Equities – Showing remarkable resilience

Global equities remained resilient over the last few weeks, despite the ongoing U.S. government shutdown and geopolitical shifts in the Middle East, where a recent peace agreement improved market sentiment.

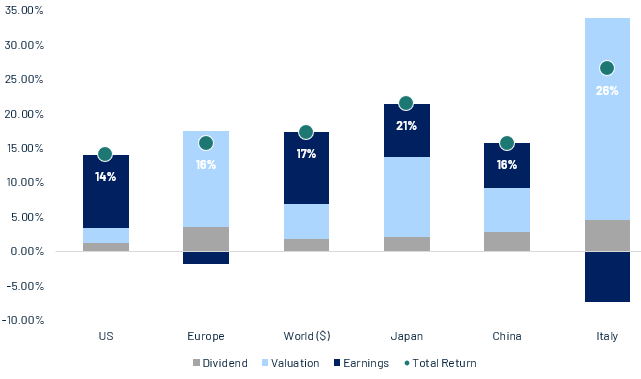

In the U.S., equities proved remarkably resilient. Markets are edging higher despite three headwinds, the government shutdown, renewed trade tensions with China over rare earth exports, and pressure on regional banks following surprise loan losses. The earnings season also started on a positive note, with most large banks beating expectations. In Europe, news flow was limited with only a few companies reporting Q3 results, yet the region continues to benefit from attractive valuations and a less overheated market compared to the U.S., keeping investor interest alive. The standout performer was Japan, where political developments and the formation of a new ruling coalition reignited hopes for fiscal stimulus and supportive policy.

Source: Algebris Investments, Bloomberg Finance L.P, data as of 17/10/2025. Performances in local currencies.

When Incentives Fade – The real EV demand test begins

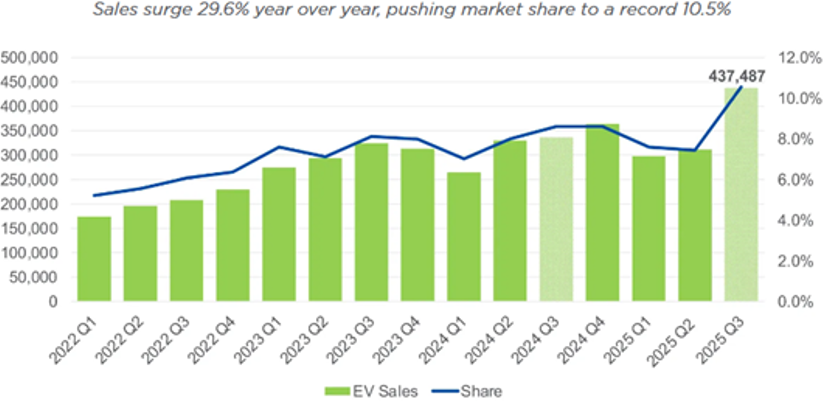

U.S. EV sales set a fresh record in 3Q25 at roughly 438,487 units, about 41% above 2Q and 30% higher year over year, pushing EVs to ~10.5% of new-car sales. Much of the surge looks like demand pulled forward as buyers rushed to capture the $7,500 federal credit before it expired at the end of September. With incentives now fading and little clarity on near-term replacements, the quarter underscores how fragile underlying EV demand is without subsidies and how the policy wind is turning less supportive.

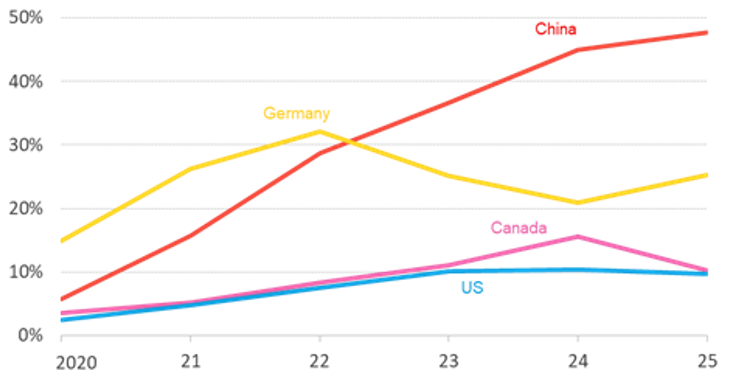

That backdrop is colliding with a difficult industrial transition. For European and North American carmakers, moving from legacy ICE to EV has proved challenging, rules have been stringent, end-customer demand uneven, and Chinese competitors increasingly fierce. Automakers are lobbying for a smoother ramp, and policymakers are starting to ease off. In the U.S., the “One Big Beautiful Bill” effectively dismantled CAFE enforcement by removing penalties for missing CO₂ targets, and a repeal of the EPA’s Endangerment Finding would further loosen emissions constraints. In Europe, the Commission in March softened the 2025 CO₂ intermediate step, allowing compliance to be averaged over 2026–2027 and brought forward the review of the 2035 ICE phase-out to end-2025 (from 2026). Together, these shifts point to a longer, bumpier transition path and a market more exposed whenever the subsidy safety net recedes.

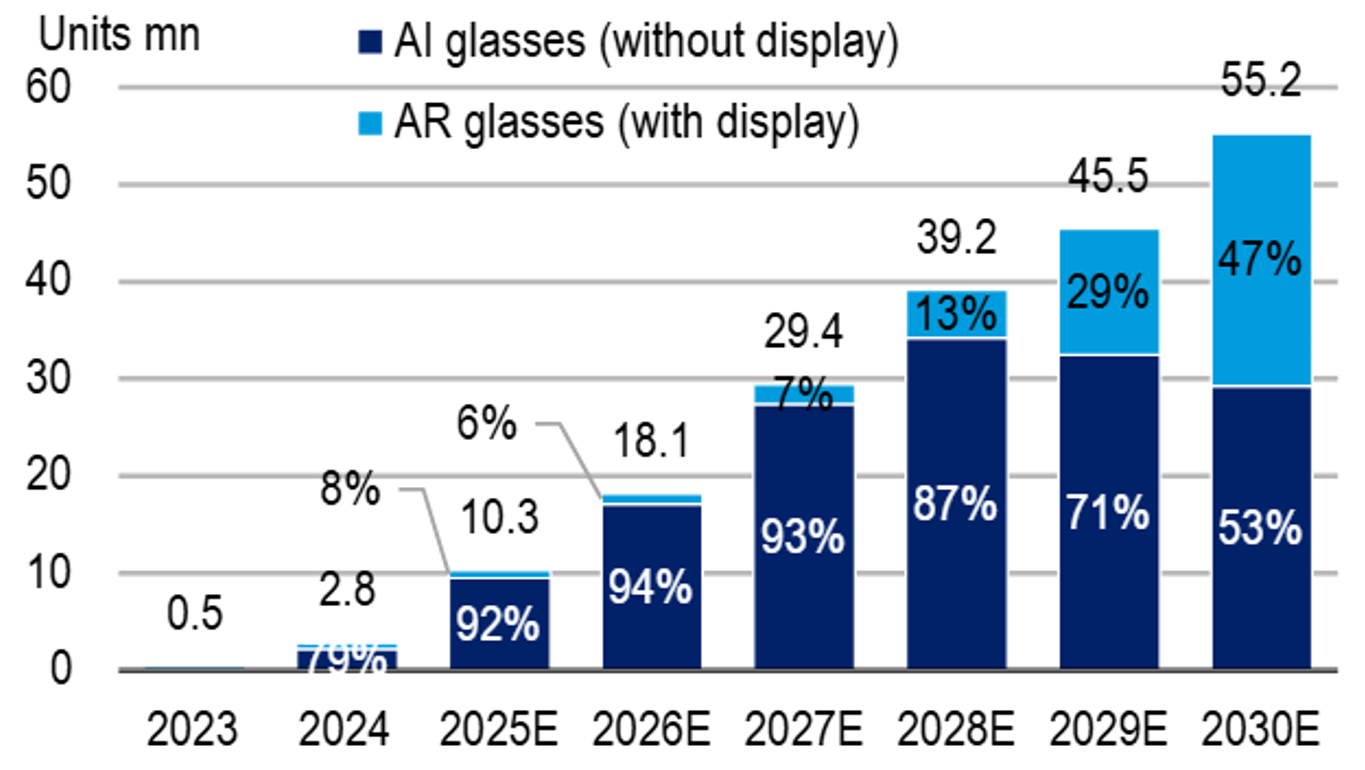

See the Future: Smart glasses to power a $14B digital display revolution by 2030

The breakout success of Ray-Ban Meta (co-developed by Meta and EssilorLuxottica) has kicked off a new race among tech giants, from Apple and Samsung to Amazon, Google and ByteDance to define the next consumer interface, AI and AR powered smart glasses. Global shipments are projected to rise from ~2 million units in 2024 to ~10 million in 2025, reaching ~55 million by 2030, creating a ~$14B hardware market growing at ~64% CAGR.

Momentum is already showing up in the numbers. In 3Q25 EssilorLuxottica posted record revenue of ~€6.9bn, up ~11.7% y/y, with Ray-Ban Meta contributing over 4 percentage points of growth, the company is accelerating capacity plans toward ~10 million units annually ahead of schedule.

The early cycle is being led by AI glasses, lightweight, display-free devices optimized for camera, audio, and on-device AI, while AR glasses with waveguide lenses and micro-displays should take over beyond 2027. The supply chain remains Asia-centric, with ~80% of suppliers based in China and tight integration across semiconductors, cameras, optics, batteries, and assembly. As optical and power bottlenecks ease, adoption is spreading from consumer brands like Meta, Xiaomi, and Rokid to enterprise players such as Microsoft and Lenovo, signalling the dawn of a new lens-based era of connected computing.

Source: BofA Global Research estimates, IDC (September 24th, 2025)

Luxury equities — 2025 read-through (using LV as the barometer)

LVMH’s Q3-25 showed a bottoming rather than a full turn: Group organic sales rose +1% to ~€18.3bn, while Fashion & Leather Goods (the proxy for core luxury demand) was –2% y/y but markedly better than –9% in Q2; Louis Vuitton ran a touch ahead of the division. Selective Retailing (Sephora) stayed a bright spot at +7%. Regionally the improvement was led by U.S. +3% and Asia ex-Japan +2%, with Europe –2% and Japan –13% as tourism corridors and yen weakness bite. Taken together, after roughly 4–5 quarters of lacklustre/negative prints, the data suggest stabilization with ongoing bifurcation: ultra-high-end and beauty resilient; aspirational price points still soft.

For the sector, while pricing power is normalizing and wholesale clean-up continues, the set-up for 2026 looks cleaner betting on re-acceleration on easier comps and healthier channels. However, what we have to keep in mind is that today’s luxury conglomerates runs with heavy cost bases (flagship networks, marketing engines, craftsmanship capacity, data/tech stacks). With organic sales at low single digits, you don’t get true operating leverage—mix, pricing, and cost discipline help, but they mostly defend margins. To actually expand margins, the sector needs a return to mid-single-digit organic growth so fixed costs are absorbed and incremental profitability kicks in. In other words: scale is no longer enough; through-cycle margin upside now hinges on stronger organic top-line.

Algebris Investments’ Global Equity Team

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

Any opinion expressed is that of Algebris, is not a statement of fact, is subject to change and does not constitute investment advice.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.