“Take some more tea-LTRO,” the March Hare said to Alice, very earnestly.

“I’ve had nothing yet,” Alice replied in an offended tone, “so I can’t take more.”

“You mean you can’t take LESS,” said the Hatter: “it’s very easy to take more than nothing.”

Adapted from Alice in Wonderland, Chapter VI, by L. Carroll

Aalborg is a lovely town in Denmark featuring Viking ruins, cosy pubs and a Zoo with 1500 animals. But Aalborg’s most interesting attraction may soon be negative rate mortgages: a Danish couple received 249 Danish Kroner ($37.8) on their latest instalment (WSJ).

Denmark is one of several countries with negative interest rates. The list is growing quickly. Deposit rates are negative in Switzerland, Sweden, Denmark, Hungary, Japan and the Eurozone. Refinancing rates are negative in Switzerland and Sweden, zero in Japan and the Eurozone.

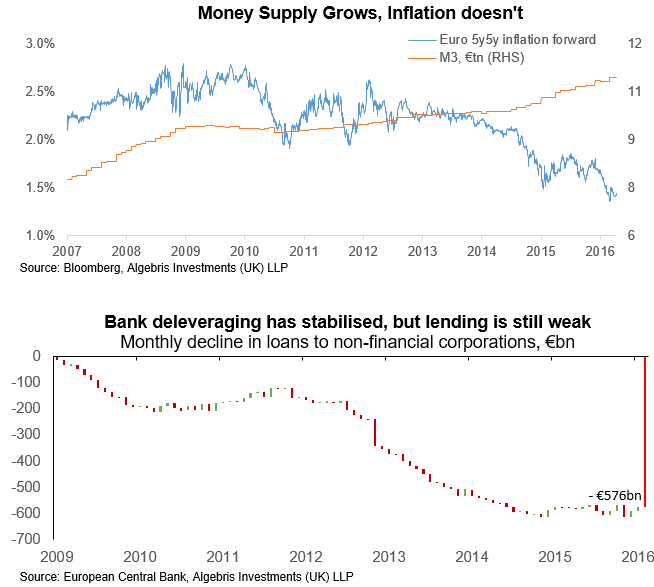

The idea behind negative rates is to discourage banks from hoarding cash, pushing them to deploy capital into riskier assets, such as loans. In the Eurozone, banks pay to deposit cash at the ECB and get paid up to 0.4% to borrow from the ECB under its new TLTRO II programme. Like Mad Hatters in Alice in Wonderland, Central Banks continue to pour tea into Alice’s cup. But are zero or negative rates going to work, and what are the collateral effects of this potentially never-ending tea party?

- Question: do negative interest rates work? The evidence is mixed. Negative interest rates were used in Switzerland in the 1970s (1972-1982). However, the policy objective was different from today’s attempt to reanimate a slowing economy. At the time, the SNB was trying to discourage buying of Swiss Francs as a safe-haven currency, but it still didn’t succeed in countering a substantial 29% real appreciation over the 1973-1978 period. Today, negative interest rates policies (NIRP) aim at making banks put cash to work in the real economy. A recent research paper by the BIS explores how central banks have implemented NIRP and looks at the pass-through beyond money markets: in the Eurozone and Sweden interest rates on loans and mortgages have fallen in lockstep with central bank rates. In Switzerland and Denmark, short-term loan rates and long-term bond yields have fallen, but banks raised mortgage spreads, so borrowers aren’t better off. But the key question is whether lending volumes are recovering, i.e. if corporates are using those low rates to invest and create jobs. ECB MFI balance sheet data shows that lending volumes have stabilised, but haven’t recovered. The data still doesn’t include the effect of TLTRO II, but recent anecdotal evidence suggests lending remains muted.

Answer: there’s only so much tea Alice can drink, even if the Mad Hatter continues to pour it.

- Question: how low can rates go? Lower than they are now – said ECB Chief Economist Peter Praet last month (FT). The lower bound depends on what alternatives depositors have: the ability and cost of storing cash, including insurance. Munich Re, a German re-insurer, has recently announced it will store €10mn to avoid paying ECB fees (Bloomberg News). How much does it cost? Excluding insurance, the cost of an “extra-large” safe deposit box in London (55x25x25cm) is around £600 a year. Each safe deposit box is around 1/30 of a cubic metre and should hold around £1.1mn (see FT Alphaville for cash/volume estimates). This means a cost of around 5.5 basis points using £50 Bank of England notes and half for £100 Scottish notes (cheaper, although that would leave you exposed to the risk of Scottish independence…). The cheapest cost of storage would be achieved using €500 notes, which the ECB is considering to ban (Reuters). Adding the cost of insurance (£1.25 for every £1,000) the total storage cost for a year would be £1,990 for £1.1mn – a total of 18 basis points. Should interest rates go below -20bp for savers then people could be encouraged to store cash rather than invest in riskier assets. This puts a theoretical floor on how negative rates could go. Of course, policymakers could find other ways to extend the floor, including banning cash altogether, as the Bank of England’s Chief Economist Andy Haldane proposed earlier. But then again, savers could get creative too, finding other cash-park assets (gold, bitcoin, London flats…).

Answer: if Alice has to pay to not drink tea, Alice may leave the party.

- What’s the impact on savers and banks? The impact of lower (or negative) interest rates on bank profitability is positive near-term, because it helps to reduce bankruptcies, but can be negative medium-term, reducing bank profitability. Research from the BIS last October suggests that persistent negative rates can erode bank profitability over time. This is one reason why the ECB has introduced a subsidy to banks borrowing under TLTRO II (borrowing banks get paid up to 40 basis points, depending on their lending volumes). So far banks have not passed on the cost of negative deposit rates to customers. In Japan, however, last month some trust banks have started to charge clients for holding cash (Reuters).

Answer: when the cost of not drinking tea rises, things can get complicated.

- How does the future look like? The ECB meets again this week, holding its press conference on April 21. After the many measures at its March press conference, we only expect clarification on the details of the programme, including purchases of corporate bonds. The BoJ will follow with its next meeting on April 28, possibly with more easing to counter its rising Yen. But more generally, the question remains open whether prolonged low interest rates may work and eventually allow for higher rates in the future. We all know the textbook economics answer: low interest rates boost demand, jobs, growth and inflation. But reality is different: low interest rates don’t always work. The IMF shed some light on the question in its World Economic Outlook last year (Chapter 3, page 77): “Financial crises may permanently reduce the level of potential output through a number of channels: investment in productive capital, potential employment, total factor productivity, and sectoral reallocation of resources.” Put differently, a financial boom-bust cycle may lead to underinvestment in some areas and overinvestment in others. The longer the reallocation process lasts after the bust, the longer productivity stagnates thereafter. A recent piece by VOX.eu estimates that resource misallocation may erode around 0.3-0.4% of GDP growth annually over the 5 years following a financial bust. This is not surprising: it takes time for economies and labour markets to adjust. Most of the slack left in US labour markets is concentrated in certain sectors (Agriculture, Mining/Energy and Construction) – coincidentally, these are the same ones which were growing fastest before the crisis, thanks to cheap financing. Today, workers need to re-train, companies need to adjust capacity overhangs and investors/banks need to absorb losses. The invisible hand of markets is a little tied up.

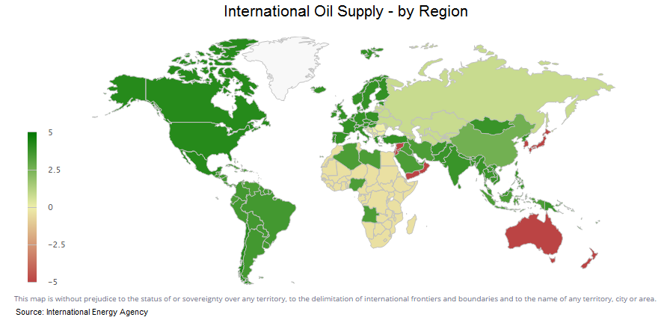

There are solutions. In Australia, for example, mining workers are getting free re-training. But their colleagues in other countries do not always enjoy the same treatment, many of them ending up with low-wage temporary jobs. Like re-training workers, adjusting industrial overcapacity is equally difficult. The map above shows that oil supply continues to grow globally, despite the imbalance with demand. Together with excess capacity, finally, comes excess debt and debt losses: these needs to be restructured too. But taking losses is easier in capital markets and where bankruptcy procedures are efficient, as in the US, a lot harder in bank-centred financial systems. In the Eurozone, non-performing loans still amount to €1tn, roughly 10% of GDP. Around €300bn are in Italy, where the bankruptcy process lasts up to 7-10 years.

Answer: if you drink a lot of tea, you may end up needing more tea.

- Is this readjustment process in labour markets, industrial overcapacity and debt made easier or worse by low interest rates? If monetary policy is the only game in town, then low interest rates may delay economic adjustment, as the BIS explains in recent research:

“The bottom line is that, over sufficiently long horizons, low interest rates become to some extent self-validating. Too low rates in the past are one reason – not the only reason! – for such low rates today. In other words, policy rates are not simply passively reflecting some deep exogenous forces; they are also helping to shape the economic environment policymakers take as given (“exogenous”) when tomorrow becomes today.”

Put differently – there could be a sort of reflexivity in central bank policy. Persistent low interest rates may delay economic restructuring of zombie corporates and banks, which in turn may make it more difficult to raise interest rates in the future.

Answer: tea isn’t always a good idea.

Conclusions: No Creation without Destruction

- Negative interest rates have had mixed effects in the past.

- Rates can go even lower than today. Central bankers may try to increase the cost of storage and/or limit holdings of cash to decrease rates further.

- So far, banks have not passed the cost of negative rates to savers, but there are signs that this may be starting to happen. If the cost of bank deposits rises to a certain threshold (say -0.2%) savers may put money under the mattress.

- Negative/low interest rates help in the near-term, but they can be self-validating if not accompanied by other policies (fiscal stimulus, reforms, adjustments in industrial capacity and in the banking system). If low interest rates prevent or delay re-adjustment (destruction), this can impair growth and productivity (creation). The longer losses stay in the system (e.g. Eurozone non-performing loans), the heavier the drag on growth. Schumpeter had a point.

- The result is that the NIRP/ZIRP party will go on for longer, affecting investors and savers. The endgame could be Helicopter Money – a stronger form of QE – or debt restructuring. But will take a long time to get there

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.