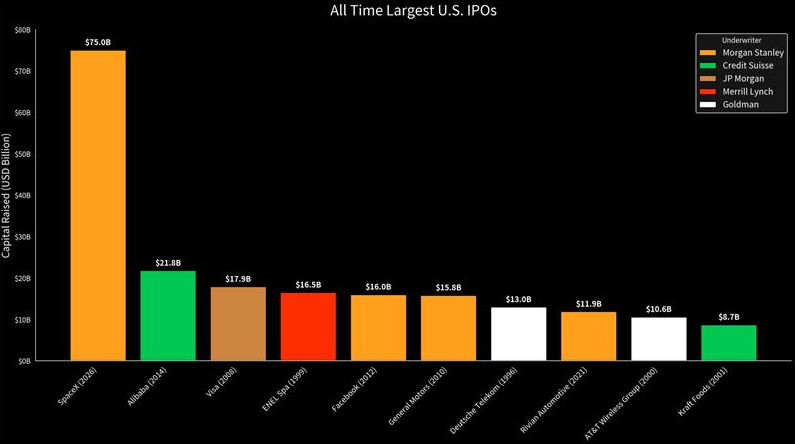

You’re already buying SpaceX – Whether you like it or not

After two quiet years, the US IPO market is reopening, and this time, the companies coming to market could be unprecedented in scale. SpaceX, OpenAI and Anthropic carry implied valuations that would place them among the ten largest companies on earth the moment they begin trading. For portfolio managers, this wave is a structural event, with implications for index weights, passive flows, liquidity regimes, and concentration risk across the entire equity book. SpaceX at $1.75 trillion would slot in behind Amazon as roughly the sixth-largest US company by market cap on day one. If included in the S&P 500, passive funds tracking the index (managing in excess of $20 trillion) would be mechanically required to buy. The mechanical consequences are meaningful for existing index holders: when passive funds must absorb new mega-caps, they sell incumbents to make room. The rotation is not discretionary. It is algorithmic. Prior mega-cap additions (Meta in 2012, Tesla in 2020) caused measurable rebalancing distortions; the 2026 cohort is larger by an order of magnitude. Millions of investors could end up owning SpaceX through their index holdings, regardless of whether they actively decided to invest. In this market, The only antidote is knowing exactly what you own, why you own it, and what happens to it when SpaceX starts trading on June 12th.

Source: Bloomberg, data as of 22/05/2026.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.