The pandemic has put humanity at a crossroads.

One way leads to a more sustainable economy where the gains from technology are shared among everyone, reforms break monopolies, re-distribute opportunity and boost productivity.

The other way is a longer and more painful liquidity trap, where the wrong set of temporary kick-the-can policies continue to be applied as if they were a long-term cure. Eventually, this will likely lead us to become a more divided society, where rich countries reap the benefits of the vaccine, technology increases the gap between the haves vs the have-nots, and economic policy compounds the rewards for strong firms over weak ones.

We have long argued that the combination of corporate tax cuts, loose anti-trust rules and asset-focused monetary policy over the past decade contributed to a winner-takes-all effect across both firms and the broader society. Today, this is evident in the gap between markets and the economy. Large firms with liquid bonds and listed equities are doing great, and their valuations reflect a V-shaped recovery. Economic conditions, unemployment for the poorest quartile of the population and business activity across small firms, instead, show us a K-shaped reality.

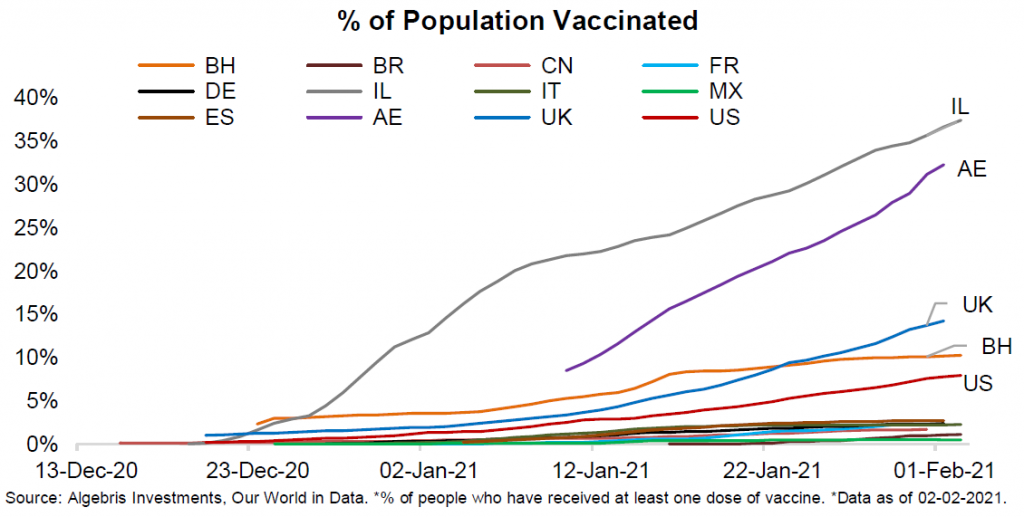

One in five low-income earners is out of a job, compared to January 2020, while employment levels for high earners, who are more likely to be able to work remotely, are roughly unchanged, in the United States. The UK and US have vaccinated over 14.2% and 7.9% of their population, respectively, and are likely to achieve immunity before year-end. We don’t know when developing countries, already hard-hit by a reduction in travel and tourism, will achieve similar results.

As long as our economy is fragile, we believe the recovery in financial markets will remain shaky as well. This is clear from recent price action in equity markets, where a short squeeze on a few mid-cap stocks recently threatened to trigger a widespread deleveraging.

There is one potential game-changer. Today, the Biden-Harris administration has a chance not only to stimulate the weakest areas of the US economy, but to shake up productivity and boost growth.

And here lies the most important question for investors, in our view: can the United States beat secular stagnation?

The answer depends on the upcoming stimulus plan. The first $1.9tn stimulus, currently under discussion, involves mostly emergency aid to individuals, states and local authorities. It is a step forward in comparison to previous policy actions. But to push the US economy out of the Covid crisis and out of secular stagnation, what is needed is much more radical.

Investing in infrastructure, opening up access to education, improving competitiveness and breaking up existing monopolies across most economic sectors – from cars to soft drinks to processors – are some of the key steps which will determine whether our economy will come out of the Covid crisis stronger, or weaker and more divided.

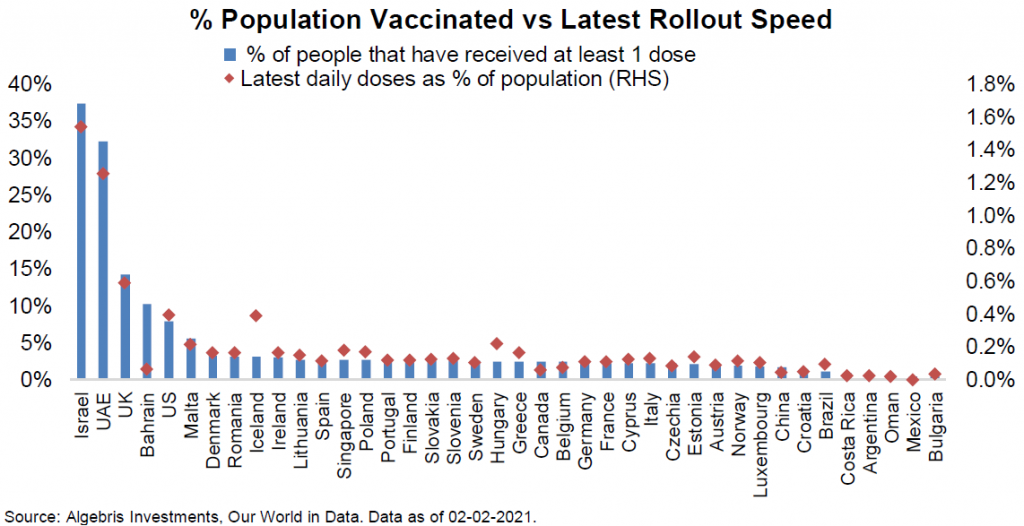

Covid-19 Vaccinations: A Race Against Time

Vaccination campaigns have started in over 65 countries with 103mn doses administered, covering around 1.1% of the global population. However, there is large variation in vaccination speed across countries. The clear leader in the race is Israel, where near 40% of the population have received at least one dose and one fifth are fully vaccinated. Based on its current daily rollout speed, Israel is on track to vaccinate 75% of its population by mid-March 2021. The UK and US have also been ramping up speed, with the UK having vaccinated 14.2% of its population vs 7.9% for the US. However, other developed countries are off to a much slower start. EU countries in general have only managed to vaccinate around 2-3% of their population respectively, and are struggling to increase daily rollout with both Pfizer and AstraZeneca having supply disruptions in Q1.

Developed countries face challenges including supply bottlenecks, insufficient distribution channels and poor coordination between different levels of government. Most of these challenges could be tackled relatively quickly and may only lead to short-term delays. For example, Pfizer announced a plan to meet its Q1 target for the EU by increasing deliveries from mid-February, and to accelerate deliveries in Q2 with up to 75mn additional doses.

Emerging countries face much more difficult challenges. Many of them have not yet secured or simply could not afford sufficient vaccine orders. This does not only raise the question of inequality, but prolonged delays in vaccinating people in poorer countries could also mean a slower and imbalanced global recovery, at the same time giving the virus more time to generate potentially harder-to-deal-with mutants.

The Biden Plan: Can America Escape Secular Stagnation?

New fiscal bill – time to be bold. A large Covid-relief bill is at the helm of the Biden agenda. Several fiscal measures adopted during Covid-19 will expire in 2021. The $900bn bill passed last-minute in December was a compromise by nature, and lockdowns have worsened since Christmas: the economy is in need of further support. With popular demand and a clear mandate, we think Biden may well go big. The market is now expecting a stimulus bill in the $900bn-$1.3tn range. Still, the original proposal was closer to $2tn, and reasons to appeal to moderates within the party go down by the day as the economy cools down and even the Fed calls for a larger fiscal presence. We therefore see a surprise to the upside as a very concrete possibility. The new bill should be discussed over the next six weeks and passed by the end of March.

Stimulus + recovery = spending sugar. A quick and large fiscal plan will boost personal income and spending. 30-50% of the plan is likely to focus on income-supporting measures, including stimulus checks and unemployment support. US savings rates are still hovering around 12%, compared to 8% pre-Covid and in gradual decay since the 30% high reached before summer. More stable income and less Covid-19 uncertainty will support spending and activity, with the potential for a booming US economy in 2H21. Local government support and tax credit expansion are the other large line items on the bill, arguably carrying a lower impact on the economy.

The Fed is likely to stay dovish.More 2021 stimulus will keep the pressure on Treasuries high. At current policies, the US Treasuries net supply for 2021 will hold at $2.5tn, compared to “just” $1tn in Fed purchases. The net amount hitting markets will be the highest since 2010, while 10y yields are at the lows since then. At the same time, Europe’s supply after ECB purchases will remain well in negative territory. Finally, spending and income growth will mean some inflation. With treasuries yielding 1%, a gradual increase of inflation towards the 2016-19 2-2.5% range would be a welcome return to target for the Federal Reserve, which is unlikely to change course in the near future.

Looking ahead: infrastructure, environment, human capital. While the immediate focus is on Covid-19 relief, we see medium-term action as the key to successfully boosting productivity growth. Infrastructure and construction are key elements of the plan presented during the campaign and are all areas in which the US has much to gain. At current policies, the US is projected to spend 1.5% of GDP in infrastructure improvement over the next 20 years, vs 5% in China, 3% in Japan and Russia, and 2.5% in France and Italy. The American Engineering Association estimates the “infrastructure gap” to account for almost $4tn in GDP loss on a five year basis. Infrastructure spending is thus relatively feasible and high-return in the current environment. Environmental and green spending are another clear focus. Finally, education spending will likely account for 5-10% of the upcoming March bill, and the administration may be finally addressing the well-known student loan issue.

Foreign policy – picking battles.On foreign policy, Biden is likely to affirm US interests in a firm but less confrontational and more predictable fashion compared to the previous administration. The first steps seen so far are encouraging. The Biden administration has suggested the possibility of both cooperation on climate change and strategic competition on the digital side, pointing to a balanced and case-by-case approach. Initial steps towards Russia are in the same direction. The nuclear non-proliferation treaty is likely to be extended soon while on elections interference a tougher line will be adopted. The focus on trade tariffs is likely to be abandoned completely.

Fiscal profligacy to stay.The US is just coming out of the toughest year since the Great Depression, and a very uncommon Presidency. It is thus very hard to say how close to promises the new administration can be. Still, we think this is a historic chance to boost productivity, growth and inflation, allowing for an exit from QE infinity monetary stimulus. A swift focus on income support will keep spending and the economy alive in 2021. Over time, we expect deficits to gradually come down. However, a level of fiscal profligacy might become structural and demanded by voters – as long as economic growth is not shared across weak parts of the country and the population. Against this backdrop, the Biden administration measures remain tame. With war-time deficit levels, the level of current tax rates, as well as of real interest rates remain still generous against historical comparisons. History tells us that there are two ways to exit such a period of chronic high debt: growth or financial repression through inflation, taxes or default. What would investors face if the new policy measures fail?

What if QE Infinity Lasts for Longer? Monetary Policy 4.0

Monetary Policy 2.0: Monetary policy is unprecedentedly loose and is likely to remain so for at least H1 2021, if not the full year. Last year, central banks exponentially expanded monetary policy and embraced monetary policy 2.0; i.e. relying more on bond purchase programs than interest rate cuts to stimulate growth. For the first time, the Fed began to buy IG corporate bonds, mirroring the existing approach of the ECB, BoJ and BoE. Both the ECB and the Fed signaled in January that it is too early to talk about exiting these emergency policy actions.

However, rising inflation risks in H2 2021 pose a threat to extra-loose policy and negative real rates. At the current pace of vaccinations both the UK and US could reach herd-immunity by the summer, with Europe later in the year given its vaccination sourcing troubles. Therefore, we could begin to see more normalized levels of activity in the UK and US in H2 2021 and potentially Q4 in Europe. In the US, this would mean the current 4% of GDP built in excess personal savings could be unleashed on the economy boosting inflation. This is not including the additional $1-1.9tr in fiscal spending being debated in Congress currently, nor the possibility of a new infrastructure spending plan. It is still early to assess how much and how fast this money may be spent and to what extent it would lead to higher inflation. However, US inflation-swaps are pricing inflation in 1 year to around 2% and there are early signs that US inflation may exceed that.

Monetary Policy 3.0: if the economic recovery takes longer, central banks will do more, as reiterated by the Fed and ECB. While monetary policy is already unprecedentedly loose, the reality is that it can be looser still. In 2016, the ECB published a speech discussing the limits of policy. Rather than economically-derived limits like central bank balance sheet as a % of GDP or balance sheet as a % of market cap, the argument focused on the legal prohibitions of monetary financing and on “proportionality” limits (that is, the benefits of more stimulus must outweigh the costs). Therefore at the next crisis, there may be little preventing the Fed or ECB increasing their balance sheets from currently 35% and 62% GDP to that of the BoJ’s or SNB’s at 133% and 150% GDP respectively.

Monetary Policy 4.0: if economic stagnation lasts for long, central banks may test new final frontiers of monetary policy and financial repression: Modern Monetary Theory (MMT) and digital currencies. As mentioned in the ECB speech above and also reiterated by the BIS, the main constraint to monetary policy is the intellectual and legal prohibitions on monetary financing of the public deficit. MMT however advocates that this constraint be abolished; that deficits can be as large as needed and they can be funded through central banks printing currency. That is, MMT codifies and legalizes the concept of QE infinity, as we have been writing for many years. While MMT has historically only been advocated by fringe economists, it is increasingly becoming part of mainstream debate and actively promoted by some who have advised left-leaning members of the US Democratic party.

Are there any constraints to MMT, however? One is the physical nature of cash. Under current circumstances, savers can attempt to escape negative interest rates by hoarding banknotes, which we estimated costs generally around 20 basis points. This puts a theoretical floor on where interest rates could go in order to stimulate the economy.

Central bank digital currencies (CBDCs) could change the picture further. CBDCs are not intended to be a monetary policy tool – but it could become a powerful one. Today, several major central banks are studying the possibility of a digital currency, with China already testing systems at a local level. The official purpose is to make payments in a fast, efficient and safe way. However, digital currencies could introduce a powerful monetary policy tool: very negative policy rates. In the case of China there is also an attempt to gain a higher share of global reserves, and spread the use of a digital Yuan across the belt and road countries.

Today, there is a physical obstacle against pushing rates to very negative levels, and against financial repression. As we estimated, savers may avoid interest rates below -0.2% by simply storing cash. However, if physical money doesn’t exist, a central bank could make rates as negative as they want – effectively placing a heavy penalty on those who hoard cash instead of spending it.

Conclusions: Return of Capital

“A really efficient totalitarian state would be one in which the all-powerful executive of political bosses and their army of managers control a population of slaves who do not have to be coerced, because they love their servitude.”

Brave New World, A. Huxley, 1932

The Covid response comes with double digit deficits and trillions of additional government debt.

On the one hand, it is an opportunity to re-start capitalism, boosting productivity and growth and moving away from the asset-focused policy mix of the past decades, which contributed to secular stagnation. Today, the US administration has a real chance to achieve this. It is a challenging task which requires implementing difficult micro policies: opening up education, breaking corporate monopolies, redistributing opportunity and improving social mobility. On the other hand, should this policy effort fail, it is investors and savers who are most likely to pay the bill. Financial repression is already here, in the form of a tax on investors for holding cash and government debt, yielding well below inflation. History tells us that the current level of real rates, at -1% in the US, is still mild. Put differently, things could get a lot worse in a prolonged liquidity trap, or QE infinity, where negative rates are compounded over time.

What would this look like? In his visionary book, Aldous Huxley imagined a world where technology and healthcare compound a winner-takes-all effect and are only enjoyed by the few – a world where humans are provided with their basic needs, in exchange for their freedom. It is a scenario that casts a shadow over our future, almost a century later. In a prolonged stagnation where reforms fail, leaving rising inequality, it is easy to imagine persistent government deficits and a gradual drift towards MMT and universal basic income at the next slowdown – how will governments secure consensus? There’s nothing more permanent than a temporary government programme, as M. Friedman said. These measures would not improve competitiveness or productivity, only put a lid on unemployment and social unrest. They might also cost investors dearly.

We do not know whether Biden’s reform agenda will win over secular stagnation – but we do know that a traditional bond or credit portfolio is poised to underperform either way. For investors in nominal assets – especially government bonds – there is little room for error: upside is capped by record-low yields, while any rise in volatility exposes to losses. The wipeout buffer for triple-B bonds is at 100-year lows. This means holding a long-only portfolio of bonds is similar to picking pennies on a railway track: bondholders will be wiped out by rising rates in a too-hot economic scenario and by rising spreads in a cold scenario.

If the outlook is grim for long-only passive fixed income strategies, there are plenty of opportunities for those who are active, for the following reasons. First, single-name and sector dispersion remains high despite low overall spreads, which gives fertile ground for alpha from picking winners vs losers. Second, most developed countries are likely to reach 50-75% immunity by mid-year, with substantial upside for cyclical sectors linked to economic reopening: transport, energy, financials and leisure. Third, more fiscal stimulus will kick-in, driving a further repricing of long-end rates above 1.5% for the 10-year Treasury – and with the Fed leaning against these moves, more Dollar depreciation.

We believe the best approach to capture these opportunities is to combine:

- Credit in selected sectors, offering robust carry at yields of 3-7%.

- Convertible debt – offering upside optionality linked to real assets and growth.

- Cash – offering downside optionality at relatively limited opportunity cost.

Stay safe, and good luck in 2021.

Image Credits: Duncan Rawlinson, Flickr

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© Algebris Investments. Algebris Investments is the trading name for the Algebris Group.